First Securitisation of Bitcoin-backed Loans: The Beginning of a New Asset Class

Vinod Kothari and Simrat Singh | Finserv@vinodkothari.com

Ledn, a Cayman Islands based bitcoin-backed lender, has originated what is believed to be the first securitisation of bitcoin-backed loans. It is a pool of about $ 199 million bitcoin-backed loans, with a first loss piece of $ 11 million, roughly 6% of the pool.

Rating agency S&P assigned BBB (sf) rating to Class A, which has 20% credit support, and B-(sf) to Class B with 6% support.

For the first time, cryptocurrency collateral has been converted into a rated, tranched capital markets instrument. Bitcoin exposure, historically confined to exchanges and wallets, has been structured into bankruptcy-remote securities assessed by a mainstream rating agency. More importantly, the deal demonstrates that Bitcoin price volatility, custody mechanics and automated liquidation frameworks can be modelled within established credit enhancement and subordination structures.

Lending against crypto collateral

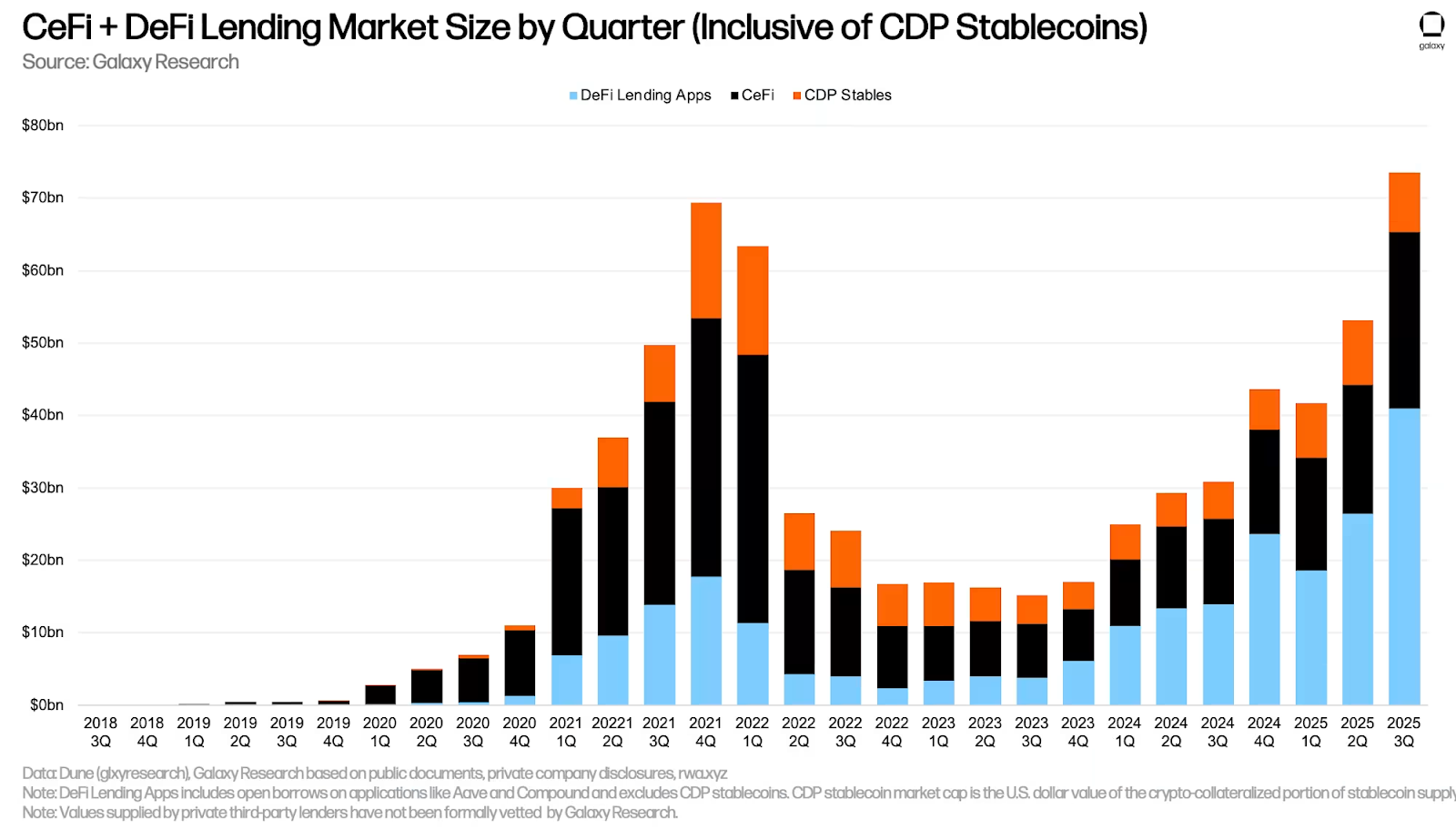

The market for collateralised lending against crypto currencies, according to a November 25 report by Galaxy, grew to reach a record volume of $ 73.6 billion by the end of Q3, 2025. This includes decentralised finance (DeFi) and centralised finance (CeFi) (see discussion below). DeFi uses smart contracts built on public blockchains to create a loan transaction if certain conditions are met; it creates a pledge that liquidates the currency if the specific LTV ratio is breached. Hence, the lending is almost like auto-triggered leverage on the crypto holding. In Defi, users retain custody of their assets and interact directly with protocols via crypto wallets. (See our article on DeFi here). CeFi, or better known as centralised lending is like the usual process of applying for a loan, qualifying for one, accepting the terms and then getting into a contract. Of course, the lending happens on specialised lending platforms, such as Binance or Coinbase.

On-chain and off-chain

As per IMF, crypto lending and borrowing is mostly channeled through crypto exchanges/financial digital platforms both centralized and decentralized, specialized in this business. The lending and borrowing through centralized (e.g., Nexo) and decentralized (e.g., Aave) platforms is also generally known as off-chain and on-chain lending, respectively. In the context of lending through centralized platforms, off-chain refers to the fact that the lending process and transactions are managed off the blockchain by a central entity. In contrast, lending through decentralized platforms is considered on-chain because it leverages smart contracts on a blockchain to facilitate lending and borrowing transactions. More importantly, on-chain transactions are actively facilitated by the platform which will ensure sufficient liquidity from depositors is available for lending

| Feature | Centralised Finance | Decentralised Finance |

| Intermediary | Centralised platform | No intermediary (protocol based) |

| Custody | Platform holds asset ie off-chain | Assets are held on-chain |

| Execution | Managed internally | Smart contract based automatic execution |

| Transparency | Limited since it depends on internal systems | Fully on-chain and therefore more transparent |

| Liquidation | Platform manager | Auto triggered via smart contracts |

| User experience | Simpler | Relatively more technical |

Regulatory concerns

Cryptocurrencies raise several regulatory concerns globally. Regulators are primarily focused on investor protection, given the extreme price volatility, risk of fraud, exchange failures and lack of clear legal recourse for users. Financial stability risk is another key concern, particularly as crypto markets grow in size and interlinkages with traditional financial institutions increase. Authorities also highlight AML, CFT and sanctions-evasion risks due to the pseudo-anonymous and cross-border nature of crypto transactions. Additional concerns include regulatory arbitrage, governance weaknesses at crypto platforms, custody and operational risks and the lack of uniform global standards regarding whether crypto should be treated as a currency, commodity, security or digital asset

In India, cryptocurrencies are not recognised as legal tender and are not considered currency under the law. The RBI has consistently expressed concerns regarding financial stability, monetary policy transmission, consumer protection, and illicit-flow risks. In April 2018, the RBI issued a circular prohibiting regulated entities from providing services to crypto businesses; however, this circular was set aside by the Supreme Court in Internet and Mobile Association of India v. RBI [Writ Petition (Civil) No.528 of 2018]. Despite the judgment, the RBI has maintained a cautious stance, warning that private cryptocurrencies may pose macroeconomic and systemic risks and advocating for strong regulatory oversight.

Most major crypto lending platforms are headquartered or legally domiciled in a small group of crypto-friendly financial jurisdictions rather than in countries that prohibit digital asset activity. A significant concentration is in the United States, particularly for larger, venture-backed platforms that target institutional or retail markets. Many crypto lenders are also structured through Cayman Islands and the British Virgin Islands due to flexible corporate law and tax breaks. In Asia, Singapore and Hong Kong have emerged as major hubs because they provide licensing regimes for virtual asset service providers and clearer regulatory frameworks for crypto trading and custody.

The United Arab Emirates (especially Dubai under the Virtual Assets Regulatory Authority or VARA) has become a fast-growing base for crypto exchanges and lenders due to its purpose-built digital asset regulatory regime. In Europe, activity is increasingly concentrated in jurisdictions aligned with the EU’s markets in Crypto-assets Regulations or MiCA framework, including countries like Germany and France, which offer regulated pathways for crypto custody and lending. Finally, Switzerland (Zug’s “Crypto Valley”) remains an important hub due to early legal recognition of digital assets and a mature fintech regulatory environment.

In short, most crypto lenders are located in jurisdictions that provide either (i) regulatory clarity with licensing pathways, or (ii) flexibility and structured-finance familiarity

How is the pledge of bitcoins registered?

Unlike land or securities, where a charge is perfected through a public registry or central depository, Bitcoin has no title registry on which a pledge can be recorded. A security interest over Bitcoin is, therefore, created contractually and perfected through control of the ‘private keys’. In practice, the borrower transfers the pledged Bitcoin into a segregated wallet held with a regulated custodian under a security and control agreement that prevents unilateral withdrawal and gives the secured party the right to direct liquidation of the Bitcoin held in that wallet upon default triggers.

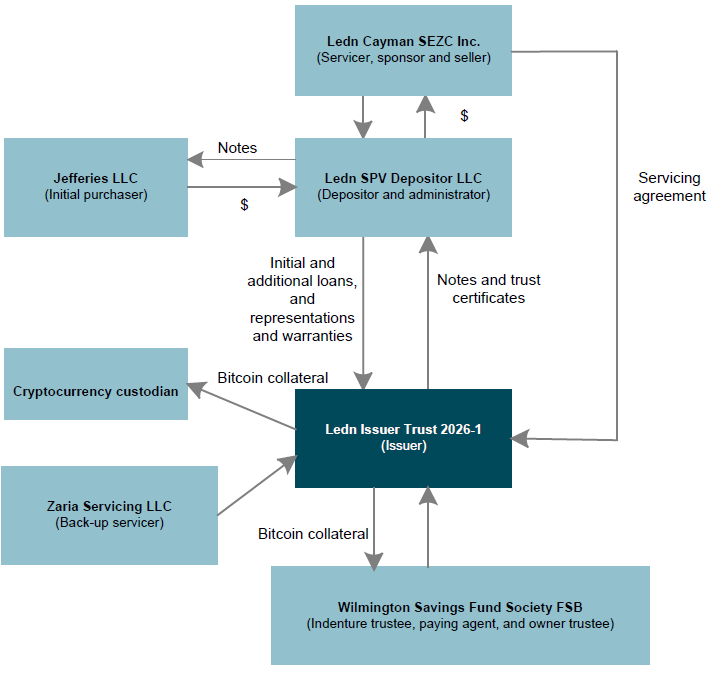

In the securitisation transaction at hand, this structure is embedded within a bankruptcy-remote issuer trust; the pledged bitcoin securing the underlying loans remains in custodian-controlled wallets, and the custodian agrees to follow the instructions of the trustee for investors.

Transaction Structure. Source: S&P Global

Why do borrowers take out a loan against crypto?

Borrowers might take crypto-backed loans to unlock liquidity without selling their crypto, preserving market exposure in case the crypto appreciates while avoiding a taxable disposal. Lenders market this explicitly (as “don’t sell your bitcoin”), because a loan does not trigger capital-gains events in many jurisdictions; selling does.

For example, in India, transfers of crypto [or Virtual Digital Asset (VDA) as defined in 2(111) of Tax Act, 2025] are taxed at a flat rate of 30% and subject to a 1% TDS as well (see section 194(1) and section 393 of Tax Act, 2025) which makes collateralised lending a much better alternative to an outright sale for investors seeking cash as it avoids a taxable transfer

Transaction structure

Underlying loans

The underlying collateral pool consists of 5,441 fixed-rate, balloon-style Bitcoin-backed loans extended to 2,914 borrowers, with an aggregate outstanding principal balance of approximately $199.1 million as of December 31, 2025 (’cut-off date’).

The loans are secured by approximately 4,078.87 BTC, which had an estimated fair market value of approximately $356.9 million at the cut-off date. This implies a weighted-average LTV of 55.78%, meaning the loans are materially overcollateralised at the borrower level.

While BTC collateral value (approx. $356.9 million) exceeds loan principal ($199.1 million), the securitised notes total $188 million ($160 million Class A + $28 million Class B). Credit enhancement to the notes is therefore driven by:

- Borrower-level overcollateralisation (WA LTV ~56%);

- Structural overcollateralisation of $11 million

- $199.1 million – ($160 million Class A + $28 million Class B)

- Subordination;

- A funded liquidity reserve ($9.4 million i.e. 5% of the outstanding note balance at closing);

Characteristics of underlying loans:

- Loan sizes range from $500 to $3,000,000;

- Interest rates range from 8.45% to 13.90%;

- Weighted-average interest rate: 11.80%;

- Weighted-average remaining term: ~8 months at cut-off;

- Maximum original tenor: 12 months

The loans are structured as bullet obligations, meaning borrowers repay principal and accrued interest in a single lump sum at maturity (or earlier via prepayment or liquidation). No scheduled amortisation occurs during the term.

If a borrower’s LTV rises to 80%, the loan is subject to liquidation through an automated engine that sells the BTC collateral to repay the loan.

Revolving Structure

The transaction features a 36-month revolving/reinvestment period. During this period, principal collections may be used to purchase additional eligible loans, subject to eligibility criteria and concentration limits. An initial $0.9 million funding account is available at closing to acquire additional loans. No principal is paid to noteholders during the revolving period unless an early amortisation event occurs. Such early amortisation triggers include:

- Servicer default;

- Effective advance rate exceeding 94%.

If triggered, the revolving period ends and principal begins to amortise sequentially (Class A first, then Class B).

Key sources of credit support include:

- Borrower-level overcollateralisation (WA LTV ~56%);

- Subordination;

- Liquidity reserve account;

- Funded at 5% of outstanding note balance at closing.

- Steps down over time

- Automated liquidation mechanism at 80% LTV

How does it address the volatility of Bitcoin prices

The transaction mitigates Bitcoin price volatility at both the loan and securitisation levels. At the loan level, underwriting is conservative, with loans originated at approximately 50% LTV, meaning borrowers pledge Bitcoin worth roughly twice the loan amount. As of the cut-off date, the pool had a weighted-average LTV of 55.78%. Margin notifications are issued at 70% and 75% LTV, and if LTV reaches 80%, the loan is automatically liquidated unless cured by additional collateral or partial repayment. This dynamic margin framework is designed to ensure that collateral is monetised well before LTV approaches 100%, thereby protecting principal.

At the securitisation level, protection is provided through multiple structural features. The collateral coverage is approximately 1.79x relative to loan principal, reflecting a substantial borrower-level cushion. In addition, the loan pool (~$199.1 million) exceeds the issued notes ($188 million), creating structural overcollateralisation of roughly $11 million. Subordination of the $28 million Class B notes beneath the $160 million Class A notes provides further credit enhancement, and a funded liquidity reserve of $9.4 million (5% of notes at closing) supports timely payment of interest and fees. While the underlying loans are short-term and bullet in nature, the transaction includes a revolving period, so volatility risk is managed primarily through LTV-triggered liquidation mechanisms and structural credit enhancement rather than tenor alone.

Conclusion

In jurisdictions where the legal status of cryptocurrency and its ownership remains uncertain or not expressly recognised, investor appetite for securities backed by crypto assets may be tempered. Questions around enforceability, custody and recognition of digital asset collateral could weigh on institutional participation. However, the relatively high interest rates associated with crypto-backed lending structures may prove attractive in yield-constrained environments.

For many investors, such securitisation offers an indirect pathway to participate in the economic upside of the cryptocurrency ecosystem, without holding the cryptocurrency directly and without assuming the operational, custody, or tax complexities associated with owning the asset itself. Whether this hybrid bridge between traditional capital markets and digital assets scales meaningfully will ultimately depend on regulatory clarity, investor risk tolerance and the continued maturation of crypto market infrastructure.

Lastly, the jurisdictional architecture is not incidental but foundational to transactions such as the present securitisation. A rated, bankruptcy-remote structure backed by Bitcoin-collateralised loans can emerge only where digital asset ownership, custody arrangements and enforcement mechanics are legally recognisable and commercially workable. The securitisation of bitcoin-backed loans is, ultimately, as much a product of regulatory geography as it is of financial engineering.

See our other resources:

- YouTube video: What is Securitisation?

- Tokenisation of Real World Assets – The Way Ahead for Creating Securities;

- Disrupting Traditional Card based Payments – Smart Contract based Payment Infrastructure using Stablecoin

- Cryptos: Are They Back in Business?;

- Security Token Offerings & their Application to Structured Finance;

- Decentralised Finances;

- Cryptocurrency on the path to Legalisation?;

- Cryptocurrency – A Cautionary Tale for India;

- Trustless System;

- Blockchain based lending; A peer-to-peer system;

- Financial Services firms foray into the metaverse.