NBFC-UL Classification Approach Revised by RBI

- Harshita Malik | finserv@vinodkothari.com

Background

RBI, vide its Press Release dated April 10, 2026, had issued draft Amendment Directions (read our article on the draft here) proposing changes to the methodology for identification of NBFC-Upper Layer (NBFC-UL) and the inclusion of Government-owned NBFCs in the Upper Layer. Following the consultation period, the RBI has finalised these proposals vide its Press Release dated June 24, 2026, effective immediately. The amendment package comprises four directions:

- SBR 2nd Amendment Directions: revises the UL identification framework under the Scale Based Regulation architecture;

- CRM 3rd Amendment Directions: extends concentration norms to Govt.-owned NBFCs and introduces the State Government guarantee provision;

- Governance Amendment Directions: exempts Govt.-owned NBFC-ULs from mandatory listing and pre-listing disclosures; and

- Financial Statements 2nd Amendment Directions: aligns the financial statements framework with the revised UL classification.

Revised Norms of Classification and Compliance

- Annual Classification/Identification Process:

RBI will continue to conduct an annual identification exercise for classifying NBFCs in the Upper Layer. Compliance obligations attach from the date the RBI notifies the NBFC-UL list, not from the date an entity crosses the asset threshold independently. - Revised Criteria for UL-Classification:

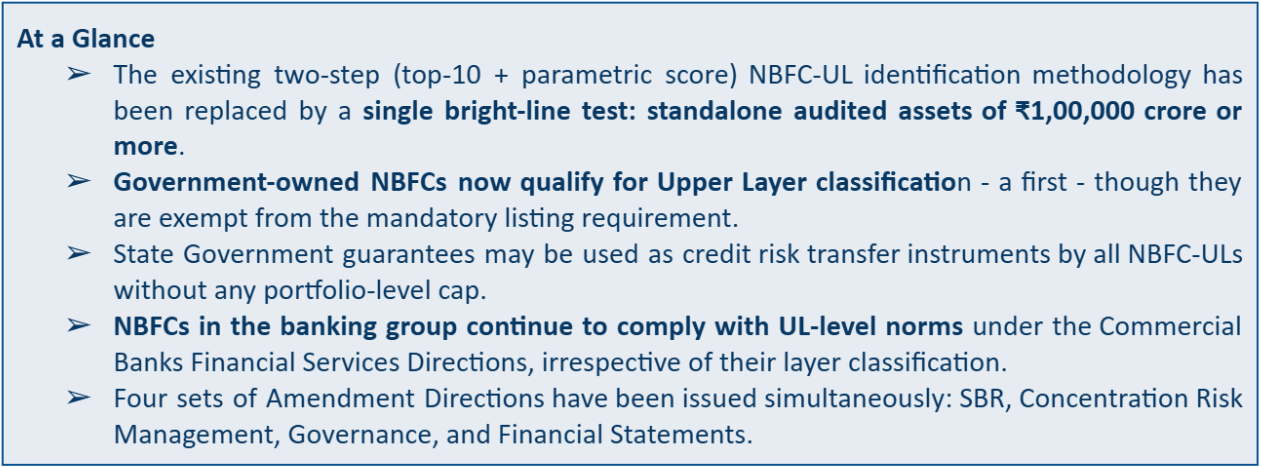

The current two-step approach (top ten by asset size and parametric scoring) will be replaced by a simple, absolute asset size criterion.

| An NBFC with standalone audited assets of ₹1,00,000 crore or more (as per the latest audited balance sheet) shall be classified in the Upper Layer. |

Key features of the revised criterion are:

- Standalone basis: asset size test applies to the standalone balance sheet of the NBFC, not consolidated group assets.

- Periodic review: ₹1,00,000 crore threshold will be reviewed every 3 years, more stringent than the 5-year cycle proposed in the draft, ensuring the threshold remains calibrated to market evolution.

- Bright-line simplicity: subjective scoring element is eliminated entirely, reducing regulatory uncertainty for entities near the boundary.

- Category-agnostic: UL list may include NBFC-ICCs, HFCs, CICs, deposit-taking NBFCs, and Government NBFCs; the type of NBFC is not a pre-condition.

- Inclusion of Government-owned NBFCs:

Eligible Government-owned NBFCs that breach the ₹1,00,000 crore threshold will now be included in the NBFC-UL list for the first time. Previously, these entities were placed only in the Base or Middle Layer. However, Government-owned NBFC-ULs are exempt from two obligations:- Mandatory listing within three years of notification (proviso to Para 43 of the Governance Directions); and

- Pre-listing disclosures (proviso to Para 23 of the Financial Statements Directions).

All other Upper Layer norms, including CET-1 capital, leverage, large exposures, governance, and provisioning requirements, apply in full.

- No exemption to Government Owned NBFCs from Concentration Norms:

Government-owned NBFCs will henceforth be subject to the concentration norms applicable to their respective layer. The earlier blanket exemption has been withdrawn. The transition is handled as follows:- Existing exposures that currently breach prudential limits are grandfathered and may continue until maturity, but no fresh exposure to such obligors is permitted.

- Additional exposure beyond prudential limits is permissible only if fully covered by eligible credit risk transfer instruments, resulting in zero net incremental exposure for Middle Layer and Upper Layer NBFCs.

- Provision for Credit Risk Transfer:

All NBFC-ULs may now use State Government guarantees to offset credit exposures without any portfolio-level cap. The regulatory treatment of the exposure so transferred is:- The exposure is recognised on the State Government (rather than the borrower);

- The exposure is exempt from prudential exposure limits; and

- 20% risk weight applies for capital computation purposes.

- Higher permissible exposure limit on connected counterparties for IFCs in Upper Layer:

NBFC-Infrastructure Finance Companies (‘NBFC-IFCs’) benefit from a specific carve-out: while the general rule caps exposure to a group of connected counterparties at 25% of the eligible capital base, NBFC-IFCs in the Upper Layer are permitted to go up to 45% of the eligible capital base (a 20 percentage-point premium) under the proviso to Para 35 of the Concentration Risk Management Directions. This reflects the inherently concentrated and long-tenor nature of infrastructure financing. - NBFCs in the Banking Group to comply with existing provisions:

NBFCs that are part of a banking group do not follow the SBR layer-based identification process for UL compliance. Instead, they shall continue to adhere to the applicable provisions for Upper Layer NBFCs, as per the RBI (Commercial Banks – Undertaking of Financial Services) Directions, 2025, for NBFCs under the banking group and carrying out lending activities. Our article on compliances to be followed by such NBFCs in the banking group can be seen here.

Regulatory Implications for Newly Classified NBFCs-UL

Classification as an NBFC-UL triggers a comprehensive set of enhanced regulatory requirements. Entities crossing the ₹1,00,000 crore threshold for the first time should anticipate the following:

| Compliance Area | Requirement for NBFC-UL | Trigger/Notes |

| CET-1 Capital | Minimum 9% of Risk-Weighted Assets | Binding where growth is aggressive |

| Leverage Ratio | Maintained alongside CRAR; special attention for derivative-heavy entities | Currently less acute as most NBFCs in India are not active in derivatives |

| Large Exposures Framework | Single-party cap: 20% of Tier 1 capital; Group cap: 25% (NBFC-IFC: 45%) | Economic-interdependence test determines group risk |

| Standard Asset Provisioning | Differential provisioning by asset class | Higher than ML/BL requirements |

| Mandatory Listing | Within 3 years of notification as UL | Exempt for Govt.-owned NBFC-ULs |

| Governance | Enhanced governance- board composition and listing requirements | Applicable under Chapter-V of the Governance Directions 2025 |

Closing Remarks

The shift from a hybrid scoring methodology to a single asset-size threshold is a significant moment in India’s NBFC regulatory architecture. The old framework, elegant in theory but notoriously opaque in application, left entities in a state of perpetual uncertainty about whether their exposure profile, liability structure, or interconnectedness would tip them over the UL line in any given year. The replacement with a bright-line rule removes that ambiguity.

That clarity, however, comes with a structural trade-off: the parametric approach was designed to capture systemic importance beyond sheer size: interconnectedness, leverage complexity, and liability fragility. A purely asset-based threshold is a blunter instrument. An NBFC with ₹1,05,000 crore in assets but a conservative, government-securities-heavy balance sheet will face the same UL compliance burden as one of equal size with complex wholesale funding and concentrated sector exposures.

The inclusion of Government-owned NBFCs is the more substantive policy shift. Large public-sector financial institutions, several of which have historically operated outside the SBR scrutiny framework, will now be subject to CET-1 discipline, large exposure limits, and differential provisioning. The listing exemption softens the reputational-governance dimension but does not dilute the prudential obligations.

The three-year review cycle (tightened from the draft’s five years) signals that the RBI is alive to the possibility that India’s NBFC sector may grow in ways that make ₹1,00,000 crore a less meaningful threshold over time. Market participants should treat this as a dynamic floor, not a permanent bright line.

Finally, the State Government guarantee provision, extending a zero-cap credit risk transfer tool to all NBFC-ULs, is a quiet but important liquidity-facilitation measure, especially relevant for NBFCs with significant exposure to state-owned utilities and infrastructure projects.

Leave a Reply

Want to join the discussion?Feel free to contribute!