Wholly controlled, but not wholly owned

– Payal Agarwal, Partner and Saloni Khant, Executive | corplaw@vinodkothari.com

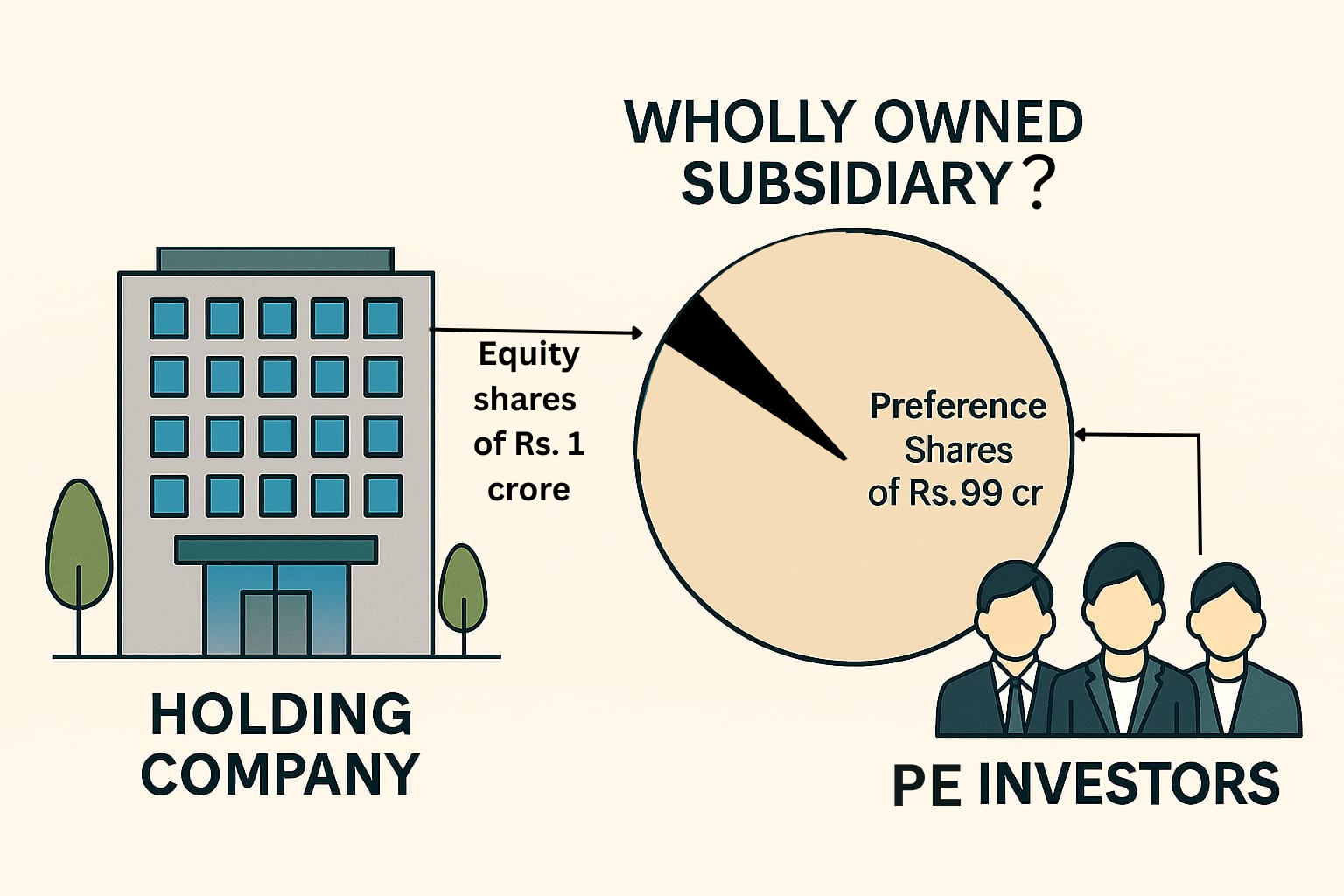

Do preference shares matter for wholly-owned subsidiary status?

Preference shares are a much preferred means of raising funds from third party investors by Indian startups. The reasons for such popularity may be accorded to the priority of payment over the equity shares, thus providing a layer of protection, flexibility in exit as compared to the permanent equity capital, ease of structuring and various other factors. Very often, this may lead to the total preference share capital holding a higher proportion as against the equity share capital of the company.

This brings a very interesting question to the fore – whether a company having preference share capital held by third parties, may still be considered to be a “Wholly Owned Subsidiary” (WOS), if such company has a sole equity shareholder, as its holding company. The question becomes particularly relevant in view of the exemptions provided to a company/ its group with respect to the WOS.

Compliance haven provided to a WOS

The Indian laws provide a myriad of relaxations in statutory requirements – a compliance haven to wholly owned subsidiaries.

Some of these have been tabulated below:

| Sr. No | Law | Section / Rule/ Regulation | Exemption |

| 1. | CA, 2013 | Section 185 | The prohibitions/ restrictions u/s 185 does not apply with respect to the loans given by the holding company to its WOS or security or guarantee provided in respect of loans to its WOS. |

| 2. | CA, 2013 | Section 186 | The limits on loan, guarantee, security, investments etc by holding company is not applicable in case of WOS. |

| 3. | CA, 2013 | Section 177(4)(iv) and 188 | Transactions between a holding company and its WOS are exempt from the approval of the Audit Committee, except in some cases. Further, RPTs specified under section 188 are exempt from shareholders’ approval. Our article on RPTs with WOS may be accessed here. |

| 4. | SEBI Listing Regulations, 2015 | Regulation 23 | Exemption from AC and shareholders’ approval for RPTs with a WOS or between two WOS of the listed holding company. |

| 5. | CA, 2013 | Section 149(4), 177 and 178 read with Rule 4 of the Companies (Appointment and Qualification of Directors) Rules, 2014 and Rule 6 of Companies (Meetings of Board and its Powers) Rules, 2014 | The following requirements do not apply: Appointment of independent directors Constitution of Audit Committee Constitution of Nomination and Remuneration Committee |

| 6. | CA, 2013 | Section 2(87) r/w Rule 2(1) of the Companies (Restriction on Number of Layers) Rules, 2017 | A layer consisting entirely of 1 or more WOS is not considered as a layer for the prohibition on having only 2 layers of subsidiaries. Our article on the restrictions w.r.t. layers of subsidiaries may be read here. |

| 7. | CA, 2013 | Section 29 read with Rule 9A(11) of the Companies (Prospectus and Allotment of Securities) Rules, 2017 | A public company that is a WOS is exempt from the requirement of mandatory dematerialisation of securities. Read our article on mandatory dematerialisation of shares here. |

| 8. | CA, 2013 | Section 233 | Fast track Merger is permitted between a holding company and its WOS. See our article on the procedure of fast track merger here. |

| 9. | SEBI Listing Regulations, 2015 | Regulation 37 | The requirement of obtaining a No-Objection Letter from the Stock exchange is dispensed for a scheme of arrangement between a listed holding company and its WOS. |

| 10. | SEBI Listing Regulations, 2015 | Regulation 37A | The requirement of shareholders’ approval for sale, lease or disposal of an undertaking, outside a scheme of arrangement, is exempt if made to the WOS. |

| 11. | The Indian Stamp Act, 1899 | Articles 23 and 62 of Schedule I, Circular issued in 1937 | Stamp duty on mergers is remitted if the merger is between a parent company and subsidiary company (parent company holding beneficial ownership of at least 90% of its share capital) or2 subsidiary companies (Common parent company is holding the beneficial ownership of at least 90% of the share capital of both the companies). Our article on the same may be accessed here |

The exemptions follow primarily an enterprise level approach, as against, entity level – thus, considering the WOS as nothing but an extended arm of the holding company. The Listing Regulations further uses the expression: whose accounts are consolidated with such listed entity, thus, signifying the relevance of ‘control’ while availing exemptions w.r.t. a WOS.

Thus, the position and rights of the preference shareholders need to be analysed in reference to whether the same provides any sort of ‘ownership’ or ‘control’ to such shareholders.

Preference shareholder as a member of the company

Section 2(55) of the CA, 2013 defines the term ‘member’ in the following manner:

(i) the subscriber to the memorandum of the company who shall be deemed to have agreed to become member of the company, and on its registration, shall be entered as member in its register of members;

(ii) every other person who agrees in writing to become a member of the company and whose name is entered in the register of members of the company;

(iii) every person holding shares of the company and whose name is entered as a beneficial owner in the records of a depository;

The definition covers every person whose name is entered in the register of members, as well as every person holding ‘shares’ in the company having their name recorded with the depository. The term ‘shares’ covers both equity and preference shares [Section 2(84) read with Section 43]. Further, in terms of section 88, the details of preference shareholders shall also be entered in the register of members. Thus, it is beyond doubt that the preference shareholders, too, are members of the company.

Preference shares: equivalent to ‘debt’ or considered as ‘capital’

In accounting parlance, preference shares are more likely to be classified as ‘debt’ than ‘equity’, depending on the terms of redemption or conversion. However, legally, the position of preference shareholder is not considered equivalent to a ‘creditor’, as has been a matter of jurisprudence in various cases.

The Hon’ble Bombay High Court held the following in the case of Aditya Prakash Entertainment Pvt. Ltd vs Magikwand Media Pvt. Ltd :

“The shareholders of redeemable preference shares of the company do not become creditors of the company in case their shares are not redeemed by the company at the appropriate time. They continue to be shareholders, no doubt subject to certain preferential rights mentioned in Section 85 of the Companies Act, 1956.”

The Bombay High Court cited references to Hindustan Gas and Industries Ltd. v. Commissioner of Income-tax, West Bengal-II, as also “Company Law” by Robert R. Pennington, 2nd edn. and noted from the said judgment that:

“ . . . we cannot persuade ourselves to accept the contentions of the assessee and hold that when a company issues redeemable preference shares it is in fact obtaining a loan as it could by issuing debentures. There is a fundamental difference between the capital made available to a company by issue of a share and money obtained by a company under a loan or a debenture. Respective incidences and consequences of issuing a share and borrowing money on loan or on a debenture are different and distinctive. A debenture-holder as a creditor has a right to sue the company, whereas a shareholder has no such right. Apart from that the scheme of the Companies Act and in particular the forms and contents of its balance-sheets are extremely rigid and, in our view, by reason of the specific compartments in such accounts it is not possible to convert an item of capital into an item of loan as has been suggested on behalf of the assesse.”

In the context of assigning a vote to the preference shareholders in a meeting of creditors, the Hon’ble Bombay High Court held the following in the case of State Bank Of India vs Alstom Power Boilers Ltd :

“A preference share is not a debt instrument. Preference share amount is a capital and not a debt. Thus, in the meeting of the creditors, it would not be possible to assign a value to the vote of a holder of preference share. If we were to hold that the preference shareholders who are not paid dividend for more than two years are also entitled to attend the meeting of the creditors under Section 391 of the Act and to vote thereat, then it would be impossible to determine what would be the value to their votes vis-a-vis the value of votes of creditors. It would be wrong to contend that preference shareholders have a right to vote but, valuation of their vote is unascertainable. We are therefore of the view that preference shareholders are not entitled to attend and vote at the meeting of the creditors convened under Section 391 of the Act even though dividend on the preference shares have remained unpaid for more than 2 years.

In Globe United Engineering & Foundry Co. Ltd, the Hon’ble Delhi High Court, while dealing with the question pertaining to the rights of the preference shareholders over arrears of dividend, observed the following:

“(15) The outside investor may be induced to subscribe for preference rather than ordinary shares by reason of the bargain offered; such investor has usually little knowledge of the company’s business, has no wish to participate in the company’s management and is keen only on his promised return. It may also happen that if the companies want to raise new capital when their existing shares are worth less than the nominal value the only direct way of raising new capital. apart from borrowings and debentures, will be to issue new class of shares with preferential rights over the existing ones. The preference shares are really part of the company share capital: they are not loans.”

The question of whether a failed redemption of preference shares constitute a contractual debt, has been a matter of jurisprudence, primarily in the context of maintainability of an application under IBC. See an article on the same here. The Hon’ble NCLAT, in a very recent judgement in the matter of EPC Constructions India Limited v. M/S Matix Fertiliser and Chemicals Limited, pertaining to the maintainability of an application by the preference shareholders under section 7 of IBC, held the following:

“…the Appellant who is holder CRPS is holder of shares which is in the nature of equity in capital, which is part of preferential share capital as defined in Section 43. Preferential shares being part of the preferential share capital of the Company shall not transfer any debt so as to initiate any Section 7 proceeding. Further, the Company having not earned any profit nor any dividend having been declared, no redemption was permissible by the statutory provision, hence, no debt was due on basis of which Section 7 application could be filed by the Appellant. There is also no material that any proceeds of a fresh issue of shares made for the Company Appeal (AT) (Insolvency) No. 1424 of 2023 purpose of such redemption was available. We, thus, fully endorse the finding of the Adjudicating Authority that there did not exist any default.”

Rights of the Preference Shareholders

Based on the various rulings discussed above, it is amply clear that preference shareholders are not creditors of the company, rather, shareholders. However, these are not equity shares, and cannot be treated at par with the equity shareholders. Murray A Pickering, in a scholarly analysis [The Problem of the Preference Share, Vol. 26 (1963) Modem Law Review], regards three principles as basically established and quotes from three decisions :

(1) The rights inter se of preference and ordinary shareholders must depend on the terms of the instrument which contains the bargain that they have made with the company and each other (a question of construction, vide Lord Simonds in Scottish Insurance Corporation, Limited v. Wilsons & Clyde Coal Company Limited, 1949 A.C. 462);

(2) where the articles set out the rights attached to a class of shares to participate in profits while the company is a going concern or to share in the property of the company in liquidation; prima facie, the rights so set out are in each case exhaustive (vide Wynn Parry, J. in re The Isle of Thenet Electricity Supply Co. Ltd., (1950) Ch. 161) and

(3) In the absence of specific provisions the rights of all shareholders are deemed to be the same (vide Lord Macnaghten in Birch v. Cooper and others, (1889) 14 A.C. 525)- case not referred (page 500 of Pickcring’s Article).

Thus, the rights of preference shareholders are based on the terms of the instrument and the Articles of the company. In the absence of any specific provisions, the rights of all shareholders are deemed to be the same.

Under the Companies Act, 2013, the rights of the preference shareholders are briefly contained in section 43 and section 47. Further, where a right is available to equity shareholders only, the same is stated expressly under the relevant provision. For instance, section 62 of the Act explicitly recognises only equity shareholders to be eligible for participating in a rights issue.

- Economic rights of preference shareholders

Certain rights are available to preference shareholders, by definition. This includes preferential rights with respect to:

- Payment of dividend, either as a fixed amount or a fixed rate

- Repayment of capital, at the time of winding up or otherwise

Depending on the terms of issue, this may further include the participating rights with respect to surplus dividend or capital repayment.

- Voting rights of preference shareholders

Section 47(2) of CA, 2013 limits the preference shareholders’ right to vote in a company on the following resolutions only in the same proportion as the paid-up capital in respect of the preference shares bears to the paid-up capital in respect of the equity capital:

- Resolutions which directly affect the rights attached to their preference shares.

- Resolution for winding up of the company.

- Resolution for the repayment or reduction of its equity or preference share capital.

However, pursuant to the second proviso to the said section, the preference shareholders acquire a right to vote on all the resolutions of the company where the dividend in respect of that particular class of preference shares has not been paid for a period of 2 years or more. Thus, the preference shareholders are not completely devoid of voting rights, they too have the right to vote on some matters or in specified conditions.

Preference shareholders, thus, may be compared with a sleeping monster. As long as the dividend is paid, the monster remains sleeping. But if the company defaults in the payment of their dividend for a period of 2 years, the monster awakens and is entitled to equal voting rights in the company as the equity shareholders. Once the default is made good by the company, that is to say, dividend is paid to the preference shareholders, whether the additional voting rights of such preference shareholders are revoked and they assume their erstwhile status or the voting rights assume permanence is not clearly laid down under the current provisions of CA, 2013. The question has been discussed in our article titled Voting Rights on Preference Shares: An Unclear Provision?. Companies putting off the payment of dividend on preference shares risk waking up the monster who might never go back to sleep again.

Further, pursuant to MCA notification no. GSR 464 (E) dated 5th June, 2015, certain exemptions were given to private companies. The notification, amongst others, provides exemption from the applicability of section 43 and section 47 to a private company where memorandum or articles of association of the private company so provides.

Hence, flexibility is provided to a private company to structure its share capital, including the voting rights therein, in the manner as may be required by such company, by providing for the same in the MoA or AoA of the company.

Thus, the voting rights on preference shares are not only in accordance with section 47 of the Act, but are also dependent on the terms of issue. In fact, companies which have issued compulsorily convertible preference shares (CCPS) often determine their total voting power on ‘as if converted’ basis.

- Rights as a member of the company

In addition to the rights specific to preference shares, other rights that are available to any member of a company are also available to a preference shareholder. These rights inter alia include:

- Right to receive annual reports and financial statements of the company [section 136]

- Right to receive notice and attend general meetings of the company [section 101]

- Right to inspect the registers and records of the company [section 94]

- Right to give special notice for removing directors [section 115]

- Right to give consent to or object to any proposed variation of shareholders’ rights [section 48]

- Right to apply to the Tribunal for relief in case of oppression & mismanagement [section 244]

Meaning of ‘subsidiary’: based on shares or voting rights?

Wholly owned subsidiary is basically a ‘subsidiary’ that is ‘wholly owned’ by a shareholder. The term ‘Wholly Owned Subsidiary’ has not been defined under the CA, 2013 or the SEBI Listing Regulations, 2015. However, reference may be drawn from the definition of ‘subsidiary company’ as defined in section 2(87) of the CA, 2013. The definition reads as:

‘A company in which the holding company controls the composition of the Board of Directors or exercises or controls more than one-half of the total voting power either at its own or together with one or more of its subsidiary companies.’

Note that a subsidiary is defined with reference to ‘voting powers’ and not ‘shareholding’. Therefore, the non-voting share capital of a company is not required to be considered in the determination of a company as a ‘subsidiary’.

The shift from ‘total share capital’ to ‘total voting power’ was based on the recommendations of the Company Law Committee, which considered the alignment of the meaning of subsidiary with consolidation principles in accounting. The CLC deliberated as follows:

During the deliberations, it was noted that by virtue of the present definition, a company in which the preference share capital was greater than its equity share capital, could become a subsidiary of an entity that holds the preference shares, even though it might not have control, or any voting rights in such a company. Further, inclusion of the preference share capital in the total share capital could create confusion about ownership of the company. Further, such companies could be shown as subsidiaries, but would not be considered for consolidation purposes, as per the applicable Accounting Standards.

Thus, preference shareholding would generally not be considered for the purpose of determining a holding-subsidiary relationship, unless such preference shares carry voting rights. Further, in view of the rationale provided by the CLC, it is clear that the voting rights need to be in the nature of ‘decision-making’ rights, and not merely affirmative or protective rights.

Wholly-owned subsidiary: is control the only factor?

While the determination of a subsidiary is based on voting powers, can it be said that it is only the equity shareholders that ‘own’ a company? In other words, whether the preference shareholders do not have any ‘ownership’ rights over the company?

In the context of incorporating a WoS outside India, the erstwhile Foreign Exchange Management (Transfer or Issue of Any Foreign Security) Regulations, 2000, further amended in 2004defined the term Wholly Owned Subsidiary as “A foreign entity formed, registered or incorporated in accordance with the laws and regulations of the host country, whose entire capital is held by the Indian party.” In the absence of any specific exclusions from the meaning of ‘capital’, the same would cover both equity and preference share capital.

Though this definition is no longer in force, the same hints on the intent of the regulator in considering the entire share capital holding as a criteria for considering a company as WoS.

WOS in the Global Context

That the determination of ‘subsidiary’ is a control-based approach, whereas a WoS is based on the entire shareholding and not merely voting rights is very clearly laid down in section 1159 of the Companies Act, 2006 of the United Kingdom. The section defines both ‘subsidiary’ and ‘wholly owned subsidiary’, in the following manner:

| Subsidiary | Wholly owned subsidiary |

| A company is a “subsidiary” of another company, its “holding company”, if that other company— (a)holds a majority of the voting rights in it, or (b)is a member of it and has the right to appoint or remove a majority of its board of directors, or (c)is a member of it and controls alone, pursuant to an agreement with other members, a majority of the voting rights in it, or if it is a subsidiary of a company that is itself a subsidiary of that other company. | A company is a “wholly-owned subsidiary” of another company if it has no members except that other and that other’s wholly-owned subsidiaries or persons acting on behalf of that other or its wholly-owned subsidiaries. |

Thus, while a ‘subsidiary’ is based on majority voting rights or such other rights that leads to ‘control’, the test of ‘wholly owned subsidiary’ is dependent on the sole membership, and is not restricted to just voting rights.

The Companies Act, 2006 of Singapore also defines subsidiary and wholly owned subsidiary in a similar fashion:

| Subsidiary | Wholly owned Subsidiary |

| 5.—(1) For the purposes of this Act, a corporation shall, subject to subsection (3), be deemed to be a subsidiary of another corporation, if — that other corporation — (i) controls the composition of the board of directors of the first-mentioned corporation; (ii) controls more than half of the voting power of the first-mentioned corporation; or (iii) holds more than half of the issued share capital of the first-mentioned corporation (excluding any part thereof which consists of preference shares and treasury shares); or the first-mentioned corporation is a subsidiary of any corporation which is that other corporation’s subsidiary. | 5B. For the purposes of this Act, a corporation is a wholly owned subsidiary of another corporation if none of the members of the first-mentioned corporation is a person other than — that other corporation;a nominee of that other corporation;a subsidiary of that other corporation being a subsidiary none of the members of which is a person other than that other corporation or a nominee of that other corporation; ora nominee of such subsidiary. |

Thus, while preference shares are explicitly excluded from the definition of ‘subsidiary’, no similar approach is followed in defining a wholly owned subsidiary.

15 U.S. Code § 80a-2 defines the term WoS in reference to ‘voting securities’. Thus, WoS is defined as: “a company 95 per centum or more of the outstanding voting securities of which are owned by such person, or by a company which, within the meaning of this paragraph, is a Wholly Owned Subsidiary of such person”. ‘Voting securities’, as defined in the said Code means “any security presently entitling the owner or holder thereof to vote for the election of directors of a company”. This may also include the preference shares, given the 12 U.S. Code § 51b entitles preference shareholders to such voting rights as may be provided for in the Articles of Association of the company.

Conclusion

Preference shareholders, though having certain rights distinct from equity shareholders, are still members of the company. Voting rights may be assigned to them either as a part of the terms of issue or upon non-payment of dividend. These preference shares may either be redeemable or convertible, and in case of the latter, becomes a part of equity share capital upon conversion. Wholly owned subsidiary should indicate complete ownership, in the form of 100% shareholding, and hence, even non-voting shares should be considered for the purpose of identification of an entity as such.

Where the preference shares are held by a person other than the holding company, the company should not be entitled to the benefits of being a wholly owned subsidiary.

Leave a Reply

Want to join the discussion?Feel free to contribute!