Scalar regulatory framework for the NBFC sector

-Financial Services Division (finserv@vinodkothari.com)

RBI has issued the Revised Regulatory Framework for NBFCs, effective from October 1, 2022. Highlights of prescribed framework can be accessed at this link.

Introduction

Systemic risk of NBFCs has been an issue for discussion, specifically in India as there have been some major NBFC failures, and the issue of inter-connectivity between NBFCs and the rest of the financial sector became clearly evident[1]. The issue is not limited to India -globally, an annual publication of the Financial Stability Board, called Global Monitoring Report on Non-banking Financial Intermediation[2] has been drawing attention to the increasing relevance of non-banking financial intermediaries and the risk they pose.

The RBI had, in its Statement on Development and Regulatory Policies dated December 4, 2020[3], highlighted a need to review the regulatory framework in line with the changing risk profile of NBFCs. The NBFC sector has witnessed various changes in the regulatory framework in the past few years, making it more comprehensive. However, the tremendous growth in the sector combined with regulatory arbitrage enjoyed by the NBFCs is now leading to a systemic risk. Hence, the regulators have thought it necessary to tighten the regulatory norms for NBFCs holding a major chunk of market share.

In line with the aforesaid announcement, the RBI released a Discussion Paper on January 22, 2021[4] seeking inputs from industry participants. The following write-up analyses the major propositions made by the RBI.

Highlights of the New Regulatory Framework

- 4 layers of regulatory intensity – progressively from bottom – BL, ML, UL, and TL, Base layer (BL) to be systematically non-significant entities, with light touch regulation. Some entities like Type 1 NBFCs (those without public interface or public funds) will always remain in the Base layer, seemingly irrespective of size. ML to consist of the systemically important NBFCs. From ML, 20-25 entities to be selected for tighter supervision, based on indicia of higher systematic risk. TL is empty by default, but to be populated only on exercise of supervisory discretion for extreme risks.

- Monetary threshold for systematic significance to be revised upwards from Rs 500 crores to Rs 1000 crores

- Aims at eliminating regulatory arbitrage at Layer 2 (ML) and above; seeks to align regulatory framework at ML with banks.

- Layer 3 (UL) is a new regulatory layer; regulations expected to be at par with banks.

- UL classification is not something that would take the NBFC by surprise; the decision to be put into the category will be communicated in advance with an opportunity to manoeuvre and come out the classification

- Entry-point requirement for new NBFC registrations to be increased 10 times, from Rs 2 crores to Rs 20 crores. Existing NBFCs to be given a timeframe, say, 5 years to measure up.

- NPA norms for BL NBFCs (currently, the NSI category) to be made 90 days instead of 180 days as of now

- At least one of the directors of the NBFCs to be a person with retail lending experience.

- ICAAP to be applicable to NBFC-ML and above.

- Auditor rotation after 3 years, appointment of a Chief Compliance Officer, managerial compensation controls, and several disclosure requirements to be imposed on ML entities.

- Concentration limits: Board-imposed caps on sectoral exposure; IPO financing limits, self-imposed real estate exposure – proposed for ML entities

- Core Banking Solution be adopted by NBFCs with 10 or more branches

- Upper Layer to consist of 25-30 entities selected from a sample of about 50 entities, based on scoring methodology, indicating distinctive systemic risk. 9% Common Equity Tier to be prescribed for these entities. Additionally, leverage limits may also be imposed.

- Differential provision for standard assets to prescribed for UL entities

- Mandatory listing, managerial remuneration controls, etc to be prescribed for UL entities

- Top layer to be similar to protective framework in case of banks: Higher capital charge, capital conservation buffer

Regulatory arbitrage: The concern behind present regulatory proposal

The operational flexibility provided to NBFCs has enabled them to assume a scale that would potentially impact systemic stability. In recent years, the regulator has identified structural arbitrage and prudential arbitrage between banks and NBFCs. While the former emanates from differences in legislative and licensing framework like net owned funds, branch approval requirements etc., the latter is concerning CRAR, prescribed leverage, liquidity guidelines etc.

There also exists some relaxation in corporate governance and disclosure norms for NBFCs in comparison to banks such as instructions on compensation policy for WTD/CEOs/Risk Control Staff and most of SCB being listed and thus abiding by the listing requirement.

NBFCs have become more interconnected with the financial system. Linkages are due to the substantial exposure that banks have in NBFCs. As per the Financial Stability Report of January 2021, NBFCs were the largest net borrowers of funds from the financial system. The gross payables and receivables stood around ₹9.37 lakh crore and ₹0.93 lakh crore as at end-September 2020.[5] More than half of this funding was supported by scheduled commercial banks (SCBs) followed by Asset Management Companies-Mutual Funds (AMC-MF) and Insurance Companies. Further the Discussion Paper noted that there are seven NBFCs (including HFCs) each having asset size exceeding 1 lakh crore and above.

The unconstrained growth of the NBFC sector in addition to the lenient regulatory framework within an interconnected financial system may sow the seeds of systemic risk. In the present scenario, failure of any large and deeply interconnected NBFC is capable of transmitting shocks into the entire financial sector and causing disruption even to the operations of the small and mid-sized NBFCs.

Classification of NBFCs by scale of activities, risks and size

The proposed framework provides for the regulation on scale based approach. This essentially means that regulatory and supervisory resources are to be more focused on the entities which have become too-big-to-fail (TBTF) owing to their systemic interconnectedness with other financial market participants. The degree of regulation is to be based on ‘principle of proportionality’. The three triggers of scale based regulation are:

- Risk perception: This parameter is based on size, leverage and interconnectedness of the NBFC with market participants in terms of prescribed threshold.

- Size of operations: The size of the balance sheet of an NBFC beyond a certain prescribed high threshold would be an important independent factor in determination of regulation.

- Nature of activity – Just by performing financial activity cannot give rise to systemic risk. Like Type 1 NBFCs which do not access public deposits and neither have customer interfaces are to be regulated with light touch. The essence of such form of NBFCs is that the financial activity is being carried out by net-owned funds. However some activities are regarded as high risk owing to their systemic connectivity and business model. The draft paper categorises NBFC-HFC, IFC, IDF, SPD and CIC as they are interconnected with other financial institutions while performing credit intermediation.

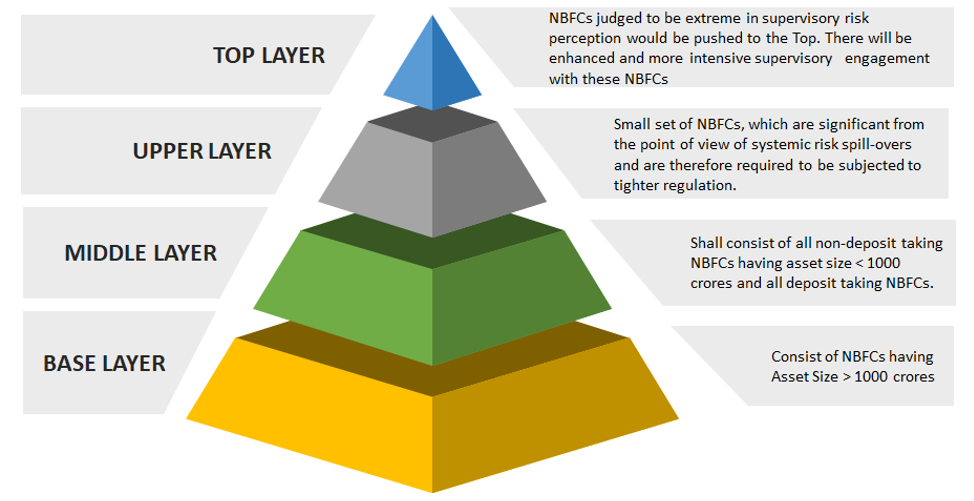

The RBI has proposed a scale-based four-layered structure regulatory framework–viz. Base Layer (NBFC-BL), Middle Layer (NBFC-ML), Upper Layer (NBFC-UL) and Top Layer. The classification of layers is made commensurate to the regulatory intervention required- i.e. the base layer having the least regulatory intervention and the intervention increasing as the one moves up the pyramid. The proposed categorisation/classification as provided in the discussion paper is summarized in the fig below.

Interestingly, CICs are poised to be put under greater scrutiny- this is possibly the regulatory reaction to a recent NBFC default. CICs are proposed to be regarded as Middle Layer NBFC (NBFC-ML) along with NBFCs currently classified as systemically important NBFCs (NBFC-ND-SI), deposit-taking NBFCs (NBFC-D), HFCs, IFCs, IDFs, SPDs. Though CICs and SPDs will fall in the Middle Layer of the regulatory pyramid, the existing regulations specifically applicable to them, will continue to apply. However, a pertinent question for discussion would be whether the activity-based classification of NBFC-AA, P2P, NOFHC in Lower Layer and NBFC-HFC, IFC, IDF, CIC and Standalone Primary Dealers in Middle Layer justified.

Increased NOF & harmonisation of NPA recognition

Further, NOF is proposed to be raised to Rs. 20 crores. Further, in order to ensure a smooth transition, a well-defined timeline will be prescribed by the RBI for existing NBFCs, spanning over a period of, say, five years. For new registrations, the higher NOF norms will get implemented immediately on the issue of instructions.

NPA recognition based on 90 DPD will be extended to all NBFCs including those which are not systemically important.

Recognition of NBFCs in Upper Layer

NBFC categorisation is based on annual review. The paper recognises two parameters; quantitative and qualitative:

- The quantitative parameters will have 70% weightage.

- The qualitative parameters will have 30% weightage.

The table below represents quantitative and qualitative parameters as proposed:

| Parameter | Sub-parameter | Sub weight | Weights |

| Quantitative Parameters (70%) | |||

| Size & Leverage | Size: Total exposure (on-and off-balance sheet)

Leverage: total debt to total equity |

20+15 | 35 |

| Interconnectedness | i) Intra-financial system assets:

– Lending to FIs – Securities of other FIs – Mark to market REPO – OTC derivatives

ii) Intra-financial system liabilities

– Borrowings from FIs – Marketable securities issued by finance company to FI – Mark to market OTC derivative with FIs iii) Securities outstanding (issued by NBFC) |

10

10

5 |

25

|

| Complexity | i) Notional amount of OTC derivatives

– CCP centrally – Bilateral OTC

ii) Trading and available for sale securities |

5

5 |

10 |

| Qualitative Parameters/Supervisory inputs (30%) | |||

| Nature and type of liabilities | – Degree of reliance on short term funding

– Liquid asset ratios – Callable debts – Asset backed funding Vs. other funding – Asset liability duration and gap analysis – Borrowing split (secured debt, CCPS, CPs, unsecured debt) |

10 | 30

|

| Group Structure | – Total number of entities

– Total number of layers – Total intra-group exposure |

10 | |

| Segment Penetration | Importance of NBFC as a source of credit in a specific segment or area | 10 | |

The scoring will be done on a sample basis, by dividing the individual NBFCs amount by the aggregate sum of all the indicators in the sample. The score for each category will be converted into basis points and the overall systemic significance score will be based on the relative importance of the NBFC compared with other NBFCs in the sample.

The sample criteria for the purpose of above parameter based measurement is to be as follows:

- Excluding the top 10 NBFCs (based on asset size) as they will automatically fall in upper layer regulation.

- The sample will include next 50 NBFCs based on total exposure (including off balance sheet)

- NBFCs designated as NBFC-UL in previous year

- NBFCs added to sample by supervisors judgement

For leverage calculation the individual score of NBFC is to be divided by average leverage of the sample. A NBFC-UL will be subjected to enhanced regulatory requirements similar to that of banks at least for a period of four years from its last appearance in the category, even where it does not meet the parametric criteria in the subsequent year.

NBFCs in Base Layer

The base layer would cover NBFCs with asset size upto Rs 1000 crores. The major propositions for this layer are provided in the table below:

| Proposals for NBFCs in Base Layer | |

| 1. | The current regulations require NPA classification of the asset having more than 180 DPDs the same is proposed to be reduced to 90 DPDs in order to bring it in sync with the regulatory guidelines for other classes of NBFCs |

| 2. | The board shall be required to have –

(i) Adequate experience and educational qualification (ii) At least one of the directors should have experience in retail lending in a bank/NBFC |

| 3. | For the Risk Management Committee-

(i) Overall role and responsibilities to be laid out, and (ii) Composition could be Board or Executive level as to be decided by the Board |

| 4. | The regulations for sale of stressed assets shall be made at par with banks once guidelines are finalized |

| 5. | Additional disclosures on type of exposures, related party transactions, customer complaints shall be prescribed |

NBFCs in Middle Layer

Several new regulatory requirements are proposed for this category in addition to the proposals for the base layer. There are no changes proposed in capital requirements for NBFC-ML.

| Proposals for NBFCs in Middle Layer | |

| 1. | Board approved policy taking into account all risks for Internal Capital Adequacy Assessment shall be required. |

| 2. | The extant credit concentration limits prescribed for NBFCs for lending and investment is proposed to be merged into a single exposure limit of 25% for single borrower and 40% for group of borrowers anchored to Tier 1 capital instead of Owned Funds |

| 3. | Compulsory Rotation of auditors shall be applicable- After completion of continuous audit tenure of three years, Auditors shall not be eligible for re-appointment for a period of six years (two tenures) |

| 4. | i) Appointment of a functionally independent Chief Compliance Officer.

ii) Additional Corporate Governance and Disclosure Requirements, including requirement for Secretarial Audit. |

| 5. | It has been proposed that no KMP of an NBFC shall be allowed hold office in any other NBFC-ML or NBFC-UL or subsidiaries, further, an Independent Director cannot be director in more than two NBFCs (NBFC-ML and NBFC-UL) at the same time |

| 6. | Board approved internal limits and adequate disclosures would be required for exposure to sensitive exposures and Dynamic vulnerability assessment by NBFCs shall be required. Sub-limit within the commercial real estate exposure ceiling should be fixed internally for financing land acquisition

|

| 7. | Restrictions on grant of loans and advances for/to the following:

(a) buy back of shares/ securities (b) activities leading to Ozone Depleting Substances (c) Directors and relatives of directors (d) Officers and relatives of Senior Officers (e) Real Estate – only where project approvals other permissions are in place. |

| 8. | The IPO financing by NBFCs shall be capped at Rs.1 crore. There is no limit prescribed for NBFCs at present, while there is a limit of Ts. 10 lakh for banks for IPO financing. |

| 9. | Mandatory for NBFCs with more than 10 branches to have Core Banking Solution for NBFCs |

NBFCs in Upper layer

In addition to the regulations applicable to NBFC-ML, a set of additional regulations will apply to NBFC-UL, they are:

| Proposals for NBFCs in Upper Layer | |

| 1. | CET 1 may be prescribed at 9% within the Tier I capital

In addition to the CRAR requirements, NBFCs will also be subjected to a leverage requirement |

| 2. | Differential Provisioning being similar as banks for standard assets to be made applicable |

| 3. | For Concentration norms-

(i) Large Exposure Framework (LEF) as applicable to banks with suitable modification will apply (ii) Transition time for implementation |

| 4. | Corporate Governance norms to be similar lines as applicable for Private Sector Banks. Additional governance regulations such as specifying qualification of board members, providing detailed disclosure on group companies including consolidated financial position and details of related party transactions. |

| 5. | Adequate phase-in-time for mandatory listing to be provided. However, disclosure requirements will kick in earlier than actual listing within the broad implementation plan for NBFC-UL |

| 6. | Removal of Independent Director shall require supervisory approval |

NBFCs in Top Layer

The top layer is currently empty and will get populated in case RBI takes a view that there has been an unsustainable increase in the systemic risk spill-overs from specific NBFCs in the Upper Layer. NBFCs in this Layer will be subject to higher capital charge, including Capital Conservation Buffers. There will be enhanced and more intensive supervisory engagement with these NBFCs.

Monetary threshold for systemically important NBFCs

Asset size of Rs 500 crores was stipulated a long time back for distinguishing between SI and NSI NBFCs, that is on November 10, 2014. The limits were in line with recommendations made by the Working Group on Issues and Concerns in the NBFC Sector, chaired by Smt. Usha Thorat.

After more than 6 years, the RBI proposes to increase the threshold from Rs 500 crores to Rs 1000 crores.

The inherent sense of reservation in this measure is itself evident from the data that the RBI has shared – that the number of NSI companies will go up from 9133 to 9209. That is, merely 76 companies will be taken out of the SI classification and put into BL category.

10-fold jump in entry point net worth requirement

If some people familiar with the evolution of regulatory framework for NBFCs may recall, the NOF requirement for NBFCs was Rs 25 lacs in 1990s. Then, it was increased to Rs 2 crores. The regulator is now proposing to increase the same to Rs 20 crores – a 10 fold increase. The underlying rationale is to have a stronger entry barrier, and to ensure that NBFCs have the initial capital for investing in technology, manpower and establishment. However, this sharp hike in entry point requirement will keep smaller NBFCs out of the fray. Smaller NBFCs, particularly those with geographical or sectoral focus, have been doing a useful job in financial inclusion.

Conclusion

The regulatory frame is going for a complete overhaul. While the new regulatory framework should have been expected to to smaller NBFCs out of regulatory glare, it is notable that only 76 companies are sliding down from SI status to NSI status due to the proposed change. The whole principle of scalar regulation should have been lesser entities to regulate, so that there is more attention where attention is needed. Further, the principle of scalar regulation would intuitively have more regulation at higher levels, but lesser regulation at the bottom of the pyramid. There are no apparent signals of reduced regulation at the base level. On an overall assessment, the scalar regulatory frame is a new thought process, and should be appreciated.

The video on “Round table discussion on RBI’s proposed regulatory framework for NBFCs” can be viewed here

Our Presentation on the topic can be viewed here

[1] See an article by Vinod Kothari, tilted Shadow Banking in India – Creating an Opportunity out of a Crisis, at https://vinodkothari.com/2020/01/shadow-banking-in-india/

[2] The 2020 Report is here: https://www.fsb.org/wp-content/uploads/P161220.pdf

[3] https://www.rbi.org.in/Scripts/BS_PressReleaseDisplay.aspx?prid=50748

[4] https://rbidocs.rbi.org.in/rdocs/Publications/PDFs/DP220121630D1F9A2A51415B98D92B8CF4A54185.PDF

Leave a Reply

Want to join the discussion?Feel free to contribute!