Foreign Entities getting into Payment Systems in India

By Vinita Nair, Vishes Kothari, Rajeev Jhawar & Simran Jalan

India is one of the most exciting markets for fintech startups. Several overseas entities, having already established businesses overseas, want to set up mobile wallets or payments systems in India. This makes them run into two laws, first by virtue of being an overseas entity desirous of moving funds in some form or the other into India, and second because it is entering the payment and settlement systems space. These bring complexities of foreign direct investment covered by Foreign Exchange Management Act, 1999, and nuances of skeletal, regulation-based law under Payment and Settlement Systems Act, 2007. This article intends to provide an easy-to-comprehend guide to the applicable regulations for overseas entities getting into payment systems in India.

What is the Payment and Settlement Systems Act, 2007

Having received the assent from the President of India on 20th December, 2007 and effective since 12th August, 2008, the Payment and Settlement Systems Act, 2007 (PSS Act) provides for the regulation and supervision of payment systems in India and designates the Reserve Bank of India (RBI) as the authority for that purpose and all related matters. The Board for Payment and Settlement Systems within the RBI looks after the PSS Act.

What is a Payment System?

Section 2(1) (i) of the PSS Act, 2007 defines a payment system to mean

“a system that enables payment to be effected between a payer and a beneficiary, involving clearing, payment or settlement service or all of them, but does not include a stock exchange (Section 34 of the PSS Act 2007 states that its provisions will not apply to stock exchanges or clearing corporations set up under stock exchanges).”

It is further stated by way of an explanation that a “payment system” includes the systems enabling credit card operations, debit card operations, smart card operations, money transfer operations or similar operations. Payment systems would include all systems (except stock exchanges and clearing corporations set up under stock exchanges) carrying out either clearing or settlement or payment operations or all of them. The entities operating such systems would be called as system providers.

Further, the definition would also extend to all entities operating money transfer systems or card payment systems or similar systems. To decide whether a particular entity operates the payment system, it must perform either the clearing or settlement or payment function or all of them.

Are entities intending to operate a payment system required to get a license, approval or authorization for the purpose?

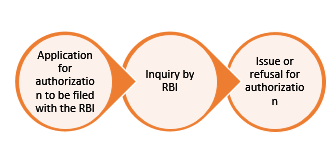

In terms of Section 4 of the PSS Act, 2007 no person other than the RBI can operate or commence a payment system unless authorized by the Reserve Bank. Any person desirous of commencing or operating a payment system needs to apply for authorization under the PSS Act, 2007 (Section 5).

The application for authorization has to be made as per Form A under Regulation 3(2) of the Payment and Settlement Systems Regulations, 2008. The application is required to be duly filled up and submitted with the stipulated documents to the Reserve Bank. A sum of Rs 10,000/- is required to be submitted as application fee, which can be submitted by cash or cheques or payment order or demand draft or electronic fund transfer in favour of the Reserve Bank along with the application for authorizations

The application for authorization has to be made as per Form A under Regulation 3(2) of the Payment and Settlement Systems Regulations, 2008. The application is required to be duly filled up and submitted with the stipulated documents to the Reserve Bank. A sum of Rs 10,000/- is required to be submitted as application fee, which can be submitted by cash or cheques or payment order or demand draft or electronic fund transfer in favour of the Reserve Bank along with the application for authorizations

All entities operating payment systems or desirous of setting up such systems are required to apply for authorization under the Act. Any unauthorized operation of a payment system would be an offence under the PSS Act, 2007 and accordingly liable for penal action under that Act.

In case of refusal of authorization application, an appeal can be made to the Central Government within thirty days from the date on which the order of refusal was communicated to the operator.

Are foreign entities allowed to operate a payment system in India?

In reference to Section 4 and Section 18 of the PSS Act 2007 there is no distinction made between foreign entities and domestic entities in regard to process required and post process matters.

Besides, each entity, irrespective of domestic or foreign, needs to obtain license/ approval / authorization from Reserve Bank before commencing payment system operations in the country. The PSS Act 2007 indicates that

“No person can operate a payment system except under and in accordance with an authorization issued by the Reserve Bank”.

Further, the PSS Act 2007 does not place any restriction on the types of payment systems / services a foreign entity can provide. However, any service provided by a domestic or foreign entity must be in accordance with the overall legal framework of the country.

Foreign entities viz., card networks like MasterCard (Singapore), Visa Worldwide Pte. Limited (Singapore), etc. are authorized under the PSS Act and operating card schemes in India. So are cross-border remittance service providers viz., Western Union Financial Services Incorporated, USA, MoneyGram Payment Systems Inc., USA., etc.

The Reserve Bank will endeavour to dispose of all applications received for authorization within six months from the date of their receipt.

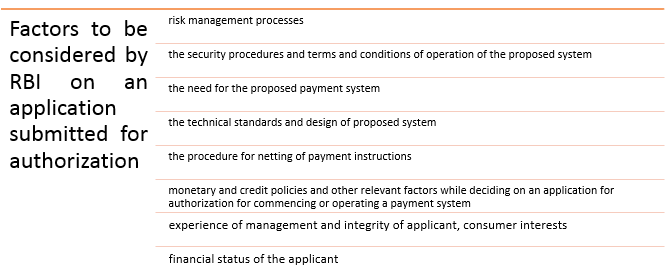

Application for authorization of a payment system operator is assessed against the criteria specified for a particular payment system. For example, the application for issuance and operation of PPI is assessed against the Policy Guidelines on Issuance and Operation of Pre-paid Payment Instruments in India. Similarly, in case of Central Counter Party, the application would be assessed against the backdrop of PFMI policy document issued by RBI.

As per Section 6 of the PSS Act, the Reserve Bank may make such inquiries as it may consider necessary for the purpose of satisfying itself the capacity, credentials of the participants or for any other valid reason.

In case, the entity is already regulated by any other authority, information from such authorities may be called for making the assessment. It may be mentioned that for licensing Indian entities as banks in the recent past, the process entailed calling for due diligence reports from foreign regulators wherever the applicant entity had group entities operating in foreign jurisdictions.

What is the Foreign Exchange Management Act?[1]

The legal framework for administration of foreign exchange transactions in India is provided by the Foreign Exchange Management Act, 1999 (FEMA).

Foreign entities may initiate business activities in India by starting a subsidiary in India, or by putting up a branch office, liaison office, etc. Each of these options may involve different tax consequences as also repatriation of money. However, the present discussion focuses on merely the FEMA issues. Establishment of branch office/ liaison office / project office or any other place of business in India by foreign entities is regulated by Foreign Exchange Management (Establishment in India of a branch office or a liaison office or a project office or any other place of business) Regulations, 2016 in terms of Section 6(6) of Foreign Exchange Management Act, 1999 read with 1Notification No. FEMA 22(R)/2016-RB dated March 31, 2016.

i. Applications from foreign companies (a body corporate incorporated outside India, including a firm or other association of individuals) for establishing BO/ LO/ PO in India shall be considered by the AD Category-I bank as per the guidelines given by Reserve Bank of India (RBI).

ii. An application from a person resident outside India for opening of a BO/LO/PO in India shall require prior approval of Reserve Bank of India in the following cases:

1. The applicant is a citizen of or is registered/incorporated in Pakistan;

2.The applicant is a citizen of or is registered/incorporated in Bangladesh, Sri Lanka, Afghanistan, Iran, China, Hong Kong or Macau and the application is for opening a BO/LO/PO in Jammu and Kashmir, North East region and Andaman and Nicobar Islands;

3.The principal business of the applicant falls in the four sectors namely Defence, Telecom, Private Security and Information and Broadcasting.

In the case of proposal for opening a PO relating to defense sector, no separate reference or approval of Government of India shall be required if the said non-resident applicant has been awarded a contract by/ entered into an agreement with Ministry of Defence or Service Headquarters or Defense Public Sector Undertakings. No separate approval is required from Reserve Bank of India for such cases only.

4.The applicant is a Non-Government Organisation (NGO), Non-Profit Organization, Body/ Agency/ Department of a foreign government.

Such applications may be forwarded by the AD Category-I bank to the General Manager, Reserve Bank of India, Central Office Cell, Foreign Exchange Department, 6, Sansad Marg, New Delhi – 110 001 who shall process the applications in consultation with the Government of India.

iii. The non-resident entity applying for a BO/LO in India should have a financially sound track record viz:

1.For Branch Office — a profit making track record during the immediately preceding five financial years in the home country and net worth of not less than USD 100,000 or its equivalent. Net Worth [total of paid-up capital and free reserves, less intangible assets as per the latest Audited Balance Sheet or Account Statement certified by a Certified Public Accountant or any Registered Accounts Practitioner by whatever name called].

2.For Liaison Office — a profit making track record during the immediately preceding three financial years in the home country and net worth of not less than USD 50,000 or its equivalent.

iv. An applicant that is not financially sound and is a subsidiary of another company may submit a Letter of Comfort (LOC) (Annex A) from its parent/ group company, subject to the condition that the parent/ group company satisfies the prescribed criteria for net worth and profit.

BRANCH OFFICE

Branch Office in relation to a company, means any establishment described as such by the company. The primary distinction between a branch office and project or liaison office is based on the scope of functions. The functional capability of a branch office is wider than that of the other two – as can be seen in the following discussion.

- Permissible Activities by a branch office:

- Companies incorporated outside India and engaged in manufacturing or trading activities are allowed to set up Branch Offices in India with specific approval of the Reserve Bank. Such Branch Offices are permitted to represent the parent / group companies and undertake the following activities in India:

- Export / Import of goods.

- Rendering professional or consultancy services.

- Carrying out research work, in areas in which the parent company is engaged.

- Promoting technical or financial collaborations between Indian companies and parent or overseas group company.

- Representing the parent company in India and acting as buying / selling agent in India.

- Rendering services in information technology and development of software in India.

- Rendering technical support to the products supplied by parent/group companies.

- Foreign airline / shipping company.

- Normally, the Branch Office should be engaged in the activity in which the parent company is engaged.

b) Retail trading activities of any nature is not allowed for a Branch Office in India.

c) A Branch Office is not allowed to carry out manufacturing or processing activities in India, directly or indirectly.

d) Profits earned by the Branch Offices are freely remittable from India, subject to payment of applicable taxes.

PROJECT OFFICE

Project Office’ means a place of business in India to represent the interests of the foreign company executing a project in India but excludes a Liaison Office. The permission required to set up a project office:

Reserve Bank has granted general permission to foreign companies to establish Project Offices in India, provided they have secured a contract from an Indian company to execute a project in India, and

- the project is funded directly by inward remittance from abroad; or

- the project is funded by a bilateral or multilateral International Financing Agency; or

- the project has been cleared by an appropriate authority; or

- a company or entity in India awarding the contract has been granted Term Loan by a Public Financial Institution or a bank in India for the project. However, if the above criteria are not met, the foreign entity has to approach the Reserve Bank of India, Central Office, for approval.

Setting up of Project Offices by foreign Non-Government Organizations/Non-Profit Organizations/Foreign Government Bodies/Departments, by whatever name called, are under the Government Route.

Accordingly, such entities are required to apply to the Reserve Bank for prior permission to establish an office in India, whether Project Office or otherwise.

LIAISON OFFICE

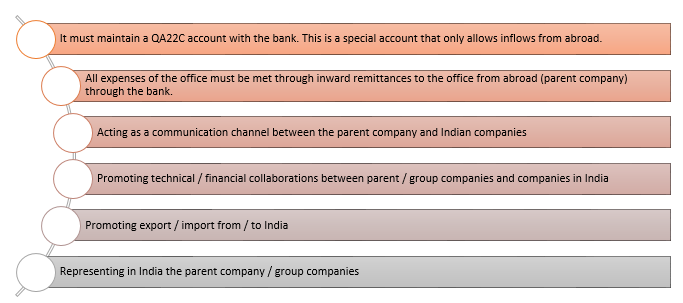

The Foreign Exchange Management Act (FEMA) defines Liaison Office as

“a place of business to act as a channel of communication between the Principal place of business or Head Office by whatever name called and entities in India but which does not undertake any commercial / trading / industrial activity, directly or indirectly, and maintains itself out of inward remittances received from abroad through normal banking channel”.

The role of a Liaison Office is limited to collecting information about possible market opportunities and providing information about the company and its products to prospective Indian customers. Permission to set up such offices is initially granted for a period of 3 years and this may be extended from time to time by an “AD Category I bank”.

A Liaison Office can undertake the following activities in India:

Activities that cannot be undertaken by a liaison office in India:

- Any income generating business activities, which may include:

- Export/import of goods

- Domestic sale and purchase of goods

- Rendering any professional or consultancy services

- Payment of dividend

- Borrowing/ Lending money

- Any other activity which generates income

Steps to set up a liaison office

- Designate a Bank and branch where your account will be opened (post approval) who will be an Authorized Dealer Bank (AD Bank) for your Liaison Office in India

- File an application with all necessary documents to the Reserve Bank of India (RBI) through the AD Bank

- Obtain approval of RBI

- Apply to ROC to obtain a “Certificate of Establishment of Place of Business in India”

- Apply for registration for PAN with Income Tax Authority

- Apply for registration for TAN with Income Tax Authority

- Open account with Bank and to obtain account number

- Obtain registration under Shop and Establishment Act (depends on location)

- Obtain registration under Professional Tax (depends on location)

- Obtain Import Export Code (if samples have to be imported)

Typically, for established foreign businesses looking to set up their business in India as fast as possible, the liaison office option is usually the quickest and cheapest, as all other options involve significant capital and variable expenditures.

The validity period of an LO is generally for three years, except in the case of Non-Banking Finance Companies (NBFCs) and those entities engaged in construction and development sectors, for whom the validity period is two years only. The validity period of the project office is for the tenure of the project.

Arrangement with AD Category-I Bank

The pre-requisite for a foreign entity who is desirous of operating as an OPGSP is to open a liaison office in India with the approval of the RBI. Subsequently, the OPGSP is required to enter into an arrangement with any AD Category-I bank. Further, the AD Category-I banks have to report the details of each such arrangement as and when entered into.

As per the RBI directions, separate export and import collection accounts have to be maintained by the Bank. Further, it is at the discretion of the Bank to offer the facility to repatriate export related remittances or the facility of payment for imports or both.

In case of import transactions, the Bank hold balances in the Import Collection account and remit the payments directly to the respective overseas exporter’s account immediately on receipt of funds from the importer. There are restricted debits and credits from this account.

In case of export transactions, AD Category-I banks providing such facilities opens a NOSTRO collection account for receipt of the export related payments. The balances held in the NOSTRO collection account are repatriated to the Export Collection account in India and then credited to the respective exporter’s account with a bank in India immediately on receipt of the confirmation from the importer. The OPGSP Export Collection account also allows only permitted debits and credits.

Since, the trail of import and export transactions are carried out separately through the respective accounts, there does not seem any mandatory requirement for the OPGSP to enter into an arrangement with a single AD Bank.

Hence, in our opinion, the OPGSP may enter into arrangement with more than one AD Bank for import and export transactions respectively.

Compliance Requirements

There are various ongoing reporting requirements for a LO:

- Reporting to RBI about address and others – the LO has to report its office address to the RBI within 6 months of approval. It also has to report RBI about its Permanent Account Number (PAN) and “Certificate of Establishment of Business Place in India” issued by office of ROC.

- Annual Activity Certificate – the LO has to obtain Annual Activity Certificate from practicing Chartered Accountant and to file the same with the following;

Authorized Dealer Bank

Director General of Income Tax (International Taxation)

- Return with ROC – the LO is required to file the following: annual receipt and payment statement, an assets and liabilities statement duly audited by practicing local Chartered Accountants to the office of Registrar of Companies (ROC); along with the latest consolidated financial statement of parent company (duly notarized and certified by Indian Embassy / Consulate office that has proper jurisdiction in the office location of the parent company). If the language of the parent company is other than English, then this will have to be translated by certified translator before starting the process of notarization and certification. Apart from the financials, LO must also provide the list of all place of business, along with copy of approval obtained if any. ROC filing has to be done before 6 months from the date of closure of books of accounts of LO

Renewal of registration

Initial approval to set up an LO is granted by RBI to establish your India Liaison office for a 3-year period. If desired, your LO can apply for extension of the same to its authorized dealer Bank. The AD Bank, in consultation with RBI, has the power to grant an extension for a further period of 3 years (subject to confirmation of certain compliance requirements). The LO should apply for extension at least 1 to 2 month before the expiry of the initial time period.

Closing a Liaison Office in India

Once you decide to close your operations – usually because you now need a more extensive set up in India – then you need to wind it up properly so that it doesn’t have unintended consequences on future operations and any new companies you have registered or partnerships you are getting into.

Closure of your LO needs to be done with ROC and with RBI:

ROC

- Board Resolution passed by the parent company with intention to close the LO in India

- Identify a date of closure of LO activity

- Terminate employment contract(s) with Employees and complete full and final settlements

- Obtain a Board Resolution for closure of the LO and empowering authorized person to file application with ROC

- File an e-form with ROC and obtain approval of ROC

RBI

- Board Resolution passed by the parent company with intention to close the LO in India

- Copy of original approval letter granted by RBI along with Extension letter granted if any

- Auditor’s certificate

- Confirmation that no legal proceedings are pending and no legal impediment to remittance

- Report from ROC or closure of registration with ROC

- Any assets that the LO is holding (e.g. computer, laptop, car etc.) in its books need to be transferred before applying for the closure of the LO with ROC and RBI. These can be transferred by sale to a Joint Venture or Wholly Owned Subsidiary of the parent company in India. However, RBI approval is required before any transfer of assets following due process of law.

- Before filing your application for closure with ROC/RBI, ensure that any reporting has been taken care of already by your LO. During closure with RBI, request your AD Bank to remit any money left in the account to your promoter company and only after that is done then you can close the Bank Account.

Applicability of the Companies Act:

The branch and liaison offices set up in India by a foreign entity is considered to be a foreign company as per the Companies Act.

Section 2(42) of the Companies Act, 2013 defines a foreign company as-

“any company or body corporate incorporated outside India which,—

- has a place of business in India whether by itself or through an agent, physically or through electronic mode; and

- conducts any business activity in India in any other manner.”

Further, the Companies (Registration of Foreign Companies) Rules, 2014 defines the meaning of electronic mode as-

“carrying out electronically based, whether main server is installed in India or not, including, but not limited to –

- business to business and business to consumer transactions, data interchange and other digital supply transactions;

- offering to accept deposits or inviting deposits or accepting deposits or subscriptions in securities, in India or from citizens of India;

- financial settlements, web based marketing, advisory and transactional services, database services and products, supply chain management;

- online services such as telemarketing, telecommuting, telemedicine, education and information research; and

- all related data communication services,

whether conducted by e-mail, mobile devices, social media, cloud computing, document management, voice or data transmission or otherwise”.

Therefore, the sections 380 to 386 and sections 392 and 393 of the Companies Act, 2013 shall apply to the branch office/liaison office set up in India. Also, any document to be delivered by the Foreign Company to the Registrar shall be delivered to the Registrar having jurisdiction over New Delhi.

Differences between Liaison office and Branch office:

| Basis | Liaison office [LO] | Branch office [BO] |

| Type of activities to be undertaken | Can undertake only liaison activities. | Should be engaged in the activity of the parent company. |

| Permitted activities | · Acting as a communication channel between the parent company and Indian companies

· Promoting technical / financial collaborations between parent / group companies and companies in India · Promoting export / import from / to India · Representing in India the parent company / group companies |

· Export / Import of goods.

· Rendering professional or consultancy services. · Carrying out research work, in areas in which the parent company is engaged. · Promoting technical or financial collaborations between Indian companies and parent or overseas group company. · Representing the parent company in India and acting as buying / selling agent in India. · Rendering services in information technology and development of software in India. · Rendering technical support to the products supplied by parent/group companies. · Foreign airline / shipping company.

|

| Functional Capability | Narrow, as can undertake only limited activities. | Wide, as are permitted to undertake the activities as mentioned above. |

| Prohibited Activities | Cannot undertake any business activities in India. | Not allowed to carry manufacturing/processing activities in India. |

| Criteria for setting up the office | · Profit making track record during the immediately 3 financial years in the home country

· Net worth not less than USD 50,000. |

· Profit making track record during the immediately 5 financial years in the home country

· Net worth not less than USD 100,000. |

| Permitted incomes | Cannot earn any income in India. | Can generate income in India. |

| Meeting of expenses | The expenses of a liaison office is to be met through inward remittances of foreign exchange from its Head Office. | The expenses of a Branch Office is to be met either out of the funds received from the Head office or through the income generated by it. |

| Repatriation of money | Money to be repatriated only on closure of LO. | Profits to be repatriated to the parent company after payment of applicable taxes. |

Conclusion

Foreign entities extending their reach to the Indian markets need to set up a subsidiary or a branch or liaison office in India. Depending upon the taxation aspects and certain other requirements, the foreign entity may decide upon the structure of its formation i.e., as a subsidiary or a branch or a liaison office. If the aim of the foreign entity is mainly to extend its reach to India, then it may set up a branch or a liaison office. Setting up of a branch office is the most viable option, in case the foreign entity wants to carry on business operations in India. However, if the foreign entity wants only a communication channel, then it may set up a liaison office in India. This latter route often provides the quickest and cheapest way for foreign entities to kickstart their business in India. Further, the office so set up is considered as a foreign company and must comply with the requirements of the various applicable provisions of the Companies Act.

[1] https://www.rbi.org.in/scripts/BS_ViewMasCirculardetails.aspx?id=9861

The blog was really helpful and easy to understand. I’m hoping you’ll carry on to add blogs.

I completely hope you continue to post blogs because the blog was quite valuable in many ways and was very simple to understand.