Recent Developments in Corporate Laws

In its stride to achieve transparency, good governance, and ease of doing business, the Government has time and again introduced amendments, proposed new ideas in the corporate laws. The very recent example of such changes are (a) Changes in RPTs proposed in LODR; (b) Minority Squeeze outs under Companies Act; and (c) introduction of Winding-up Rules, 2020.

In light of the these amendments/ proposed amendments, it becomes important to understand its impact on the already existing set-up. A brief analysis of the aforementioned topics has been discussed here

Comparative Analysis of provisions enabling majority shareholders to squeeze out minorities

Harshil Matalia, Executive, Vinod Kothari & Company

Introduction

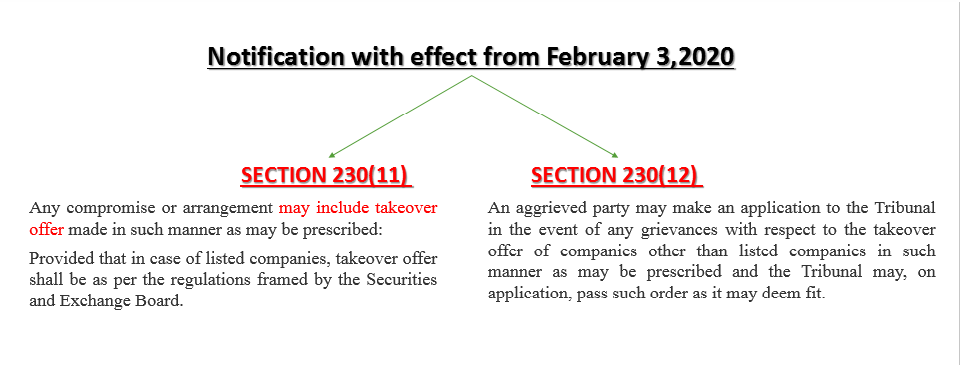

Squeezing out minority shareholders has gradually become an area of intense interest and scrutiny. With the recent set of notifications, Ministry of Corporate Affairs (MCA) has opened yet another way of squeezing out minority shareholders. The MCA has recently notified[1] sub section (11) and (12) of section 230 of the Companies Act, 2013 (‘Act’) on 3rd February, 2020 (effective from the date of notification itself), whereby power has been given to the majority shareholders holding atleast 3/4th of the share capital of the target company to enter into arrangement for acquisition of any part of the remaining shares of the target company.

While section 236 of the Act specifically provides for squeezing out of minority shareholders, the prerequisite of holding atleast 90% of the share capital is a challenge to implement. Whereas, with the notification, those holding atleast 75% can move ahead with the proposal before the NCLT via Scheme and can acquire the balance by offering a fair price determined by the Registered valuer.

The term ‘squeeze out’ reflects a situation whereby controller shareholders undertakes a transaction to forcibly acquire remaining shares of a company. There are number of methods provided in the Act through which minorities can be squeeze out by majorities, viz. reduction of share capital, consolidation of shares etc.

This write up is an attempt to analyse the implementation of the recently notified provisions and a brief comparison of the same with the existing options of squeezing out minority shareholders.

An Overview of Section 230

Section 230 of the Act provides for any compromise and arrangement between shareholders or creditors of a company with the company pursuant to a scheme. The company or any shareholder or creditor or liquidator (in case the company is under liquidation) can file application before the National Company Law Tribunal (NCLT) for the approval of the scheme of compromise or arrangement along with the documents as provided under rule 3 of the Companies (Compromises, Arrangements and Amalgamations ) Rule, 2016.

Approval from at least 90% of shareholder and creditors of applicant companies will enable the companies to get dispensation from the NCLT convened meeting, otherwise, dual approval as per section 230 (6) of the Act will be required, which is ‘majority of persons representing 3/4th in value.

Further, the Act also provides for sending of a copy of application to all the regulatory authorities, such as Registrar of Companies, Central Government (power delegated to Regional Director), Official Liquidator, Income Tax Authorities, Securities and exchange board of India (in case of listed companies), CCI and Reserve bank of India (in case of NBFC, for inviting their objection, if any on the proposed scheme. In consideration of all the respective Tribunal can allow the scheme. The scheme, once approved by the Tribunal, shall be binding on the company, all the shareholders, creditors, and in case of company being wound up, on the liquidator and the contributories of the company.

Proviso to section 230 (4) provides for right to object to the shareholder holding 10% of the share capital of company either individually or together with other shareholders; and the creditors holding 5% of the outstanding debt either individually or together with other creditors.

The enabling notifications[2] provides for ‘takeover offer’ by the shareholders holding at least 3/4th of the shares of a company to the remaining shareholders, which means shareholders holding 75% or more of the issued share capital of the a company can now enter into an arrangement with the target company to acquire remaining shares by offering them the price determined by the registered valuers. While the other compliance as set out in section 230 of the Act will remain same for the scheme involving takeover offer, the applicant shall additionally be required to deposit 50% of the offer price in a separate bank account after getting requisite approval from the shareholders and creditors but before getting approval from the Tribunal.

In addition to the right to object u/s 230 (4), further liberty has been given to the aggrieved party, other than listed companies, to make application before the NCLT in case of any grievances with the said takeover.

Analysis of acquisition of minority shareholding in terms of section 236

Section 236 empowers the registered holders holding at least 90% of the issued share capital of a company, either individually or along with person acting in concert, by virtue of:

- an amalgamation,

- share exchange,

- conversion of securities or

- for any other reason

to first intimate the company regarding their intention to buy the remaining shares or part thereof, then to make offer to the minority shareholders at a price determined by the registered valuer and finally getting the possession of the shares by depositing the amount equal to the value of shares to be acquired in a separate bank account. Alternatively, the minority shareholders may also offer the shares to the acquirer at a price determined on the basis of valuation by a registered valuer in accordance with prescribed rules.

However, in the practical scenario, the section fails to achieve its objective of releasing the minority shareholders as the section does not clarify whether upon receiving such an offer the minority shareholders or the Acquirer is obligated to sell or buy the shares, and no specific timelines have been prescribed for acceptance of such an offer or for the tender of shares. Further, the instance where the shares are held in demat form, has also not been considered.

The process under section 236 can be seen below:

Other methods of acquiring minority shares under the Act

Apart from the transactions mentioned above, there are several other methods available to implement squeeze out minority shareholders within the Act, such as consolidation of shares, reductions of share capital etc. out of which, most commonly used method is reduction of share capital. However, all the provisions have their own benefits and lacuna’s. The brief overview of the said transactions are as follows:

Consolidation of shares:

Consolidation of shares means consolidating nominal value of shares that results into decrease in the number of shares with increase in nominal value of each share. For example 100 shares of face value of Rs. 10 each may be consolidated into 1 share of face value of Rs 1000 each. Consolidation is also known as reverse stock split, which is the effective tool by which a company can restructure its capital and can eliminate minority holding with the approval of Tribunal in terms of section 61 (1) (b) of the Act and Rule 71 of the NCLT Rules, 2016.

Reduction of share capital:

A company limited by shares can reduce its share capital through: (a) reducing/extinguishing its liabilities on unpaid share capital; (b) with or without extinguishing or reducing its liabilities on any shares which is lost or is unrepresented by its existing assets; or (c) with or without extinguishing or reducing its liabilities on any shares which is in excess of its requirement. Section 66 of the Act provides for the reduction of capital by a company with the approval of Tribunal, only if it is not defaulted in repayment of any deposit accepted by it or interest thereon.

Acquiring Minority shareholding in terms of section 235:

An Acquirer/Transferee Company can acquire the shares of Transferor Company under a scheme or contract subject to the approval of holders of minimum 90% of value of shares other than shares already held by Transferee Company or its nominee or its subsidiary companies. Such approval is required to be obtained by Transferee Company within 4 months after making such offer. Upon receipt of the said approval, within 2 months from the expiry of the offer period, the Transferee Company shall give notice to dissenting shareholders by conveying its intention to acquire their shares and the dissenting shareholders may then approach NCLT for seeking remedy within one month from the date of such notice.

The entire process of acquiring the shares from the dissenting shareholders is extensive and time consuming for the acquirer. This makes the process of squeezing out dissenting shareholders unreasonably lengthy.

Conclusion

In conclusion, the notified section has added a way for unlisted companies to eliminate minorities smoothly vide scheme of arrangement which will further boost the dominance of majority over minority. On prima-facie view, one can say that the section seems to have covered the lacuna’s of other squeezing out provisions of the Act, however, the supervisory role of the respective regulatory authorities and the views to be taken by respective Tribunals will decide the materialisation of the notification.

Links to related write ups –

Takeover under Companies Act, 2013- https://vinodkothari.com/2020/02/takeover-under-ca-2013/

[1] http://www.mca.gov.in/Ministry/pdf/Notification_04022020.pdf

Condonation of delay provisions now extended to LLPs

Megha Saraf, Manager | Corporate Law Division

Ministry of Corporate Affairs (“MCA”) vide its recent Notification[1] dated 30th January, 2020 has given a relaxation to all Limited Liability Partnerships (LLPs) by extending the scope of condoning the delay to them in filing applications/ documents to the Central Government/ Registrar. As per the powers conferred upon the Central Government under Section 67 of the Limited Liability Partnership Act, 2008 (“LLP Act”), Section 460 of the Companies Act, 2013 (“Act, 2013”) which provides for condonation of delay has now been extended to LLPs with effect from 30th January, 2020.

A brief of the amendment is provided below:

Existing scope of Section 460 of the Act, 2013

Section 460 of the Act, 2013 refers to condonation of delay of offences in certain cases which provides for the following:

- delay in filing application to the Central Government

- delay in filing any document to the Registrar

In the aforesaid cases, the Central Government may condone the delay after recording the reasons in writing. Accordingly, companies can file e-Form CG-1 accompanied by an application with the Registrar of Companies (RoC) in order to condone the delay that has happened.

Revised scope of Section 460 of the Act, 2013

MCA vide its recent Notification has now extended the provisions of Section 460 to LLPs which would mean that now LLPs also have the option of proceeding before the Central Government on account of any delay in filing an application/ document with the Central Government or Registrar respectively. In absence of any particular section providing for condonation of delay, LLPs may file such application for condonation in e-Form 22 with the Registrar.

It can be said that with such extension of the provisions, the LLPs may now have a chance to rectify and condone the offence committed by them instead of opting for compounding as provided under section 39 of the LLP Act.

[1] http://www.mca.gov.in/Ministry/pdf/NotificationLLP_31012020.pdf

Customary puppets: Meaning of Companies Act expression “accustomed to act”

Vinod Kothari and Pammy Jaiswal

The expression “accustomed to act” occurring with advice, directions or instructions of a person, is not at all new in corporate laws. Such expression was used in the 1956 Act, and has abundantly been used in the various global legislations like the UK Companies Act 1948, UK Act of 2006, Singapore Companies Act, 2006 as well as the Australian Corporation Act, 2001 to name a few other global jurisdictions. However, the provisions of section 185, restricting and regulating inter-corporate lending to directors’ entities, seems to be giving a new significance to this expression, as Explanation (c) below sec 185 (2) uses this term. Questions do arise as to when can it be presumed that the board of one company acts as per directions of another, or any other person? Who establishes this? Are there circumstances where there is presumption as to such customary adherence, or does it have to be purely left to circumstances?

This article explains the concept and seeks to provide a practical guidance as to the meaning of the expression.

Shadow directors:

The most important reason for the law referring to persons in accordance with whose directions the board of a company is accustomed to act, is to refer to “shadow directors”. Shadow directors are persons who are not formally anointed to the board, and yet, either because of their shareholding or their beneficial control over the company, are able to exercise absentee control over the board of the company. Despite such a person not holding the formal position of a director, such person is “deemed director”.

Sec 2 (13) of the 1956 Act sought to include shadow directors, as the definition included a person occupying the position of a director, by whatever name called. Rightly or wrongly, the 2013 Act makes a clear departure from this principle. Sec 2 (34) of the 2013 Act states that a director shall be regarded as such only where he is appointed as such to the Board. In other words, the functional position as a shadow director no more matters: for being regarded as a director, a person has to be appointed to the board.

At the same time, references to the word “officer” and “officer in default”, in sections 2 (59) and 2 (60) of the Act, continue to include references to shadow directors as well. In other words, responsibilities of the law fastening to “officers in default” may include shadow directors too, but the expression “director” cannot be deemed to include reference to a shadow director. The definition of “promoter” in sec. 2 (69), and “related party” in sec 2 (76) also include the reference to shadow directors.

Global position on accustomed to act

Under the UK law:

The UK Companies Act 2006[1] contains elaborate references to “shadow directors”. Sec 251 specifically defines the term as well. Of course, the definition goes no further than stating the most obvious: “In the Companies Act “shadow director”, in relation to a company, means a person in accordance with whose directions or instructions the directors of the company are accustomed to act.” Sub-section (2) makes an exception to following advice given in professional capacity. As is obvious, a shadow director may be either an individual or any other person.

The UK law also makes a specific exception to a holding company – a parent shall not be deemed to be a shadow director of the subsidiary, merely by reason of the board of directors of the parent acting as per the directions or advice of the parent. It is but natural that the board of a subsidiary will act as per the advice of the parent.

Under the Australian Law:

Even though the Australian Corporation Act, 2001[2] do not contain explicit mention of the term shadow director, however, the definition of the term director is clear enough to include and strongly indicate towards a person who even though is not validly appointed as a director but the directors of the company are accustomed to act as per the instruction or wishes of such person

Further, the definition also clarifies that such advice if made on a professional basis will not attract the provisions of a shadow director.

Under the Singaporean Law:

Similarly, the definition of director under the Singaporean Companies Act, 2006[3] contains like provisions as that under the Australian law.

Under the US Law:

The Jamaican Companies Act[4] also defines a shadow director and contains similar provisions as that under the UK law.

Judicial guidelines on identification of shadow directors:

There are several rulings on shadow directors, and in the era where institutional investors continue to exercise control on the strength of shareholders’ agreements, the phenomenon of absentee control on boards of companies continues to get stronger.

One of the classic authorities is Re Hydrodan (Corby) Ltd [1994] BCC 161. Millet J in this ruling gave several indicia of absentee directorship, and said that prima facie, the existence of such relationship has to be proved by the person alleging it. “What is needed is first, a board of directors claiming and purporting to act as such; and secondly, a pattern of behaviour in which the board did not exercise any discretion or judgment of its own, but acted in accordance with the directions of others”. One must stress the factual assertion that the board did not exercise any discretion or judgement of its own.

In Secretary of State for Trade and Industry v Deverell [2001] Ch 340, the scope of the expression “instructions” or “directions” was widened, even to include informal communication. Here, the court came to a finding that the so-called “guidance” given by Mr Deverell gave to his guidance the potency of a instructions or directions. He was listened to and followed. Hence, he was regarded as a shadow director.

Another ruling where the distinction between shadow director and de facto directors has been discussed, and disbanded, is Holland v The Commissioners for Her Majesty’s Revenue and Customs (Appellant) v Holland and another [2010] UKSC 51 .

Quite often, positive as well as negative control is exercised pursuant to commercial contracts or shareholders agreements. It may be interesting to argue whether such rights of positive or negative control would put the controlling party to the position of a shadow director. One such interesting case is Australian ruling in Buzzle Operations Pty Ltd (in liq) v Apple Computer Australia Pty Ltd [2010] NSWSC 233 and [2011] NSWCA 109. Here, the court laid several principles – first, that the directions or instructions by the alleged shadow director must be in relation to board matters, that is, matters requiring decision of board of directors. Second, referring to the test laid by Millet, J in Hydrodan, the court laid here that it is not necessary that the board of the controlled company must not exercise any discretion at all. It is still possible for the board of the controlled company to exercise discretion in matters where there is no direction from the shadow director. Third, there must be a clear causal link between the instructions given by the shadow director, and the actions on the part of the board of the controlled company. Mere commercial pressure is not sufficient. Finally, it is not necessary to ensure that the entire board of the controlled company acts as per directions of the shadow – it is sufficient if a functional majority does so.

Further, in the matter of Vivendi SA v Richards and Bloch[5], reliance was placed in the matter of Secretary of State for Trade and Industry v Deverell to conclude that Mr. Richard and Mr. Bloch have acted against their fiduciary duties and hence are liable under the law.

Who decides whether there is a shadow director:

It is imperative to note the provisions of section 166 (3) which states the following:

“A director of a company shall exercise his duties with due and reasonable care, skill and diligence and shall exercise independent judgment.”

The provisions of this section are explicit to clarify the position of directors and the judgement they are expected to exercise while delivering their obligations in the company. Being appointed by the member of the company, they are reposed with the faith and expectations of the members and thus, stand in a fiduciary capacity. In case, the actions of a director are influenced or instigated by the directions of a third party (not being an advise on a professional basis), the provision of section 166 (3) is said to be breached to call for prosecution on the accused director.

Clearly, it is purely a circumstantial issue as to whether the board of a controlled company is merely acting as a puppet in the hands of a shadow director. There is a basic presumption that a properly constituted board of directors of any company acts as per its own wisdom in the best interest of the company. Directors of every company are presumably aware of their duties, and liabilities in law, and therefore, the presumption to be made at the threshold is that every board is independent, and is not the alter-ego of another person or entity.

If someone alleges that the board is, in fact, accustomed to act as per instructions, the duty of discharging the onus is on the person making the allegation.

Can the holding company be said to be shadow-controlling the subsidiary:

As mentioned above, the UK Companies Act contains a specific exception in case of holding companies. However, the question is, had there been no such exception, is it likely that the board of the subsidiary company will be deemed controlled by the board of the holding company? The holding company’s control over the board of the subsidiary company is a de-jure control. On the face of it, the holding company is the parent, and hence, entitled to both shareholding control as well as management control. The sole purpose of shadow control is to detect and bring on board control which is latent, and not apparent. Surely the control of a holding company does not fall in this category.

Conclusion:

With plethora of duties and liabilities cast upon directors, the erstwhile practice of putting nominees on the board, by institutional investors or other stakeholders, may undergo a change. If control can be exercised without being on board, why be on the board at all? In such a situation, the deliberate deletion of the functional test of directorship in the 2013 Act may be undesirable. However, in application of restrictive provisions such as sec. 185 pertaining to loans to directors, whether a borrower or beneficiary company is shadow-controlled by the lending company or any director of the lending company, is a factual question that will continue to create confusion.

[1] http://www.legislation.gov.uk/ukpga/2006/46/pdfs/ukpga_20060046_en.pdf

[2] https://www.legislation.gov.au/Details/C2018C00031

[3] https://sso.agc.gov.sg/Act/CoA1967

[4] http://www.oas.org/juridico/english/mesicic3_jam_companies.pdf

[5] https://www.casemine.com/judgement/uk/5a8ff74260d03e7f57eaa801