MCA exemption notification paves way for limitless deposits from members, by Vinita Nair

Deposits have always been strictly regulated by all the law makers, be it MCA, RBI or SEBI. Chapter V of Companies Act, 2013 (‘Act, 2013’) read with Companies (Acceptance of Deposits) Rules, 2014 [‘Deposit Rules’] provides the framework for lawful acceptance of deposits by companies. The framework provides list of amounts which do not fall within the meaning of deposits, compliances to be ensured for accepting deposits from members and compliances to be ensured for accepting public deposits by eligible companies.

Exemption under principal notification

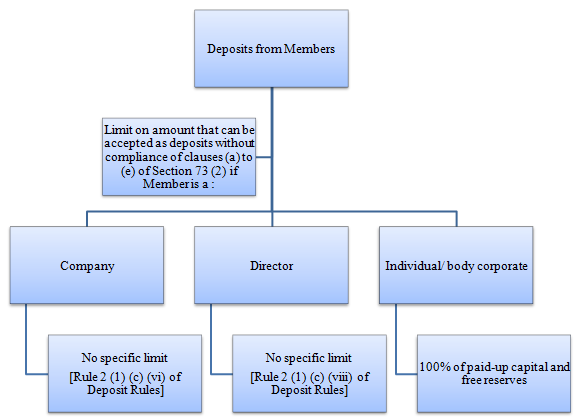

MCA, vide exemption notification dated June 5, 2015 (‘principal notification’) extended exemption from compliance of provisions of clauses (a) to (e) of Section 73 (2)[1], if the said private company accepted from its members monies not exceeding one hundred per cent of aggregate of the paid-up share capital and free reserves, and such company filed the details of monies so accepted to the Registrar in the manner prescribed. So, the exemption even provided for a maximum amount that could be accepted as deposits from members without the requirement to comply with provisions of clauses (a) to (e) of Section 73 (2). However, the private company was exempted

The exemption was subject to a maximum limit of 100% of aggregate of paid-up share capital and free reserves. Private companies were also exempted from the requirement of Section 180.

So, in case a private company intended to raise amount in excess of aforesaid limit from members, following options were available:

Exemption under amendment notification

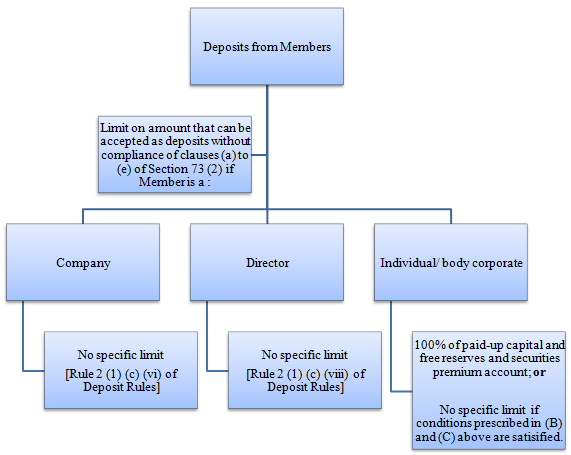

MCA vide notification dated June 13, 2017 (‘amendment notification)’, amended the principal notification to substitute the aforesaid exemption with the following:

“Clauses (a) to (e) of sub-section 2 of Section 73 shall not apply to a private company-

(A) which accepts from its members monies not exceeding one hundred per cent. of aggregate of the paid up share capital, free reserves and securities premium account; or

(B) which is a start-up, for five years from the date of its incorporation; or

(C) which fulfills all of the following conditions, namely:-

(a) which is not an associate or a subsidiary company of any other company;

(b) if the borrowings of such a company from banks or financial institutions or any body corporate is less than twice of its paid up share capital or fifty crore rupees, whichever is lower; and

(c) such a company has not defaulted in the repayment of such borrowings subsisting at the time of accepting deposits under this section:

Provided that the company referred to in clauses (A), (B) or (C) shall file the details of monies accepted to the Registrar in such manner as may be specified.”

By virtue of the aforesaid amendment, a private company can avail limitless deposits if it has not defaulted in filing the financial statements and annual returns with the Registrar and falls under any of the conditions specified in (B) and (C) above. Alternatively, if the member is also a director or relative of a director of a private company or is a company, limitless deposits can be availed pursuant to Rule 2 (1) (c) (viii) and (vi) respectively of Deposit Rules.

So, revised position is as under:

Conclusion

The intent seems to allow limitless deposits from members without compliance of clauses (a) to (e) of sub-section (2) of Section 73 in view of no restriction on borrowing limits under Section 180 of Act, 2013 as well. This provides good scope for members to infuse funds in the company where needed without the requirement to block by subscribing to share capital, so long as the conditions prescribed above are duly met and such private company files particulars of deposits accepted with the Registrar.

—

[1] (2) A company may, subject to the passing of a resolution in general meeting and subject to such rules as may be prescribed in consultation with the Reserve Bank of India, accept deposits from its members on such terms and conditions, including the provision of security, if any, or for the repayment of such deposits with interest, as may be agreed upon between the company and its members, subject to the fulfillment of the following conditions,

namely:—

(a) issuance of a circular to its members including therein a statement showing the financial position of the company, the credit rating obtained, the total number of depositors and the amount due towards deposits in respect of any previous deposits accepted by the company and such other particulars in such form and in such manner as may be prescribed;

(b) filing a copy of the circular along with such statement with the Registrar within thirty days before the date of issue of the circular;

(c) depositing such sum which shall not be less than fifteen per cent. of the amount of its deposits maturing during a financial year and the financial year next following, and kept in a scheduled bank in a separate bank account to be called as deposit repayment reserve account;

(d) providing such deposit insurance in such manner and to such extent as may be prescribed;

(e) certifying that the company has not committed any default in the repayment of deposits accepted either before or after the commencement of this Act or payment of interest on such deposits; and

(f) providing security, if any for the due repayment of the amount of deposit or the interest thereon including the creation of such charge on the property or assets of the company:

Provided that in case where a company does not secure the deposits or secures such deposits partially, then, the deposits shall be termed as “unsecured deposits‘‘ and shall be so quoted in every circular, form, advertisement or in any document related to invitation or acceptance of deposits.

by Vinita Nair (vinita@vinodkothari.com)

Leave a Reply

Want to join the discussion?Feel free to contribute!