Accounting treatment of securitization transactions undertaken by financial entities in India

By Vijaylakshmi Agarwal & Kanishka Jain, (finserv@vinodkothari.com)

1. Introduction

Presently, the accounting treatment for securitization transaction is unclear and ambiguous despite a clear convergence with IFRS. The accounting principle for securitization was contained in AS 30 (based on IAS 39). The ICAI had originally promulgated AS 30 (based on IAS 39) in the year 2009, but was kept in abeyance, and subsequently repealed[1], while IND AS 109 is applicable from the year 2018. Therefore currently, there is no standard as such dealing with securitization for such companies on which IFRS is not applicable. Therefore for the interim period i.e. from 2015 to 2018, there are no standards governing the accounting for securitization in existence.

While the transition date for IFRS starts with the next fiscal year i.e. 1/4/2017 and financial sector entities getting covered in the Phase 1(discussed subsequently in the article) will have to in-parallel adopt IFRS. So it is necessary on the part of the entity to understand the implication of the transition and adoption of IFRS that will be on the securitization transaction. Thus, in this article we have dealt with the transition effect and accounting treatment of securitization transaction under the IFRS regime.

2. Executive Summary

The key accounting aspects for accounting treatment for securitization resides in the following pints:

- De-recognition – that is, whether the securitized asset [Collateral Pool] will be put off the balance sheet of the originator. The term is used for ceasing to recognize a financial asset or financial liability in the entity books.

- Profit recognition – that is, whether there will be gain/loss at the time of sale of the Collateral Pool

- Consolidation – whether the special purpose vehicle which holds the legal rights to the Collateral Pool will be consolidated with the originator/any other investor.

The accounting principles generally require, for de-recognition purpose, to consider whether the transfer is to a consolidated entity or not. Therefore logically the first step is to determine whether the sale is to an entity which is getting consolidated or not. The table below summarizes the accounting for securitization in brief and there is more detailed discussion in the subsequent part of the article.

| Before moving to provide accounting treatment to securitization transactions, primarily two questions are required to be answered:

a) Will the securitization entity require consolidation with transferor? b) Has the sale been done as per the IFRS 9? The answer to above questions together is to be understood for determining the accounting treatment of the transaction:

|

3. Accounting for Securitization

3.1. Current Accounting standards for securitization in India

First and foremost let us understand the prevalent standards relating to the securitization transactions in India. Presently the country is witnessing changes in accounting laws, with shift to IND AS in phased manner, there are two sets of accounting standards that are in existence a) Accounting Standard (“AS”) b) Indian Accounting Standard (“IND AS”). The Indian Accounting Standards are required to be followed by only select companies as prescribed by MCA. Therefore there are two sets of accounting standard which is required to be followed. Accounting for securitization is dealt with by:

- AS 30,31 and 32 (for companies following AS)

- IND AS 109 (for companies following IND AS)

The ICAI had originally promulgated AS 30 (based on IAS 39), which was kept in abeyance, and subsequently repealed[2], while IND AS 109 is applicable from the year 2018 (for financial sector entities). Therefore currently, there is no standard as such dealing with securitization for such companies on which IND AS is not applicable. The table below summarizes the above discussion:

| Standard | Issued in the year | Status |

| AS 30,31 and 32 | 2009 | Withdrawn |

| IAS 39 based IND AS 39 | 2014 | Not applicable (Superseded by IND AS 109) |

| IND AS 109 | 2015 | Applicable (only on select companies) |

3.2. Current accounting treatment in India

The accounting for the different aspects of the securitization transaction done is as follows:

- De-recognition – The market practice is to go by true-sale. Every securitization transaction is presumably a true sale and is backed by a legal opinion saying so. Therefore, practitioners treat the legal sale as evidence of off-balance sheet treatment.

- Profit recognition – Securitization guidelines of 2012 provide that the originator shall not recognize gains on sale even if the gains are encashed upfront. The originator will park the same in Gains on sale as a liability and release the same linearly based on the receivables accruing.

- Consolidation – Accounting standards [AS 21] is currently based on voting rights as the basis of consolidation. Since SPVs are structured so that voting rights are not exercisable by the originator, transactions never lead to consolidation of the SPV with the originator.

3.3. Securitization accounting under IFRS (IND AS)

India is to align itself with IFRS in a phased manner over a period of time. The financial entities are required to adopt IND AS starting from the financial year 2018-19. The adoption phase has been summarized below:

Phase 1:

- NBFCs having a net worth of 500 crore INR or more.

- Holding, subsidiary, joint venture or associate companies of the above, other than those companies already covered under the corporate roadmap announced by MCA.

- Comparative information required for the period ending 31 March 2018 or thereafter.

Phase 2:

- NBFCs whose equity and/or debt securities are listed or are in the process of listing on any stock exchange in India or outside India and having a net worth less than 500 crore INR.

- NBFCs that are unlisted companies, having a net worth of 250 crore INR or more but less than 500 crore INR.

- Holding, subsidiary, joint venture or associate companies of companies covered above, other than those companies already covered under the corporate roadmap announced by MCA.

- Comparative information required for the period ending 31 March 2019 or thereafter.

3.3.1 Relevant IFRSes

The relevant IFRSes for securitization accounting is as follows:

- IFRS 9 for principles and conditions of de-recognition

- IFRS 10 for consolidation of the SPV

- IFRS 12 for certain disclosures as may be applicable to an unconsolidated structured entity

3.3.2 De-recognition (IFRS 9) (IND AS 109)

The key issue is whether the transaction will at all qualify for de-recognition.

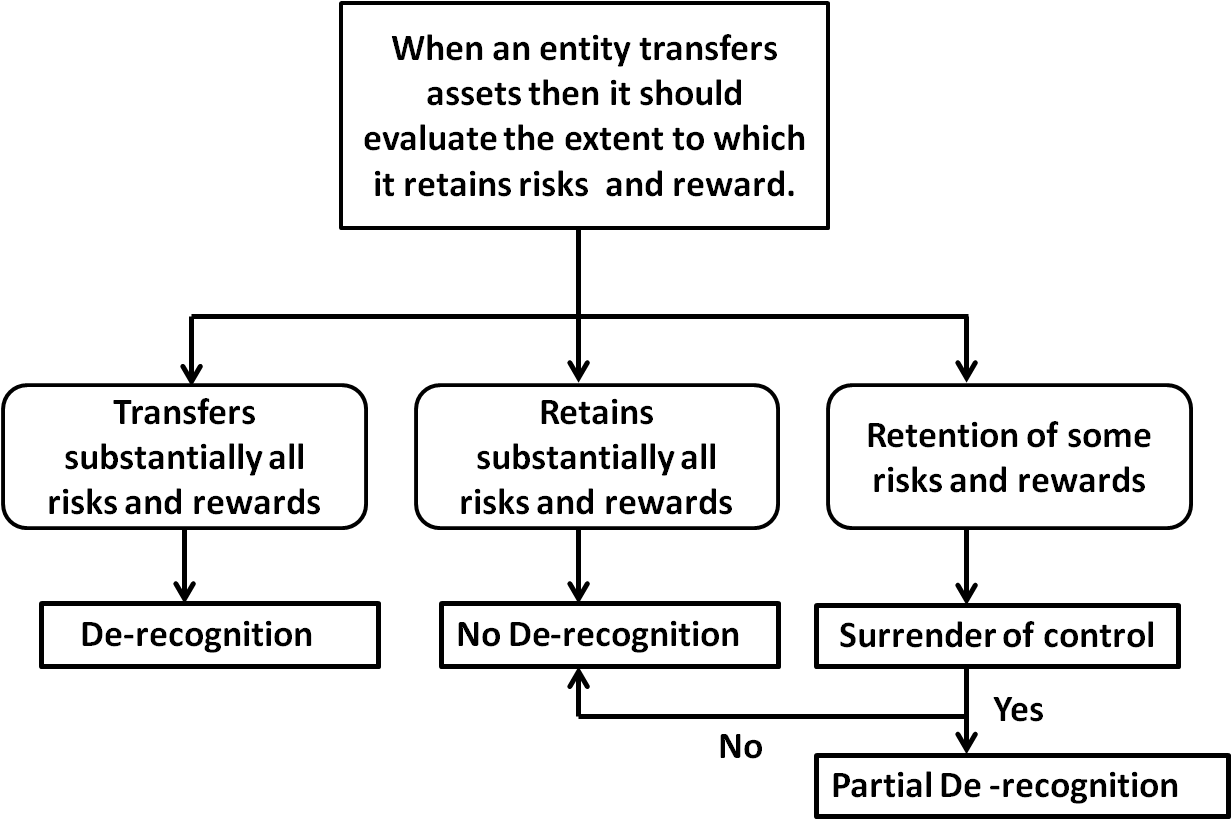

The conditions of de-recognition are stated in Para 3.2.6 of IFRS 9. There may be essentially 3 situations:

- Transfer of substantially all risks and returns – de-recognition

- Retention of substantially all risks and returns – no de-recognition

- Retention of some risks and returns – however, surrender of control – partial de-recognition.

The dynamics below appropriately explains the above written text:

In order to qualify even for a partial de-recognition, there has to be a significant (that is, more than nominal) transfer of risks and returns. We need to understand two key elements:

- Risks

- Returns

Risk, in case of typical securitization transactions, is the exposure to credit risk of the transaction. Return is understandably a compensation for the risk, and is mostly represented by the excess spread. Understandably, all the risks and returns were with the originator prior to the transaction of securitization. One has to compare the impact the transaction makes on the originator’s exposure to risks and returns after the transaction, so as to see whether there is a significant transfer of risks/returns.

3.3.3 Consolidation and structured entity disclosures (IFRS 10 & 12) (IND AS 110 & 112)

If the transaction qualifies for de-recognition, the question of consolidation or disclosures as required in case of structured entities under IFRS 12 will arise.

In all likelihood, securitization SPV will qualify for a non-substantive structured entity under IFRS 12. There is no role of voting rights, and there are generally no activities to be carried out in an SPV. The transaction is mostly an auto-pilot. These entities are squarely covered by IFRS 12.

On the other hand, if there is an on-going selection of assets (for example, in case of revolving transactions), it is likely that the transaction is covered by IFRS 10.

If IFRS 10 is applicable, and the transaction has been able to achieve de-recognition under IFRS 9, then consolidation may be done on the following principles:

- The principles of consolidation are two fold –exposure to risks and ability to control. Between the two, control is most important.

- Control means control over relevant activities – relevant activities mean those which decide the economic results of the enterprise or activity carried by the entity.

- In case of securitization vehicles, mostly, there is no activity as such carried by the vehicle. However, the returns or risks of the entity are affected by the selection of the assets. If the selection of assets is done by the originator, then it is likely that it may be argued that the originator has control over the entity, and therefore, the entity may require consolidation back with the originator.

- On the contrary, if it can be established that the control, that is, selection of assets, etc., are based on the decisions of an independent expert [say an investor representative] then the transaction may avoid control with the originator. Note that typically, the trustee of the SPV is independent, and there are several legal controls with the trustee rather than with the originator.

- In short, structuring of the SPV and the transaction may avoid possibility of consolidation.

- Eventually the transaction will come under IFRS 12 requiring disclosures.

| Note: If the whole understanding and logic of IFRS 9 and 10 is extended to the Non Performing Loans (NPLs) securitization, there appears a major debacle coming through. Banks offload their junk assets (NPLs) through securitization trusts formed by the Asset Reconstruction companies (ARCs). These securitization trusts issue security receipts (“SRs”) to the investors backed by the NPLs. Generally 85% of the SRs are subscribed by the originator. Now going by the risk and reward criteria, the risk necessarily stays with the originator only. Therefore under the IFRS provisions, there may not be any de-recognition at all. This will thus require the banks to maintain continued provisions with regard to the NPLs and there may not be any relief even if the asset is transferred to the ARCs. Therefore the whole edifice on which the ARCs are working gets frustrated. |

3.4. Impact of transition to IFRS on securitization transaction

As discussed above the financial sector entities are required to adopt IFRS (IND AS) from the financial year 2018 i.e. from 1st April 2018. Therefore there is a shift from AS to IND AS from the above financial year and consequently differences will have to be adjusted for. This period is known as transition period. So a question arises that what would happen to transactions undertaken prior to, on and after the transition date?

To understand the implication of the above question we will have to first understand the meaning of transition date as given in IND AS 101 or IFRS 1. IND AS 101 or IFRS 1 contains the provision guiding the first time adoption of IND AS financial statements and as per the provisions, transition date happens to be earliest date of the previous financial year construed from the year in which the entity is required to follow IFRS. Thus to illustrate, if a financial entity is required to follow IFRS from the year 1/4/2018 – So transition date for the entity will be 1/4/2017. Therefore the opening balances as on 1st April 2018 are required to be IFRS compliant, and therefore, effectively, the entity has to in-parallel adopt IFRS in 2017-18 as well. So there is great impact of transition to IND AS on the financial sector entities from 1/4/2018.

Now coming to the effects on accounting treatment of the securitized transaction, there seems to be a major impact affecting the financial entities. The whole idea of securitization is to achieve off-balance sheet accounting treatment. But the same is getting frustrated under the IFRS regime as it will no more be possible for the entities to put assets off-balance sheet. Reading Para B2 and Para B3 of the IFRS 1 or IND AS 101, it is very clear that in respect of de-recognition of financial assets as per existing Indian GAAP, the assets will still be on the balance sheet from the year 2017-18 if de-recognition as does not meets the criteria as set out by IND AS 109.

As per para B2, a first time adopter of IND AS is required to adopt the de-recognition requirements in IND AS 109 prospectively for transactions occurring on or after the date of transition to IND Ass. Hence financial assets and liabilities that has been derecognized by an entity in accordance with the erstwhile Indian GAAP, as a result of transaction that occurred before the date of transition to IND AS, it shall not recognize those assets and liabilities in accordance with IND ASs, unless they qualify for recognition as a result of a later transaction or event. Simply put the following situation will arise:

| Before 31/3/2017 | After 1/4/2017 | After 1/4/2018 | |

| De-recognized | Grandfathering provisions will apply and no subsequent recognition as per IFRS even if the transfer do not qualify for de-recognition post IFRS adoption. | The assets will be put off-balance sheet for the financial year 2017. However the assets will be on balance sheet again on account of transition to IFRS, if the de-recognition do not meet criteria as specified in IFRS 9 and no consolidation is required as per IFRS 10. | The Assets will be put off-balance sheet only if the respective provisions of IFRS 9 and 10 are followed. |

4. Conclusion

Convergence with IFRS will have a huge impact on the financial statements of the entity. It will not only change the perspective of accounting for securitization but also the very objective of accounting in the country. Presently, in the absence of any accounting standard governing the accounting for securitization, assets are taken off books once there is legal sale or true sale without giving any consideration to transfer of risk and rewards while voting rights determine the position for consolidation. However, post IFRS convergence, the asset will be only put off-books only if:

- there is a whole or substantial transfer of risk or reward, and

- the originator does not control the SPV and is not exposed to the variable interest in the SPV.

Thus it is unlikely that any asset may go off the books in the IFRS regime and therefore achieving off-balance sheet may not be possible. This would have a hard hitting effect on the securitization of NPLs, which will stay of the books despite being transferred to the ARCs. Thus it seems the whole idea for securitization gets frustrated. However, it will be interesting thing to watch as to what carve outs would be given to the financial sector entities and how does the convergence fares in the coming years.

[1] http://resource.cdn.icai.org/43918asb33625.pdf . Two primary parts of IAS 39 dealt with de recognition, and accounting for derivatives. As regards accounting for derivatives, ICAI has subsequently issued a Guidance Note on Accounting for derivatives.

[2] http://resource.cdn.icai.org/43918asb33625.pdf . Two primary parts of IAS 39 dealt with de recognition, and accounting for derivatives. As regards accounting for derivatives, ICAI has subsequently issued a Guidance Note on Accounting for derivatives.

Leave a Reply

Want to join the discussion?Feel free to contribute!