Attributes of a Resolution Plan

Attributes of a Resolution Plan

Other ‘I am the best’ presentations can be viewed here

Our other resources on related topics –

Other ‘I am the best’ presentations can be viewed here

Our other resources on related topics –

-Sikha Bansal

Below we provide a quick snapshot of the extant provisions of the insolvency framework in India vis-a-vis Minority Shareholders, in light of related laws and judicial developments so as to assess their rights and standing in the current insolvency ecosystem –

Parth Ved, Executive

The Standing Committee on Finance (“Standing Committee”), on 3rd August, 2021, issued its Report on Implementation of Insolvency and Bankruptcy Code – Pitfalls and Solutions[1] wherein it has recommended the deletion of and suitable amendment in Regulation 32(e) and Regulation 32(f) of the Insolvency and Bankruptcy Board of India (Liquidation Process) Regulations, 2016 (“Liquidation Process Regulations”) respectively, which deal with sale of the corporate debtor or its business as a going concern.

The said recommendation comes in light of the mismatch of sorts between the Code and the Liquidation Regulation w.r.t. closure of business vide going concern. In this article, we discuss and analyse the recommendations made by the Standing Committee, and present our case as to why such recommendation may not be in the interest of the Code and its stakeholders.

Before delving further into the rationale of the said recommendation, and whether such recommendations ought to be implemented, it is important to understand what is a going-concern – suggestive of its name, a ‘going concern’ indicates continuity or the ability of the business to be carried out as is. Hence, in simple terms a ‘Going Concern sale’ (GCS) means the sale of all the assets, tangibles or intangibles and resources, needed to continue to operate independently a business activity which may be whole or a part of the business of the corporate debtor, without values being assigned to the individual asset or resource.

Interestingly, in a GCS, the legal entity of the company also forms part of the ‘property’ being transferred. Hence, the sale of an entity as a going concern implies that the entity would be functional as it would have been prior to initiation of sale, retaining the same name and style[2].

The power to sell the assets of the corporate debtor as a going concern was added to Regulation 32 of the Liquidation Process Regulations vide amendment dated October 22, 2018. Consequently, Regulation 32 was substituted with the following:

“32. Sale of Asset etc. –

The liquidator may sell –

(a) an asset on a standalone basis;

(b) the assets in a slump sale;

(c) a set of assets collectively;

(d) the assets in parcels;

(e) the corporate debtor as a going concern; or

(f) the business(s) of the corporate debtor as a going concern:

Provided that where an asset is subject to security interest, it shall not be sold under any of the clauses (a) to (f) unless the security interest therein has been relinquished to the liquidation estate.”

The Standing Committee has proposed to delete clause (e) and consequently amend clause (f) stated above in light of the stand taken by the Hon’ble Principal Bench of NCLT in the matter of Invest Assets Securitisation & Reconstruction Pvt. Ltd vs. Mohan Gems & Jewels Pvt. Ltd.[3] stating that liquidation requires dissolution under the Insolvency and Bankruptcy Code, 2016 (IBC) and hence regulations that provide for liquidation as a going concern are ultra-vires the provisions of the Code and that the legislation has created further uncertainty. The said order, as well as the recommendation of the Standing Committee crops from the supposed reason that a liquidation process shall mandatorily end by dissolution.

With this pretext, the Author humbly deviates from the views put forth by the Standing Committee, and suggests that ruling out the option of a going-concern, merely on grounds of non-alignment in the extant provisions would be disproportionate, and hence, undesirable.

Below we discuss several grounds / reasons which further prove a good case for a going-concern sale under liquidation.

It is a common economic understanding that sum of parts is better than sum of the parts; and it is by virtue of such principle that going-concern values are generally in excess of value of individual assets. The various assets, stitched together as one, constitute a much greater value than the same assets in isolation.

As such, selling assets on a piece-meal basis might not be lucrative for the buyers due to the loss of synergic benefit arising from purchasing a going concern leading to an ultimate loss to the creditors of the corporate debtor. This is in addition to the fact of loss of jobs of several employees of the corporate debtor which might have been saved in case of sale as a going concern.

Recognising this, various Adjudicating Authorities have, in the past, allowed the sale of the corporate debtor as a going concern for value maximisation. In the matter of M/s. Gujarat NRE Coke Limited[4], the Hon’ble NCLT, Kolkata Bench held:

“The Liquidator shall try to dispose of the Corporate Debtor company as a going concern after publication of notice in newspaper with the reserve price which shall be equal to the total debt amount including interest and maximum period applicable for trying the sale of the Corporate Debtor as a going concern will be only three month from the date of the order if the process of sale as a going concern is failed during this period, then process of the sale of the assets of the company will be according to the provisions of sale of asset of the Corporate Debtor prescribed under section 33, Chapter VI of the Insolvency & Bankruptcy Board of India (Liquidation Process) Regulations, 2016. In case it is not concluded within this period, the order of this Court directing the sale of the company as a going concern shall stand set aside and corporate debtor to be liquidated in the manner as laid down in Chapter III of the Liquidation process provided in Insolvency & Bankruptcy Code.”

Further, it is commonly observed that NCLTs across jurisdictions have followed the practice of directing liquidators to endeavor a GCS prior to other modes of sales envisaged under the Liquidation Process Regulations.

A liquidator may find it difficult to complete the sale of all the assets of the corporate debtor (piece by piece) in the stipulated 1 year period, to finally make an application of dissolution as provided under Section 54. This may result in failure in fulfilment of one of the key objectives of enacting IBC, that is, timely completion of the proceedings.

Allowing the liquidator to sell the corporate debtor as a going concern proves to be time and cost effective, as well as saves the effort of the liquidator to find multiple buyers for multiple assets of the corporate debtor; hence, resulting in faster realisation for the creditors which is the ultimate aim of this entire exercise.

While relying on Regulation 32(e) of the Liquidation Process Regulations, the Hon’ble Supreme Court in the matter of Arcelor Mittal India Private Limited Vs. Satish Kumar Gupta & Ors[5] observed that:

“The only reasonable construction of the Code is the balance to be maintained between timely completion of the corporate insolvency resolution process, and the corporate debtor otherwise being put into liquidation. We must not forget that the corporate debtor consists of several employees and workmen whose daily bread is dependent on the outcome of the corporate insolvency resolution process. If there is a resolution applicant who can continue to run the corporate debtor as a going concern, every effort must be made to try and see that this is made possible.” (emphasis supplied)

Another key objective of IBC is to provide a painless revival mechanism for entities. Hence, a technical gap in the wordings of the IBC and Liquidation Process Regulations, which is easily fixable, should not act as a hindrance for fulfilment of this objective. Such an ouster would be in contravention to the doctrine of proportionality.

The Bankruptcy Law Reforms Committee (BLRC), in its Report[6], had also recognised GCS as an effective method of realization of assets and stated that from the viewpoint of creditors, a good realisation can generally be obtained if the firm is sold as a going concern[7].

The approach of BLRC was well-found and well-reasoned. Removing such enabling clauses from regulations merely due to lack of clear language in law would thus be disproportional and against the objective for which the provisions were first inserted.

Unlike winding-up, where the aim is to dissolve the entity, liquidation implies liquidating the entity and the main objective is to sell-off the asset(s) at a maximum value for realization and not necessarily kill the entity. In line with this objective, various Adjudicating Authorities have, in the past, allowed GCS in liquidation process.

In Gaurav Jain v. Sanjay Gupta, Liquidator of Topworth Pipes and Tubes Pvt. Ltd.[8], the Adjudicating Authority noted that even though there is no specific provision in IBC for “sale of the Company as a going concern”, the Liquidation Process Regulations provide guiding principles in dealing with the case. It held that “going concern” sale, in normal parlance, is transfer of assets along with the liabilities. However, as far as the ‘going concern’ sale in liquidation is concerned, there is a clear difference that only assets are transferred and the liabilities of the corporate debtor has to be settled in accordance with Section 53 of IBC and hence the purchaser of the assets takes over the assets without any encumbrance or charge and free from the action of the creditors. The legal entity of the corporate debtor survives and the assets with claims, limitations, licenses, permits or business authorisations remain with the corporate debtor. Only the ownership of the corporate debtor is acquired by the successful bidder and all creditors of the corporate debtor get discharged.

In Y. Shivram Prasad v S. Dhanapal & Ors.[9], the Appellate Authority ordered:

“…during the liquidation process, step required to be taken for its revival and continuance of the ‘Corporate Debtor’ by protecting the ‘Corporate Debtor’ from its management and from a death by liquidation. Thus, the steps which are required to be taken are as follows:

The Discussion Paper on Corporate Liquidation Process dated April 27, 2019[10] also recognized that the corporate debtor may continue to exist with or without business on completion of the process in case of a GCS. Even if an order under Section 33 of IBC has been passed for liquidation of a corporate debtor, on completion of GCS under IBC, the corporate debtor may not be liquidated or dissolved.

According to the Quarterly Newsletter of the Insolvency and Bankruptcy Board of India Vol.18[11], till March 31, 2021, out of a total of 138 cases of closure of liquidation proceedings, 128 liquidations (i.e. 92.75%) closed by dissolution, 6 (i.e. 4.35%) by going concern sale and 4 (i.e. 2.90%) by compromise /arrangement. The cases of closure by going concern sale had claims amounting to Rs. 4325.16 crore, as against the liquidation value of Rs. 290.03 crore. The liquidators in these cases realised Rs. 336.76 crore and companies were rescued. Therefore, it can be rightly said that going forward, going concern sale can be an important tool of value preservation.

Notably, GCS is only an option of ‘sale’. No harm accrues to the stakeholders if the entire entity can be sold as going concern. While it might be relevant to reconsider the regulations which mandate the liquidator to first attempt a GCS. It must be totally left to the wisdom of the liquidator to attempt or not to attempt a GCS, depending upon the market, investor interest, status of the assets, etc. Recognizing this, the Insolvency Law Committee (ILC) in its Report (2020)[12] noted that the liquidator is best placed to decide whether a going concern sale should be attempted, after assessing relevant factors such as the commercial viability of the business of the corporate debtor, and consulting the relevant stakeholders of the corporate debtor to ensure that it would generate a greater value than the other modes of liquidation. The Committee also agreed that GCS should not be mandated during liquidation and that the liquidator, in consultation with the relevant stakeholders of the corporate debtor, should be permitted to decide if a going concern sale should be attempted.

Addressing the incompatibility between Schemes of Arrangement under Section 230 of the Companies Act, 2013 and the liquidation as envisaged under IBC, the ILC stated that repeatedly attempting revival, through schemes of arrangement or otherwise, even where the business is not economically viable is likely to result in value destructive delays, and was identified as a key reason for the failure of the regime under the SICA, by the BLRC in its Interim Report. Indeed, where the business of the corporate debtor is still viable, the liquidator would have recourse to a going concern sale of the business to ensure that the liquidation process remains value maximizing. We, in our earlier article too, had questioned the need of a scheme under Section 230 of the Companies Act, 2013 in IBC which can be accessed here.

Having discussed the above, a possible counter-view that may be taken is that if sale as a going concern is allowed, the resolution applicant may prefer to wait for initiation of liquidation proceedings to buy the corporate debtor at a discounted value since liquidation value will always be lower than the value he would have had to shell out in insolvency resolution stage.

However, this may not be a well-backed stance because of the following reasons:

The Hon’ble NCLAT, Principal Bench, vide its order dated August 24, 2021[13], has upheld the validity of a GCS during liquidation by dismissing the order given by the Hon’ble NCLT, Principal bench in Invest Asset Securitisations & Reconstruction Pvt. Ltd (supra), based on which the Standing Committee had recommended the removal of clause pertaining to the sale of corporate debtor as a going concern. The NCLAT, in its order, stated the following:

By allowing the sale of corporate debtor as a going concern in liquidator, the NCLAT has made it clear that it is not disproportional to the Code and dissolution need not be the only outcome of liquidation.

It is pertinent to note that the Code does not prevent the closure of liquidation process in the instance the corporate debtor is sold as a going concern pursuant to Regulation 32(e) following the final closure report filed under Regulation 45(3)(a) of the Liquidation Process Regulations. It would, therefore, be contradictory to observe that closure of Liquidation Proceedings cannot be done and only dissolution is provided for under the Code. This would demolish the very spirit and objective of the Code.

Thus, it is once again emphasized that ouster of a widely acknowledged mode of sale, merely on account of a disparity in law would not be in favour of the Code and its stakeholders. In this pretext, it will be interesting to see the fate of this recommendation of the Standing Committee. Further, removal of the provision for going-concern for want of alignment would create a vacuum which could be potentially prejudicial for the Code and its stakeholders.

[1] https://www.ibbi.gov.in/uploads/whatsnew/fc8fd95f0816acc5b6ab9e64c0a892ac.pdf

[2] See detailed analysis on sale of legal entity of a corporate debtor at –https://vinodkothari.com/2020/11/sale-of-legal-entity-as-an-asset/

[3] https://nclt.gov.in/sites/default/files/Interim-order-pdf/Invest%20Assets%20Securitisation%20%26%20Reconstruction%20Pvt%20Ltd%20Vs.%20Mohan%20Germs%20%26%20Jewels%20Pvt%20Ltd._1.pdf

[4] http://164.100.158.181/Publication/Kolkata_Bench/2018/Others/13.pdf

[5]https://www.ibbi.gov.in/webadmin/pdf/whatsnew/2018/Oct/33945_2018_Judgement_04-Oct-2018_2018-10-04%2018:02:45.pdf

[6] https://ibbi.gov.in/BLRCReportVol1_04112015.pdf

[7] Page 15

[8] http://primusresolutions.in/pdf/Order-by-NCLT-for-successful-sale-as-Going-Concern.pdf

[9] https://nclat.nic.in/Useradmin/upload/212469115c8a433965360.pdf

[10] https://ibbi.gov.in/Discussion%20paper%20LIQUIDATION.pdf

[11] https://ibbi.gov.in/uploads/publication/2021-05-29-204331-atxcy-3363461de858b06bfa1afdbf13151b90.pdf

[12] https://www.mca.gov.in/Ministry/pdf/ICLReport_05032020.pdf

[13] https://ibbi.gov.in//uploads/order/ed29b92ace06f136a9060e3964e27ad8.pdf

Introduction

Under the provisions of Insolvency and Bankruptcy Code, 2016 (IBC), the determining criteria for insolvency is a definite default, rather than financial sickness or ‘inability to pay’ . While the latter is certainly suggestive of a larger state of insolvency, where the company may be unable to pay its outstanding debts, the former does not necessitate the same. Hence, the likelihood of an application for initiation of CIRP on the basis of an isolated event of default/ non-payment, sans a financial stress in the company, cannot be ruled out.

Owing to such uncertainty, it may so happen that an application, initiated on the basis of such an isolated event of default, is admitted before the adjudicating authority without any other cases of defaults by the company. Naturally, there would be no claims to file except that of the applicant. If it were to happen, it forces one to ponder as to how CIRP will proceed, and if at all there is something to resolve.

CIRP without claims?

As per the Code, CIRP commences after an application has been admitted by the AA. Once an application is admitted by the AA, an Interim Resolution Professional is appointed, who is responsible for invitation and collation of claims, and subsequent constitution of the committee of creditors (‘CoC’). All decisions with respect to the corporate debtor’s business are thereafter taken with the approval of CoC, including approval of Resolution Plan or passing of a resolution for liquidation of the Corporate Debtor. Hence, it can be said that the CoC, constituted on the basis of the claims, drives the CD through the process till revival/ liquidation, as the case may be.

However, in a rather odd situation, when no claims are received after the initiation of CIRP, how will the IRP constitute CoC? In essence, when no claims are received by the Interim Resolution Professional (‘IRP’) after the initiation of CIRP, the questions that would arise are (aside, the broader question as to whether there was at all a need for resolution, will remain) – how is the CIRP likely to proceed, how will IRP constitute CoC, and most importantly, what is it for which the IRP should invite resolution plans? Does non-receipt of any claims by the creditors prove that the Corporate Debtor is, in fact, not a defaulter?

Books of the corporate debtor/public announcement

At the first instance, the books of the corporate debtor will assist in determining whether at all the CD has liabilities (financial/operational, otherwise). It may be the case that the CD does not have any liability at all (besides that pertaining to the creditor who filed the application). In such a case, attempts can be made by the CD and the Creditor to arrive at an agreement among themselves, instead of proceeding with CIRP and having the CD jammed in a situation of Moratorium.

However, there may be cases where the books acknowledge liabilities but there are no claimants. This might pose practical difficulties for the IRP because if no claims are received, the constitution of CoC would become impossible which in turn would lead to the CIRP coming to a complete halt. Occurrence of such a situation might necessitate the following actions to be taken by the IRP-

Say, even after these efforts, no one shows up. There is a stage set, but there are no creditors to run the show. In such cases, what can the IRP do? We can explore the following alternatives.

Section 12A of Insolvency and Bankruptcy Code, 2016

Prior to section 12A of the Code, the withdrawal of an admitted insolvency resolution process was not expressly provided for. However, in view of reasons like a post-admission settlement or restructuring, the need to allow such withdrawal was realised – Section 12A of the Code enables withdrawal of the applications filed under Section 7, 9 or 10 of IBC, post its admission, if the committee of creditors (CoC) approves of such withdrawal by a voting share of at least ninety percent.

The very fact that section 12A mandates the approval of CoC as a precondition for withdrawal, there is no occasion to apply the said provisions before the constitution of CoC. A deeper reading of section 12A further indicates that the application for withdrawal must be filed by the very applicant who initiated the process. The reason is simple, the cause initiated by one cannot be withdrawn merely by virtue of a majority of others. Thus, the fact that withdrawal can be done only at the behest of the original applicant and with the consent of at least 90% CoC members maintains the much required trade off.

However, in the given state of affairs, the devil lies in the fact that no claims have been received so as to constitute the CoC. Further, to assume that the applicant who, at the first place, initiated the application, and thereafter chose to remain missing in action would initiate the withdrawal process, seems rather bizarre.

Even if one were to assume the possibility of withdrawal application by such a creditor, would the very filing be construed as a mere pressure tactic for recovery of claims? If yes, the same would attract penal provisions under the Code, and as such the Applicant would be liable for the consequences.

Knocking the Doors of NCLT

From the above discussion, we understand that a situation as such would indeed put the IRP/ RP in a pickle. Another probable way out could be an application being filed by the IRP/ RP under section 60 (5) of the Code thereby praying for annulling the process or directing the original applicant to file an application under section 12A.

Further, in Swiss Ribbons (P) Ltd. v. Union of India (Supra)[1], the Hon’ble Supreme Court made it clear that “at any stage where the committee of creditors is not yet constituted, a party can approach the NCLT directly, which Tribunal may, in exercise of its inherent powers under Rule 11 of the NCLT Rules, 2016, allow or disallow an application for withdrawal or settlement…….”

Thus, on the strength of the aforesaid order and the power and jurisdiction in section 60 (5), the IRP/ RP may take necessary steps before the Hon’ble Bench.

Such entanglement would leave the IPR/ RP in the middle of the sea, so to say that he can neither continue the CIRP in absence of the CoC, nor proceed for withdrawal as per section 12A.

Corporate Debtor – a Defaulter or no

Another line of thought that arises in the given facts could be whether the Corporate Debtor can be construed as a ‘defaulter’. In the given case, since no claims are received after the initiation of CIRP, can it be assumed that the Corporate Debtor has not defaulted in the payment of dues of any other creditor except for that of the applicant. Based on this assumption, can it be said that the CD is not a defaulter?

The above straight jacket assumption would not hold good as it is important to note that another probable situation that could arise is that the default of other creditors is apparent from the books of accounts of the Corporate Debtor. In such cases, if no claims are received by the IRP, the IRP may, in furtherance to the mandatory public announcement, send a mail to the banks/ financial creditors, inviting claims from them so that at least the CoC can be constituted and the CIRP can proceed.

While the above situation is a rather odd one, it would indeed be an interesting situation to understand the possible course of action that the IPs could resort to, and the role of the Adjudicating Authorities in such cases.

Ever since the Jaypee and Amrapali cases, home buyers have been under the scanner. From orders of the Hon’ble Supreme Court to multiple amendments in the Insolvency and Bankruptcy Code, measures have been taken to protect the interest of the home buyers. While earlier, the home buyers were treated as ‘other creditors’, that is, neither operational nor financial, with the landmark ruling in Chitra Sharma v. Union of India, there status as financial creditors was established – the same also found place in the Code by way of amendments in section 7 of the Code.

In this presentation, we discuss the provisions w.r.t. Home Buyers under the Code and a detailed case study of the Amrapali Case and Jaypee Infratech Case.

Home Buyers under IBC & Case Studies-Megha Mittal, Associate and Prachi Bhatia, Legal Intern

Insolvency laws, globally, have propagated the principle of equitable distribution as the very essence of liquidation/ bankruptcy processes; and while, “equitable distribution” is often colloquially read as “equal distribution” the two terms hold significantly different connotations, more so in liquidation processes – an ‘equitable distribution’ simply means applying similar principles of distribution for similarly placed creditors.

Closer home in India, the preamble of the Insolvency and Bankruptcy Code, 2016 (‘Code’/ ‘IBC’) also upholds the principles of equitable distribution – thus balancing interests of all stakeholders under the insolvency framework. Judicial developments have also had a significant role in holding such equity upright[1]. However, in the recent order of the Hon’ble National Company Law Appellate Tribunal, in Technology Development Board v. Mr. Anil Goel[2], the Hon’ble NCLAT has refused to acknowledge the validity of inter-se rights of secured creditors once such security interest in relinquished in terms of section 52 of the Code.

In what may potentially jeopardize interests of a larger body of secured creditors, the Appellate Authority held that inter-se arrangements between the secured creditors, for instance, first charge and second charge over the same asset(s), would not hold relevance if such secured creditors choose to be a part of the liquidation process under the Code – thus placing all secured creditors at an equal footing. The authors humbly present that the instant order may not be in consonance with the established and time-tested principles of ‘equitable’ treatment of creditors. The authors opine that contractual priorities form the very basis of a creditor’s comfort in distress situations – as such, a law which tampers with such contractual priorities (which of course, are not otherwise hit by avoidance provisions) in those very times, will go on to defeat the commercial basis of such contracts and demotivate the parties. This, as obvious, cannot be a desired outcome of a law which otherwise delves on the objective of ‘promotion of entrepreneurship and availability of credit’. The authors have tried putting their perspective in this article.

– Sikha Bansal, Partner and Megha Mittal, Associate (resolution@vinodkothari.com)

Preference shares, as the nomenclature suggests, represent that part of a Company’s capital which carries ‘preference´ vis-à-vis equity shares, with respect to payment of dividend and repayment of capital in case of winding up. However, the real position of preference shares may be quite baffling, given that the instrument, by its very nature, is sandwiched between equity capital and debt instruments. Although envisaged as a superior class of shares, preference shareholders enjoy neither the voting powers vested with the equity shareholders (true shareholders) nor the advantages vested with debenture-holders (true creditors). As such, the preference shareholders find themselves suspended midway between true creditors and true shareholders – hence facing the worst of both worlds[1].

The ambivalence associated with preference shares is adequately reflected in the manner various laws deal with such shares – a preference share is a part of ‘share-capital’ by legal classification[2], but can be a ‘debt’ as per accounting classification[3]; similarly, while a compulsorily convertible preference share is classified as an ‘equity instrument’[4], any other preference share constitutes external commercial borrowing[5] under foreign exchange laws. Needless to say, the divergent treatment is owed to the objective which each legislation assumes.

-Prachi Bhatia

Legal Intern at Vinod Kothari & Company

The three-judge bench of the Hon’ble Supreme Court vide its order dated 14th April, 2021, in Asset Reconstruction Limited v. Bishal Jaiswal & Anr[1] (‘ARCIL v. Bishal’) has settled the dust around acknowledgment of liability in books of corporate debtor for the purpose of section 18 of the Limitation Act; corollary to the applicability of the section to the Insolvency and Bankruptcy Code, 2016 (‘Code’). This comes in tandem with another recent order of the Hon’ble SC in LaxmiPat Surana v. Union Bank of India & Anr[2], wherein too the Apex Court upheld that acknowledgement of debt in the balance sheet would render initiation of the limitation period afresh for the purpose of filing an application under the Code.

In what seems to be the final word of law, the, vide the instant order, the Hon’ble SC further set aside the judgment set aside the Full Bench judgment of the Hon’ble NCLAT in V.Padmakumar v. Stressed Assets Stabilisation Fund[3], (‘V. Padmakumar’), wherein the Appellate Tribunal dismissed the benefit of extension of limitation to the creditors by virtue of the debt’s presentation in the books of the corporate debtor.

In this article, author humbly analyses the order of the Apex Court in ARCIL v. Bishal in light of the catena of preceding judgements both in favour and against the ratio-decidendi in ARCIL v. Bishal.

– Megha Mittal

The Insolvency and Bankruptcy (Amendment) Ordinance, 2021 (‘Ordinance’)[1] was promulgated on 5th April, 2021 to bring into force the prepackaged insolvency resolution framework for Micro, Small, Medium Enterprises (MSMEs). While the Ordinance put forth the structure of the prepack regime, a great deal was dependent upon the relevant rules and regulations. On 9th April, 2021, the Insolvency and Bankruptcy (Pre-packaged Insolvency Resolution Process) Regulations, 2021 (“Regulations”)[2] as well as the Insolvency and Bankruptcy (Pre-Packaged Insolvency Resolution Process) Rules, 2021 (“Rules”)[3] have been notified with immediate effect.

As one delves into the whole scheme of things, including the complicated provisions of the Ordinance and the even complication regulations, one gets to feel that the prepack framework will act only as a consolation for the MSMEs – while efforts aimed to increase the efficacy of insolvency resolution, the proposed Framework seems to do a little towards this end. In the author’s humble opinion, key elements of prepacks – cost and time efficiency and a Debtor-in-Possession approach, have been diluted amidst the micromanaged Rules and Regulations. In this article, we discuss how[4].

-Siddarth Goel (finserv@vinodkothari.com)

The penetration of electronic retail payments has witnessed a steep surge in the overall payment volumes during the latter half of the last decade. One of the reasons accorded to this sharp rise in electronic payments is the exponential growth in online merchant acquisition space. An online merchant is involved in marketing and selling its goods and/or services through a web-based platform. The front-end transaction might seem like a simple buying-selling transaction of goods or services between a buyer (customer) and a seller (merchant). However, the essence of this buying-selling transaction lies in the payment mode or methodology of making/accepting payments adopted between the customer and the merchant. One of the most common ways of payment acceptance is that the merchant establishes its own payment integration mechanism with a bank such that customers are enabled to make payments through different payment instruments. In such cases, the banks are providing payment aggregator services, but the market is limited usually to the large merchants only. Alternatively, merchants can rely upon third-party service providers (intermediary) that facilitate payment collection from customers on behalf of the merchant and thereafter remittance services to the merchant at the subsequent stage – this is regarded as a payment aggregation business.

The first guidelines issued by the RBI governing the merchant and payment intermediary relationship was in the year 2009[1]. Over the years, the retail payment ecosystem has transformed and these intermediaries, participating in collection and remittance of payments have acquired the market-used terminology ‘Payment Aggregators’. In order to regulate the operations of such payment intermediaries, the RBI had issued detailed Guidelines on Regulation of Payment Aggregators and Payment Gateways, on March 17, 2020. (‘PA Guidelines’)

The payment aggregator business has become a forthcoming model in the online retail payments ecosystem. During an online retail payment by a customer, at the time of checkout vis-à-vis a payment aggregator, there are multiple parties involved. The contractual parties in one single payment transaction are buyer, payment aggregator, payment gateway, merchant’s bank, customer’s bank, and such other parties, depending on the payment mechanism in place. The rights and obligations amongst these parties are determined ex-ante, owing to the sensitivity of the payment transaction. Further, the participants forming part of the payment system chain are regulated owing to their systemic interconnectedness along with an element of consumer protection.

This write-up aims to discuss the intricacies of the regulatory framework under PA Guidelines adopted by the RBI to govern payment aggregators and payment gateways operating in India. The first part herein attempts to depict growth in electronic payments in India along with the turnover data by volumes of the basis of payment instruments used. The second part establishes a contrast between payment aggregator and payment gateway and gives a broad overview of a payment transaction flow vis-à-vis payment aggregator. The third part highlights the provisions of the PA Guidelines and establishes the underlying internationally accepted best principles forming the basis of the regulation. The principles are imperative to understand the scope of regulation under PA Guidelines and the contractual relationship between parties forming part of the payment chain.

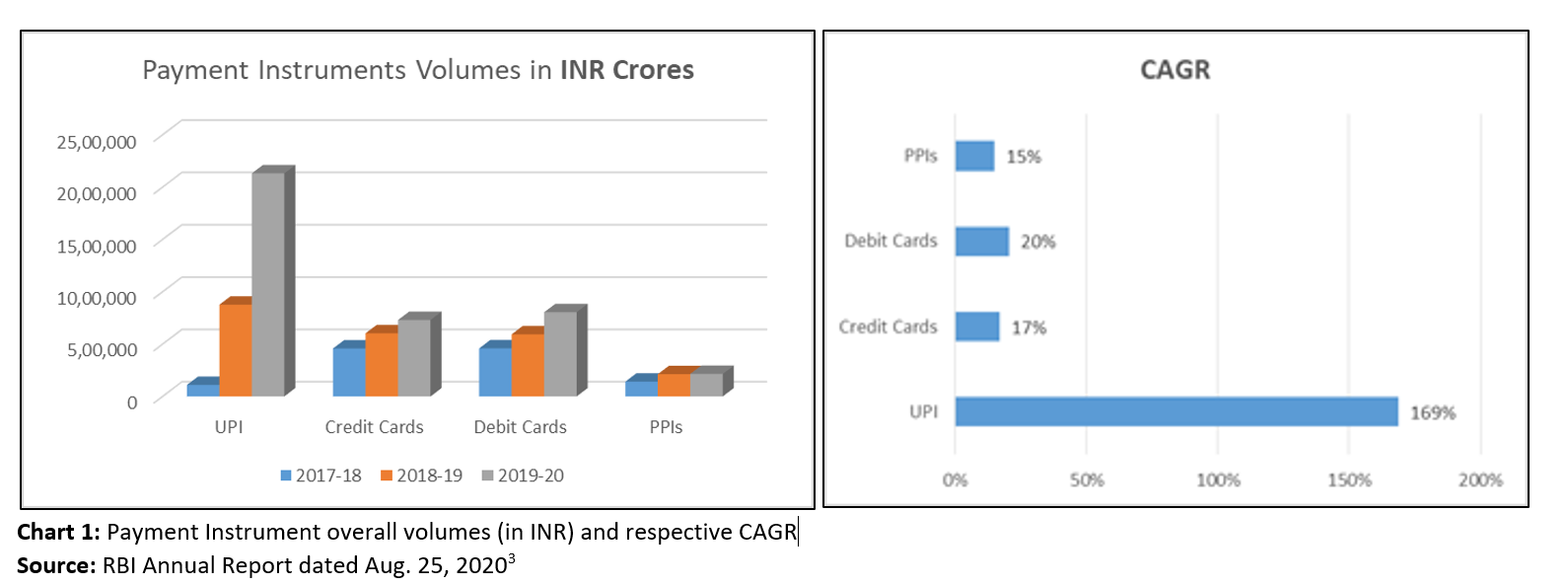

The RBI in its report stated that the leverage of technology through the use of mobile/internet electronic retail payment space constituted around 61% share in terms of volume and around 75% in share in terms of value during FY 19-20.[2] The innovative payment instruments in the retail payment space, have led to this surge in electronic payments. Out of all the payment instruments, the UPI is the most innovative payment instrument and is the spine for growth in electronic payments systems in India. Chart 1 below compares some of the prominent payment instruments in terms of their volumes and overall compounded annual growth rate (CAGR) over the period of three years.

The payment system data alone does not show the complete picture. In conformity with the rise in electronic payment volumes, as per the Government estimates the overall online retail market is set to cross the $ 200 bn figure by 2026 from $ 30 bn in 2019, at an expected CAGR of 30 %.[4] India ranks No. 2 in the Global Retail Development Index (GRDI) in 2019. It would not be wrong to say, the penetration of electronic payments could be due to the presence of more innovative products, or the growth of online retail has led to this surge in electronic payments.

The terms Payment Aggregator (‘PA’) and Payment Gateways (‘PG’) are at times used interchangeably, but there are differences on the basis of the function being performed. Payment Aggregator performs merchant on-boarding process and receives/collects funds from the customers on behalf of the merchant in an escrow account. While the payment gateways are the entities that provide technology infrastructure to route and/or facilitate the processing of online payment transactions. There is no actual handling of funds by the payment gateway, unlike payment aggregators. The payment aggregator is a front-end service, while the payment gateway is the back-end technology support. These front-end and back-end services are not mutually exclusive, as some payment aggregators offer both. But in cases where the payment aggregator engages a third-party service provider, the payment gateways are the ‘outsourcing partners’ of payment aggregators. Thereby such payments are subject to RBI’s outsourcing guidelines.

One of the most sought-after electronic payments in the online buying-selling marketplace is the payment systems supported by PAs. The PAs are payment intermediaries that facilitate e-commerce sites and merchants in accepting various payment instruments from their customers. A payment instrument is nothing but a means through which a payment order or an instruction is sent by a payer, instructing to pay the payee (payee’s bank). The familiar payment instruments through which a payment aggregator accepts payment orders could be credit cards, debit cards/PPIs, UPI, wallets, etc.

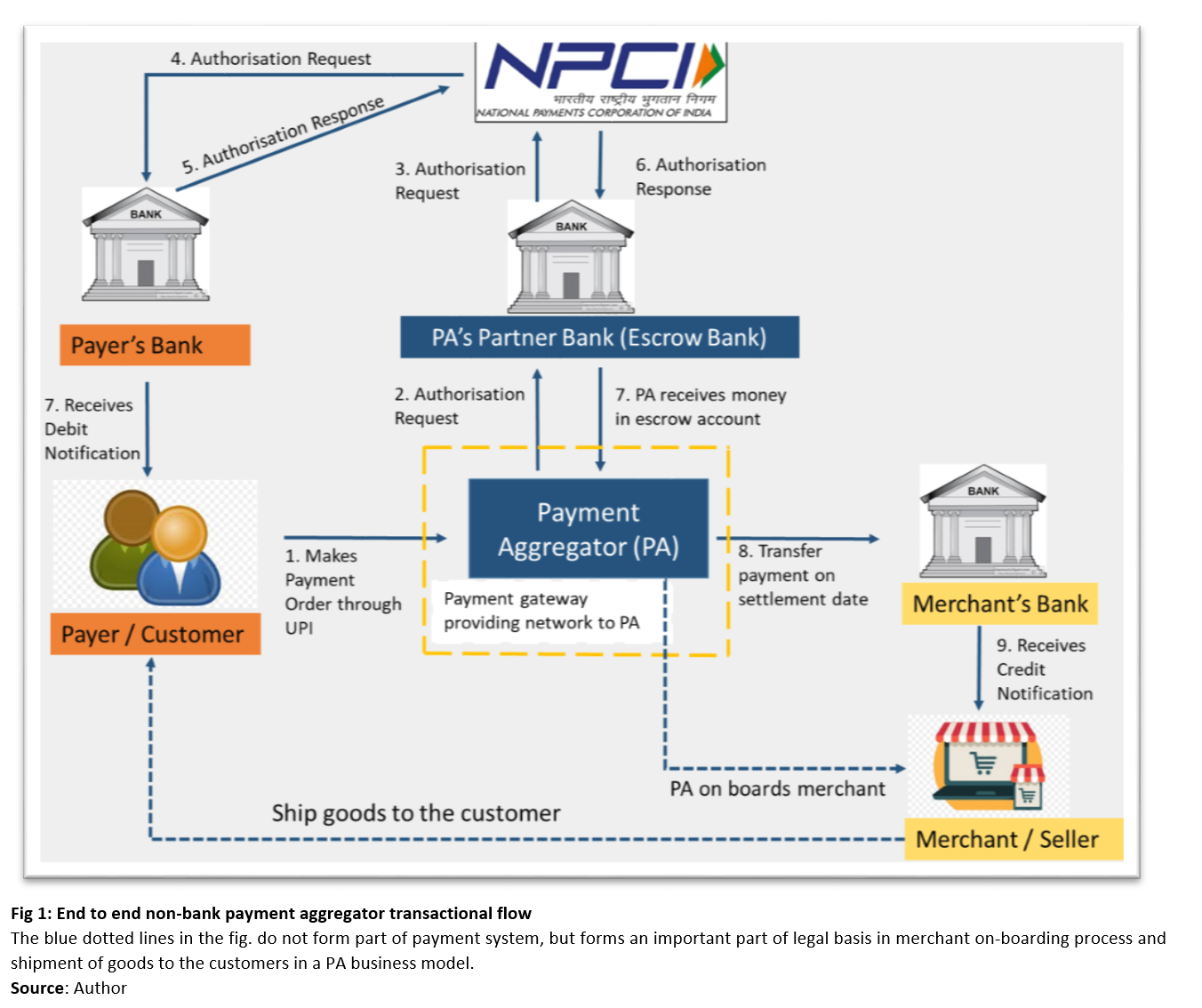

Payment aggregators are intermediaries that act as a bridge between the payer (customer) and the payee (merchant). The PAs enable a customer to pay directly to the merchant’s bank through various payment instruments. The process flow of each payment transaction between a customer and the merchant is dependent on the instrument used for making such payment order. Figure 1 below depicts the payment transaction flow of an end-to-end non-bank PA model, by way of Unified Payment Interface (UPI) as a payment instrument.

In an end-to-end model, the PA uses the clearing and settlement network of its partner bank. The clearing and settlement of the transaction are dependent on the payment instrument being used. The UPI is the product of the National Payments Corporation of India (NPCI), therefore the payment system established by NPCI is also quintessential in the transaction. The NPCI provides a clearing and settlement facility to the partner bank and payer’s bank through the deferred settlement process. Clearing of a payment order is transaction authorisation i.e., fund verification in the customer’s bank account with the payer’s bank. The customer/payer bank debits the customer’s account instantaneously, and PA’s bank transfers the funds to the PA’s account after receiving authorisation from NPCI. The PA intimates the merchant on receipt of payment and the merchant ships the goods to the customer. The inter-bank settlement (payer’s bank and PA’s partner bank) happens at a later stage via deferred net-settlement basis facility provided by the NPCI.

The first leg of the payment transaction is settled between the customer and PA once the PA receives the confirmation as to the availability of funds in the customer’s bank account. The partner bank of PA transfers the funds by debiting the account of PA maintained with it. The PA holds the exposure from its partner bank, and the merchant holds the exposure from the PA. This explains the logic of PA Guidelines, stressing on PAs to put in place an escrow mechanism and maintenance of ‘Core Portion’ with escrow bank. It is to safeguard the interest of the merchants onboarded by the PA. Nevertheless, in the second leg of the transaction, the merchant has its right to receive funds against the PA as per the pre-defined settlement cycle.

The international standards and best practices on regulating Financial Market Infrastructure (FMI) are set out in CPSS-IOSCO principles of FMI (PFMI).[5] A Financial Market Infrastructure (FMI) is a multilateral system among participating institutions, including the operator of the system. The consumer protection aspects emerging from the payment aggregation business model, are regulated by these principles. Based on CPSS-IOSCO principles of (PFMI), the RBI has described designated FMIs, and released a policy document on regulation and supervision of FMIs in India under its regulation on FMIs in 2013.[6] The PFMI stipulates public policy objectives, scope, and key risks in financial market infrastructures such as systemic risk, legal risk, credit risk, general business risks, and operational risk. The Important Retail Payment Systems (IRPS) are identified on the basis of the respective share of the participants in the payment landscape. The RBI has further sub-categorised retail payments FMIs into Other Retail Payment Systems (ORPS). The IRPS are subjected to 12 PFMI while the ORPS have to comply with 7 PFMIs. The PAs and PGs fall into the category of ORPS, regulatory principles governing them are classified as follows:

These principles of regulation are neither exclusive nor can said to be having a clear distinction amongst them, rather they are integrated and interconnected with one another. The next part discusses the broad intention of the principles above and the supporting regulatory clauses in PA Guidelines covering the same.

The legal basis principle lays the foundation for relevant parties, to define the rights and obligations of the financial market institutions, their participants, and other relevant parties such as customers, custodians, settlement banks, and service providers. Clause 3 of PA Guidelines provides that authorisation criteria are based primarily on the role of the intermediary in the handling of funds. PA shall be a company incorporated in India under the Companies Act, 1956 / 2013, and the Memorandum of Association (MoA) of the applicant entity must cover the proposed activity of operating as a PA forms the legal basis. Henceforth, it is quintessential that agreements between PA, merchants, acquiring banks (PA’s Partners Bank), and all other stakeholders to the payment chain, clearly delineate the roles and responsibilities of the parties involved. The agreement should define the rights and obligations of the parties involved, (especially the nodal/escrow agreement between partner bank and payment aggregator). Additionally, the agreements between the merchant and payment aggregator as discussed later herein are fundamental to payment aggregator business. The PA’s business rests on clear articulation of the legal basis of the activities being performed by the payment aggregator with respect to other participants in the payment system, such as a merchant, escrow banks, in a clear and understandable way.

The framework for the comprehensive management of risks provides for integrated and comprehensive view of risks. Therefore, this principle broadly entails comprehensive risk policies, procedures/controls, and participants to have robust information and control systems. Another connecting aspect of this principle is operational risk, arising from internal processes, information systems and disruption caused due to IT systems failure. Thus there is a need for payment aggregator to have robust systems, policies to identify, monitor and manage operational risks. Further to ensure efficiency and effectiveness, the principle entails to maintain appropriate standards of safety and security while meeting the requirements of participants involved in the payment chain. Efficiency is resources required by such payment system participants (PAs/PGs herein) to perform its functions. The efficiency includes designs to meet needs of participants with respect to choice of clearing and settlement transactions and establishing mechanisms to review efficiency and effectiveness. The operational risk are comprehensively covered under Annex 2 (Baseline Technology-related Recommendation) of the PA Guidelines. The Annex 2, inter alia includes, security standards, cyber security audit reports security controls during merchant on-boarding. These recommendations and compliances under the PA Guidelines stipulates standard norms and compliances for managing operational risk, that an entity is exposed to while performing functions linked to financial markets.

An important aspect of payment aggregator business covers merchant on-boarding policies and anti-money laundering (AML) and counter-terrorist financing (CFT) compliance. The BIS-CPSS principles do not govern within its ambits certain aspects like AML/CFT, customer data privacy. However, this has a direct impact on the businesses of the merchants, and customer protection. Additionally, other areas of regulation being data privacy, promotion of competition policy, and specific types of investor and consumer protections, can also play important roles while designing the payment aggregator business model. Nevertheless, the PA Guidelines provide for PAs to undertake KYC / AML / CFT compliance issued by RBI, as per the “Master Direction – Know Your Customer (KYC) Directions” and compliance with provisions of PML Act and Rules. The archetypal procedure of document verification while customer on-boarding process could include:

PAs shall ensure that the merchant’s site shall not save customer’s sensitive personal data, like card data and such related data. Agreement with merchant shall have provision for security/privacy of customer data.

The other critical facet of PA business is the settlement cycle of the PA with the merchants and the escrow mechanism of the PA with its partner bank. Para 8 of PA Guidelines provide for non-bank PAs to have an escrow mechanism with a scheduled bank and also to have settlement finality. Before understanding the settlement finality, it is important to understand the relevance of such escrow mechanisms in the payment aggregator business.

Surely there is a bankruptcy risk faced by the merchants owing to the default by the PA service provider. This default risk arises post completion of the first leg of the payment transaction. That is, after the receipt of funds by the PA from the customer into its bank account. There is an ultimate risk of default by PA till the time there is final settlement of amount with the merchant. Hence, there is a requirement to maintain the amount collected by PA in an escrow account with any scheduled commercial bank. All the amounts received from customers in partner bank’s account, are to be remitted to escrow account on the same day or within one day, from the date amount is debited from the customer’s account (Tp+0/Tp+1). Here Tp is the date on which funds are debited from the customer’s bank account. At end of the day, the amount in escrow of the PA shall not be less than the amount already collected from customer as per date of debit/charge to the customer’s account and/ or the amount due to the merchant. The same rules shall apply to the non-bank entities where wallets are used as a payment instrument.[7] This essentially means that PA entities should remit the funds from the PPIs and wallets service provider within same day or within one day in their respective escrow accounts. The escrow banks have obligation to ensure that payments are made only to eligible merchants / purposes and not to allow loans on such escrow amounts. This ensures ring fencing of funds collected by the PAs, and act as a deterrent for PAs from syphoning/diverting the funds collected on behalf of merchants. The escrow agreement function is essentially to provide bankruptcy remoteness to the funds collected by PA’s on behalf of merchants.

Settlement finality is the end-goal of every payment transaction. Settlement in general terms, is a discharge of an obligation with reference of the underlying obligation (whatever parties agrees to pay, in PA business it is usually INR). The first leg of the transaction involves collection of funds by the PA from the customer’s bank (originating bank) to the PA escrow account. Settlement of the payment transaction between the PA and merchant, is the second leg of the same payment transaction and commences once funds are received in escrow account set up by the PA (second leg of the transaction).

Settlement finality is the final settlement of payment instruction, i.e. from the customer via PA to the merchant. Final settlement is where a transfer is irrevocable and unconditional. It is a legally defined moment, hence there shall be clear rules and procedures defining the point of settlement between the merchant and PA.

For the second leg of the transaction, the PA Guidelines provide for different settlement cycles:

These settlement cycles are mutually exclusive and the PA business models and settlement structure cycle with the merchants could be developed by PAs on the basis of market dynamics in online selling space. Since the end-transaction between merchant and PA is settled on a contractually determined date, there is a deferred settlement, between PA and the merchant. Owing to the rules and nature of the relationship (deferred settlement) is the primary differentiator from the merchants proving the Delivery vs. Payment (DvP) settlement process for goods and services.

Banks operating as PAs do not need any authorisation, as they are already part of the the payment eco-system, and are also heavily regulated by RBI. However, owing to the sensitivity of payment business and consumer protection aspect non-bank PA’s have to seek RBI’s authorisation. This explains the logic of minimum net-worth requirement, and separation of payment aggregator business from e-commerce business, i.e. ring-fencing of assets, in cases where e-commerce players are also performing PA function. Non-bank entities are the ones that are involved in retail payment services and whose main business is not related to taking deposits from the public and using these deposits to make loans (See. Fn. 7 above).

However, one could always question the prudence of the short timelines given by the regulator to existing as well as new payment intermediaries in achieving the required capital limits for PA business. There might be a trade-off between innovations that fintech could bring to the table in PA space over the stringent absolute capital requirements. While for the completely new non-bank entity the higher capital requirement (irrespective of the size of business operations of PA entity) might itself pose a challenge. Whereas, for the other non-bank entities with existing business activities such as NBFCs, e-commerce platforms, and others, achieving ring-fencing of assets in itself would be cumbersome and could be in confrontation with the regulatory intention. It is unclear whether financial institutions carrying financial activities as defined under section 45 of the RBI Act, would be permitted by the regulator to carry out payment aggregator activities. However, in doing so, certain additional measures could be applicable to such financial entities.

The payment aggregator business models in India are typically based on front-end services, i.e. the non-bank entitles are aggressively entering into retail payment businesses by way of providing direct services to merchants. The ability of non-bank entitles to penetrate into merchant onboarding processes, has far overreaching growth potential than merchant on-boarding processes of traditional banks. While the market is at the developmental stage, nevertheless there has to be a clear definitive ex-ante system in place that shall provide certainty to the payment transactions. The CPSS-IOSCO, governing principles for FMIs lays down a good principle-based governing framework for lawyers/regulators and system participants to understand the regulatory landscape and objective behind the regulation of payment systems. PA Guidelines establishes a clear, definitive framework of rights between the participants in the payment system, and relies strongly on board policies and contractual arrangements amongst payment aggregators and other participants. Therefore, adequate care is necessitated while drafting escrow agreements, merchant-on boarding policies, and customer grievance redressal policies to abide by the global best practices and meet the objective of underlying regulation. In hindsight, it will be discovered only in time to come whether the one-size-fits-all approach in terms of capital requirement would prove to be beneficial for the overall growth of PA business or will cause a detrimental effect to the business space itself.

[1] RBI, Directions for opening and operation of Accounts and settlement of payments for electronic payment transactions involving intermediaries, November 24, 2009. https://www.rbi.org.in/scripts/NotificationUser.aspx?Mode=0&Id=5379

[2] Payment Systems in India – Booklet (rbi.org.in)

[3] https://m.rbi.org.in/Scripts/AnnualReportPublications.aspx?Id=1293

[4] https://www.investindia.gov.in/sector/retail-e-commerce

[5] The Bank for International Settlements (BIS), Committee on Payment and Settlement Systems (CPSS) and International Organisation of Securities Commissions (IOSCO) published 24 principles for financial market infrastructures and and responsibilities of central banks, market regulators and other authorities. April 2012 <https://www.bis.org/cpmi/publ/d101a.pdf>

[6]Regulation and Supervision of Financial Market Infrastructures, June 26, 2013 https://www.rbi.org.in/scripts/bs_viewcontent.aspx?Id=2705

[7] CPMI defines non-banks as “any entity involved in the provision of retail payment services whose main business is not related to taking deposits from the public and using these deposits to make loans” See, CPMI, ‘Non-banks in retail Payments’, September 2014, available at <https://www.bis.org/cpmi/publ/d118.pdf>

RBI to regulate operation of payment intermediaries – Vinod Kothari Consultants