IMPACT OF FAIR VALUE CHANGES ON RETAINED EARNINGS DURING FIRST TIME IND AS ADOPTION

By Beni Agarwal (beni@vinodkothari.com)

By Beni Agarwal (beni@vinodkothari.com)

Refer to valuation approaches here- http://vinodkothari.com/2020/09/valuation-approaches-and-methods/

By Nikita Snehil | nikita@vinodkothari.com

The term ‘Fair market value’ has been used hundreds of times in the Income Tax Act, 1961, however, the same has also been given due weightage under the Companies Act, 2013. The present Article intends to explain the meaning of the term ‘Fair Market Value’, its significance and its relevance as per Companies Act, 2013.

In general parlance, Fair market value is the price agreed between a buyer and a seller for a specific asset. Both parties should be aware of the asset’s condition and willing to participate in the transaction with no force or conditions.

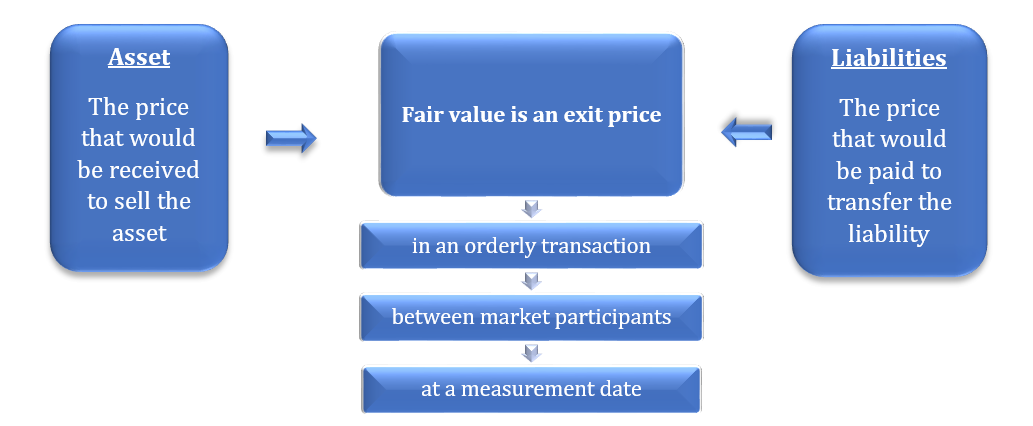

However, the term has been defined in para 9 the Ind AS 113[1], which states the following:

“Ind AS defines fair value as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date.”

Therefore, the definition can be illustrated in the following way:

The concept of Fair Market Value has become all pervasive particularly after the introduction of International Financial Reporting Standards because there is greater stress on fair value today than in the past.

The provisions of the Companies Act, 2013 (‘Act’) talks about the requirement of valuation in many cases, the following table shows the sections of the Act requiring valuations:

| Section no. | Valuation purpose |

Requirements in brief

|

| 54 | Issuance of Sweat Equity Shares | The sweat equity shares to be issued shall be valued at a price determined by a registered valuer as the fair price giving justification for such valuation.

|

| 62(1) (c) | Preferential Offer | When a company proposes to issue new shares, the price of such shares should be determined by the valuation report of a Registered Valuer.

|

| 192(2) | Non-cash transaction involving directors | Where there is a sale or purchase of any asset involving a company and its directors (or its

holding, subsidiary or associate company) or a person connected with the director for consideration other than cash, the value of the assets has to be calculated by a Registered Valuer.

|

| 230 & 232 | Compromises, Arrangements and Amalgamations | In case of compromise or arrangement between members or with creditors or any class of them, a valuation report in respect of shares, property or assets, tangible and intangible, movable and immovable of the company is required by a Registered Valuer.

|

| 236 | Purchase of minority share holding | Where an acquirer or person acting in concert with the acquirer acquires 90% or more of the equity capital in a company, then they can offer to the minority shareholder or the minority shareholder can offer to the acquirer, to acquire the minority shareholding at a valuation determined by the Registered Valuer.

|

| 281 & 305 | Winding up of a company | In case of winding up, the valuation of assets of the company prepared by the Registered Valuer is required.

|

Though the Act does not specify anything regarding the eligibility of the registered valuers, the Companies (Share Capital and Debenture) Rules, 2014 provides the following:

For the purposes of these rules, it is hereby clarified that, till a registered valuer is appointed in accordance with the provisions of the Act, the valuation report shall be made by an independent merchant banker who is registered with the Securities and Exchange Board of India or an independent Chartered Accountant in practice having a minimum experience of ten years.

Thereafter, MCA had notified the provisions governing valuation by registered valuers [section 247 of the Act and the Companies (Registered Valuers and Valuation) Rules, 2017 (‘Rules’), both to come into effect from 18 October, 2017.

Valuation by Registered Valuers

As per the notified section 247(1), where a valuation is required to be made in respect of any property, stocks, shares, debentures, securities or goodwill or any other assets or net worth of a company or its liabilities under the provision of this Act, it shall be valued by a person having such qualifications and experience and registered as a valuer in such manner, on such terms and conditions as may be prescribed and appointed by the audit committee or in its absence by the Board of Directors of that company.

Proposal of MCA to have registered valuers

The definition of ‘Valuer’ in the said Rules, provides the following:

“valuer” means a person registered with the authority in accordance with these rules and the term “registered valuer” shall be construed accordingly.

Therefore, the valuer will have to obtain the Certificate of Registration after complying the qualification and eligibility criteria as specified in the Rules, in order to do the valuation.

Eligibility of Registered Valuers

As per Rule 3 of the said Rules, the following person shall be eligible to be a registered valuer if he-

Explanation.- For the purposes of this clause, “a valuer member” is a member of a registered valuers organisation who possesses the requisite educational qualifications and experience for being registered as a valuer;

Explanation.- For the purposes of these rules ‘person resident in India’ shall have the same meaning as defined in clause (v) of section 2 of the Foreign Exchange Management Act, 1999 (42 of 1999) as far as it is applicable to an individual;

Provided that if a person has been convicted of any offence and sentenced in respect thereof to imprisonment for a period of seven years or more, he shall not be eligible to be registered;

Further, with respect to a partnership entity or company, the following shall not be eligible to be a registered valuer if-

Applicability of the Rules

As per the transitional provisions specified in the Rules read with the MCA’s Notification[1] on extending the transitional period:

“Any person who may be rendering valuation services under the Act, on the date of commencement of these rules, may continue to render valuation services without a certificate of registration under these rules upto 30th September, 2018:

Provided that if a company has appointed any valuer before such date and the valuation or any part of it has not been completed before 30th September, 2018, the valuer shall complete such valuation or such part within three months thereafter.”

Therefore, the persons intending to act as the registered valuers must obtain the Certificate of Registration within September 30, 2018, as per the requirements of the Rules.

Recognising the need to have the consistent, uniform and transparent valuation policies and harmonise the diverse practices in use in India, the Council of the Institute of Chartered Accountants of India at its 375th meeting has issued the Valuation Standards vide the Press Release[2] dated May 25, 2018, mandating the compliance with the Standards for the Chartered Accountants providing valuation reports under various provisions of the Companies Act.

The Standards include the framework for the preparation of valuation report, valuation bases, approaches and methods, scope of work, analyses and evaluations, documentation and reporting, intangible assets and financial instruments, among several other aspects.

Therefore, recognizing the importance of valuation, the Rules introduced by MCA and the standards introduced by ICAI will provide a benchmark to the professionals to ensure uniformity in approach and quality of valuation output.

[1] http://mca.gov.in/Ministry/pdf/INDAS113.pdf

[2] http://www.mca.gov.in/Ministry/pdf/CompaniesRules2018_12022018.pdf

[3] https://www.icai.org/new_post.html?post_id=14799&c_id=238

Anita Baid

finserv@vinodkothari.com

The Reserve Bank of India (RBI) released its first monetary policy statement for FY 2018-19 on April 05, 2018[1] (‘Policy Statement’). The aforesaid statement sets out various developmental and regulatory policy measures for the financial sector. It aims at strengthening regulation and supervision; broadening and deepening financial markets; improving currency management; promoting financial inclusion and literacy; and, facilitating data management. Some of the major issues from the Policy Statement have been discussed herein below: Read more →

CS Vinita Nair | vinita@vinodkothari.com

Loading…

Loading…