Corporate succession events: Treatment of unspent or overspent CSR obligations

CS Aisha Begum Ansari, Manager & Payal Agarwal, Deputy Manager | corplaw@vinodkothari.com

Background

The identity of a corporate entity may undergo various restructurings, either in the form of merger, demerger, sale of one or more divisions or undertakings. conversion of a company into LLP etc. Let us, for the sake of convenience, call them a “corporate succession” event, implying a situation where a corporate entity is succeeded by another entity, or its business, operations or undertaking shifts to another entity. In some cases, say, amalgamation, the erstwhile corporate entity gets dissolved. In case of a demerger, the transferor entity continues. In case of conversion into LLP or vice versa, a company gets transformed into an LLP or other way round.

Usually, in corporate succession events, the assets and liabilities forming part of an undertaking are shifted to another undertaking, say, the successor entity. The assets and liabilities that are comprised in an undertaking are mostly defined to include all liabilities existing on pertaining to a certain date, let us call it “appointed date”.

One of the perplexing aspects of this process of transfer of assets and liabilities may be the treatment of the unspent CSR obligations, or excess spending, by the corporate entity which is undergoing a change in its identity. The question becomes increasingly significant in the present day regulatory environment due to the shift in CSR from COPEX (Comply or Explain) to COPP (Comply or Pay Penalty).

In the present write-up, we discuss the treatment of CSR obligations as a result of the following actions resulting into a change in the identity of a corporate –

- Merger

- Demerger

- Sale of a division/ undertaking (“Slump sale”)

- Conversion of a company into LLP

A. Treatment of CSR in case of merger

In case of merger of two or more companies into one, the transferor company loses its identity altogether and only the transferee company survives. There is a time gap between the approval of merger in the board of the transferor and transferee companies and the final approval of NCLT to the scheme of merger. During this time gap, while the transferor company is understood to be operating the business activities as a trust for the transferee company, however, till the approval of the scheme by NCLT, the entities continue to operate separately and prepare their separate set of financials.

Here, before we discuss the concerns on CSR and treatment thereof, let us first understand the concept of “Appointed Date” and “Effective Date”.

Appointed Date and Effective Date

The Appointed Date (‘AD’) and Effective Date (‘ED’), though not defined, are most commonly used terms in relation to corporate restructurings. One may refer to various judicial precedents explaining the meaning of each of the aforesaid.

In L&T Hydrocarbon Engineering Ltd v/s Union of India[1], the Gujarat High Court interprets the AD and ED as below in the context of demerger –

“The appointed date is the date with effect from which the Scheme shall upon sanction of the same by the High Court, be deemed to be operative.

XXX

The effective date denotes the date on which the demerger is completed in all respects after having gone through the formalities involved, and a copy of the High Court’s order sanctioning the scheme is filed with the Registrar of Companies.”

MCA also had clarified vide a circular that the “acquisition date” for the purpose of Ind AS – 103 is akin to the appointed date under a scheme of arrangement. Under Ind AS, it has been defined as “a date on which the acquirer obtains control of the acquiree”.

Therefore, while the effective date is the date when a scheme receives the final sanction of NCLT, and therefore, actually becomes operative; the appointed date is the date from which the same is deemed to be operative. In other words, while a scheme is effective from the appointed date, the same has no effect until the effective date. For a more detailed understanding of the “appointed date” and “effective date”, one may refer to Effectiveness of Appointed Date in a Scheme of Arrangement.

Any income earned or expenses incurred by the transferor company during the period from AD to ED, is deemed to be the income and expense of the transferee company, and the transferor company is deemed to be acting as a trust for the transferee company from the AD till the ED.

Multiple questions may arise for consideration here, for example –

- Whether the applicability of CSR from AD till ED is to be determined on the basis of the merged financials of the transferor and transferee companies? If so, how is the CSR spending obligation of such a financial year determined?

- Whether the unspent CSR obligations of the transferor company gets transferred to the transferee company on merger?

- Whether the excess amount spent by the transferor company is available for set-off to the transferee company?

We discuss each of these below with appropriate examples.

a. Determining applicability of CSR and spending obligations thereof

The applicability of CSR u/s 135(1) of the Companies Act, 2013 (‘the Act’) is computed on the basis of the specified thresholds of the financial parameters (being net profits, net worth and turnover) as on the preceding financial year.

Further, the CSR spending obligations under section 135(5) is computed as an average of the adjusted net profits of the last three years’ financials.

Till the time the scheme of merger is approved by NCLT and made effective, the transferor and transferee entities continue to operate as separate legal entities and draw separate financials. They are not required to prepare merged financials for the period between AD and ED, till the time the merger is finally effective. Therefore, the applicability of CSR as well as spending obligations thereof should be calculated on the basis of standalone financials of the transferor and transferee companies, and not the merged financials.

Let us understand the same by way of the following example –

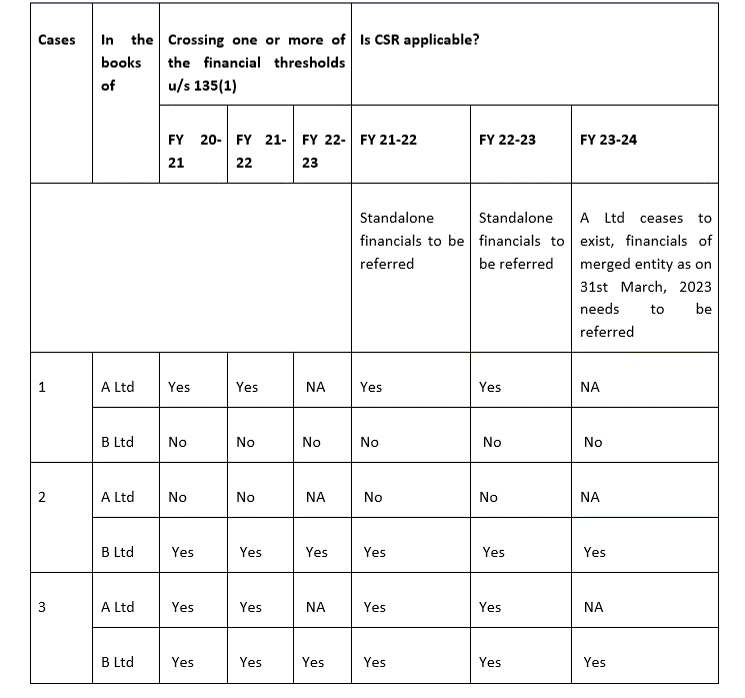

Example: A Ltd is a transferor company and B Ltd is the transferee company. The AD for the scheme of merger is 1st April, 2021 and the ED is 30th September, 2022.

In the aforesaid example, for FY 21-22 and FY 22-23, the companies continue to be guided by their individual financial thresholds for determination of applicability of CSR, and therefore, CSR obligations. However, the question arises in FY 23-24, in which A Ltd (transferor company) ceases to exist, and B Ltd (transferee company) operates as a merged entity. The thresholds for applicability are based on the financials of the preceding financial year, i.e., FY 22-23 in the instant case. While both A Ltd and B Ltd operate as standalone entities for the first half of the FY, i.e., till 30th September, 2022, B Ltd operates as a merged entity for the remaining part of the FY.

Since the financial thresholds as existing on the last day of the financial year is taken into account for the purpose of determining applicability, therefore, the merged financials for FY 22-23 should be taken into consideration for determining applicability of CSR provisions.

The CSR obligations for FY 23-24 has to be calculated as an average of the net profits of the Company for the three immediately preceding financial years, being FY 22-23, 21-22 and 20-21. Post the merger being effective, it will be deemed to have been in effect from 1st April, 2021, hence, the profits as per the merged financials of the transferee company will be taken into consideration for FY 21-22 and FY 22-23. For FY 20-21, the standalone financials of the transferee company continues to be referred to.

b. Treatment of unspent CSR obligations of the transferor company

As discussed earlier, from AD till ED, the transferor company continues to operate as a separate entity, and is required to comply with all applicable provisions of law including CSR spending obligations, if applicable. However, once the merger is approved, what implications does it have on the transferee company, if there are any unspent obligations of the transferor company.

Consider Case I of the aforesaid example, where only A Ltd (transferor company) is covered by the provisions of CSR. During FY 22-23, A Ltd has a CSR obligation of Rs. 1 crore. There may be following probable situations in such case –

| Situations | Amount spent on CSR activities | Resultant Impact |

| Situation 1 | 1 crore | No pending obligations for FY |

| Situation 2 | < 1 crore | The unspent obligation ceases to exist with the cessation of A Ltd (transferor company) as a result of merger |

| Situation 3 | >1 crore | Dealt with in later part of this article |

Thus, if any amount remains unspent by the transferor in the year in which merger gets approved, the same does not pass on to the transferee company. The transferee is responsible only for its own CSR obligations computed out of its own past net profits.

Here, one may contend that since the merger becomes effective from the AD itself, the unspent CSR obligations of the transferor company, results in accrual of such obligations on the transferee company automatically. However, this will lead to practical difficulties in implementation and therefore, does not seem to be a logical approach to the same.

While the CSR spending obligations during the year may cease to exist with the dissolution of the transferor company, the CSR obligations, if any remaining unspent at the end of the relevant financial year, will be recognised as a liability in the books of the transferor company. Here, please note that the liability arises only at the end of the financial year and hence the liability for the same is recognised at the end of the financial year. The same has also been clarified by ICAI vide Frequently Asked Question on Accounting for amounts to be incurred towards Corporate Social Responsibility (CSR) pursuant to the Companies (Corporate Social Responsibility Policy) Amendment Rules, 2021 dated 10th May, 2021.

For example, A Ltd (transferor company) has a CSR obligation of Rs. 80 lacs during FY 21-22, out of which Rs. 50 lacs remained unspent at the end of FY 21-22. The ED of the merger is at any time during FY 22-23, let’s say 20th May, 2022.

In this case, as on 31st March, 2022, a liability amounting to Rs. 50 lacs will be recognised in the books of A Ltd in the name of “Unspent CSR liability”. In case A Ltd does not transfer the said amount to a fund specified under Schedule VII prior to the merger becoming effective, the liability gets transferred to the transferee company, and the same will be required to transfer the same within 30th September, 2022. In the event of failure to do such transfer within the specified time, the transferee company may also be liable to penalty in terms of sub-section (7) of section 135 of the Act.

c. Treatment of CSR excess spent by the Transferor company

Rule 7(3) of the CSR Rules, allows a company to set off the excess CSR spent against the CSR obligations of the immediately succeeding 3 financial years. Para 23 of the ICAI’s Technical Guide on Accounting for Expenditure on Corporate Social Responsibility Activities requires recognition of the excess expenditure as an asset, if proposed to be carried forward to the next year to be adjusted against profits of succeeding years.

Going by the same principle as applicable in the case of Unspent CSR amount, the excess expenditure incurred by a company during a financial year will cease to exist with the cessation of existence of the transferor company. However, the excess expenditure carried forward from the previous financial year in the form of assets in the books of the transferor company, gets absorbed in the books of the transferee company as a result of merger, and therefore, benefit of the same can be availed by the transferee company, post the merger becomes effective.

d. Treatment of ongoing projects of the Transferor company

Section 135(6) provides that if the company has identified any CSR project as an ongoing project and has allocated some portion of the CSR obligations towards such project, it is required to transfer such unspent amount to the Unspent CSR Account which in turn is required to be spent within a period of 3 financial years from the date of such transfer. However, it is important to understand the fate of such an ongoing project where such a company gets merged with another company during said period of 3 years.

Consequent to the merger, the Unspent CSR Account of the transferor company also gets transferred to the transferee company. Therefore, the unspent CSR obligations with respect to an ongoing project becomes an obligation on part of the transferee company. In case the transferee company intends to spend the funds pertaining to the ongoing project in other CSR activities, the same can be spent in such a manner with an approval from the board of directors of the transferee company.

Examples:

| AD and ED | FY 20-21 | FY 21-22 | FY 22-23 | FY 23-24 | FY 24-25 |

| Case 1 AD and ED- 1st July 2022 | Transferor identified CSR ongoing project and allocated Rs. 10 lakhs to it | Transferor spent Rs. 2 lakhs towards such ongoing project | The unspent obligation of ongoing projects as on 31st March, 2022 gets transferred in an Unspent CSR Account. On 1st July 2022, the same becomes the liability of the Transferee company who will be required to spend the same in the project | Transferee company to ensure utilisation of the funds towards the ongoing project | Any amount remaining unspent will have to be transferred to the Fund specified under Schedule VII |

| Case 2 AD – 1s t April 2021 ED – 30th July 2023 | Transferor identified the CSR ongoing project and allocated Rs 10 lakhs to it. | Transferor spent 2 lakhs towards such ongoing project | Transferor spent 3 lakhs towards such ongoing project | The unspent obligation of ongoing projects as on 31st March, 2023 gets transferred in an Unspent CSR Account. On 30th July 2023, the same becomes the liability of the Transferee company who will be required to spend the same in the project |

B. Treatment of CSR in case of demerger

In case of a demerger, a division/ an undertaking of an existing company (‘Demerged company’) is separated and transferred to another existing/ new company (‘Resulting company”). Unlike in case of a merger, where one company necessarily ceases to exist post merger, in case of demerger, both the Demerged company and the Resulting company continue to survive.

The CSR obligations are calculated on a company basis, and not on the basis of the unit/ division from which the profit has been derived from. Therefore, the segregation of a unit/ division from an existing company should not have any impact on the determination of CSR obligations of a company prior to AD, during AD to ED, and post ED. Both the Demerged company and Resulting company should continue to determine CSR applicability, spending obligations, etc. on the basis of their respective financials.

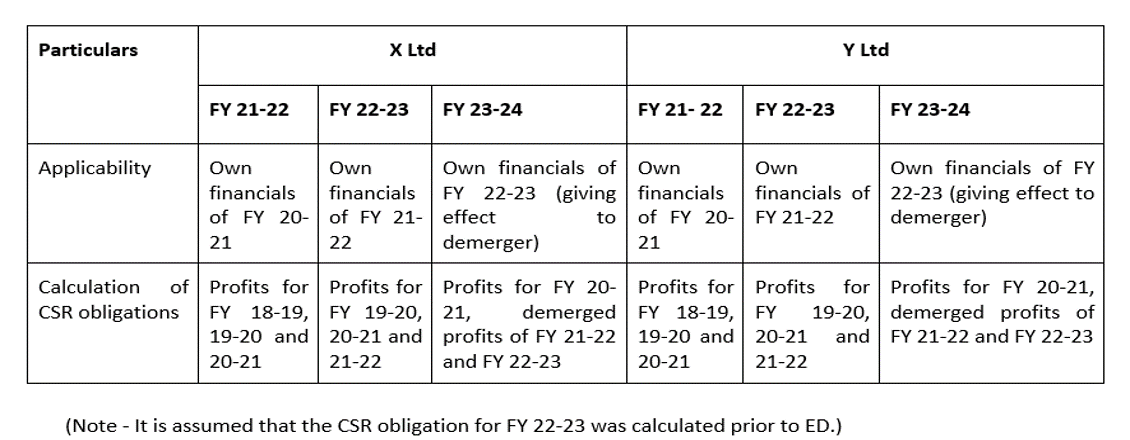

For example: A scheme of demerger has been filed for demerger of spandex business of X Ltd (Demerged company) to Y Ltd (Resulting company). The AD of the Scheme is 1st April, 2021 and the ED is 30th July, 2022. How will the CSR obligations of X Ltd and Y Ltd be determined for FY 21-22, 22-23 and 23-24?

C. Treatment of CSR in case of slump sale

A corporate action similar to demerger is “slump sale”. This involves transfer of a group of assets and liabilities, against a lump sum consideration, without apparently changing the corporate identity of a company. In such a case, there is no concept of AD/ ED, only the transferred assets and liabilities become a part of the assets and liabilities of the acquirer with effect from the date of acquisition.

In such a case, there is no concept of adjusted financials, and the CSR obligations are calculated normally on the basis of the figures appearing in the respective financial statements of the acquirer and seller.

D. Conversion of a company into other forms of entities or vice versa

The Indian laws enable a company to get itself converted into an LLP; as also permits other forms of entities to get themselves converted into a company. The provisions of CSR are applicable only to a company incorporated under the provisions of the Companies Act, including a foreign company. It does not apply in case of any other form of legal entity in India, be it a partnership firm, an LLP or any other association of persons.

Therefore, on conversion of the form of the entity, whatever unspent or excess CSR obligations remain, the same ceases to exist with the cessation of the company.

Concluding remarks

Both CSR and managerial remuneration is calculated on the basis of net profits arrived in accordance with section 198 of the Act. However, unlike managerial remuneration, CSR is based on past profits, and that too, of 3 years in the past. This is the root cause of several situations which look logically unsustainable, however, one is constrained to apply the law by referring to the average profits of the last 3 years. Change of corporate entity is not the only situation(s) where such inequitable or unjustifiable results may arise; there are several other situations too. For example, a company having had profits on an average for the last 3 years, in the 4th year, may incur a default, may wipe its net worth, or may even slip into CIRP. In such cases, looking at the historical profits and expecting the company to meet its social obligations where it is not even hand-to-mouth, may seem completely illogical. Change of corporate entity also poses such inequitable situations.

[1] C/SCA/11308/2019

Excess csr in case of demerger shall remain on original entity or will also be allocated to resulting entity

It is not clear

Para 23 of the ICAI’s Technical Guide on Accounting for Expenditure on Corporate Social Responsibility Activities recognises the excess expenditure as an asset. Transfer of all assets/ liabilities, privileges/ obligations in case of demerger is explicitly set out by way of the scheme. Hence, the treatment of excess CSR should be incorporated in the scheme of demerger. It is to be noted that there will be a limitation in filing the form CSR-2 for claiming the excess CSR amount for the resulting company. (as the form autopopulates the amount of excess from the form filed last year).