AT1 bonds: blessed with perpetuity or cursed with mortality?: Will Yes Bank write-off sensitise investors to risks of AT1 bonds?

-Financial Services Division

Introduction

In the Yes Bank restructuring proposed by the RBI[1], equity shareholders will not lose all their money, depositors, hopefully, will be fully protected, and other creditors may also sail safe. However, the first casualty is the investors in AT1 bonds, as the same have been fully written off. The returns on AT1 bonds are much lower than those on equity, and only a shade higher than those on Tier 2 bonds; however, in terms of being under the guillotine, they have come even ahead of equity. Sometimes, the risks of investing in an instrument are not understood until there is a casualty. Will the market now become jittery in AT1 investing? Will the cost of AT1 investing go up significantly, so that banks will have to cough up higher servicing costs as they raise AT1 bonds, as compared to Tier 2 bonds, unsecured bonds or secured bonds?

The article discusses the basic features of AT1 bonds and then gets into the impact of the Yes Bank write off on the market for AT1 bonds in India.

Concept of AT1 Bonds

The concept of Additional Tier-1 (AT1) Bonds was introduced by Basel III post the 2008 financial crisis, to protect depositors of a bank on a going concern basis. These bonds are also commonly known as Contingent convertible capital instruments (CoCos)[2]. AT1 or perpetual bonds are quasi debt instruments, which do not have any fixed maturity period. It bears higher risk compared with normal bonds. They are perpetuals as they do not have a redemption date, and are callable at the initiative of the issuer after a minimum period of five years. However, regulators may permit the exercise of call options within the first five years if it can be established that the bank was not in a position to anticipate the event at issuance.

If an issuing bank incurs losses in a financial year, it cannot make coupon payment to its bond holders even if it has enough cash. Further, the essential element of this instrument is that they are hybrid capital securities that absorb losses in accordance with their contractual terms when the capital of the issuing bank falls below a certain level. That is to say, in case the Common Equity Tier-1 (CET 1) ratio falls below a threshold level, the holders of such bonds shall bear the losses without the bank being liquidated.

As per the Basel III requirement, the terms and conditions of AT1 bonds must have a provision that requires such instruments, at the option of the relevant authority, to either be written off or converted into common equity upon the occurrence of the trigger event. Paragraph 55 of Basel III norms provide comprehensive criterions for an instrument to be included in Additional Tier 1 Capital. The relevant extract is reproduced herein below:

Instruments issued by the bank that meet the Additional Tier 1 criteria

- The following box sets out the minimum set of criteria for an instrument issued by the bank to meet or exceed in order for it to be included in Additional Tier 1 capital.

| Criteria for inclusion in Additional Tier 1 capital | ||

| 1. | Issued and paid-in | |

| 2. | Subordinated to depositors, general creditors and subordinated debt of the bank | |

| 3. | Is neither secured nor covered by a guarantee of the issuer or related entity or other arrangement that legally or economically enhances the seniority of the claim vis-à-vis bank creditors | |

| 4. | Is perpetual, i.e. there is no maturity date and there are no step-ups or other incentives to redeem | |

| 5. | May be callable at the initiative of the issuer only after a minimum of five years:

a. To exercise a call option a bank must receive prior supervisory approval; and b. A bank must not do anything which creates an expectation that the call will be exercised; and c. Banks must not exercise a call unless: i. They replace the called instrument with capital of the same or better quality and the replacement of this capital is done at conditions which are sustainable for the income capacity of the bank[3]; or ii. The bank demonstrates that its capital position is well above the minimum capital requirements after the call option is exercised.[4] |

|

| 6. | Any repayment of principal (eg. through repurchase or redemption) must be with prior supervisory approval and banks should not assume or create market expectations that supervisory approval will be given | |

| 7. | Dividend/coupon discretion:

a. the bank must have full discretion at all times to cancel distributions/payments[5] b. cancellation of discretionary payments must not be an event of default c. banks must have full access to cancelled payments to meet obligations as they fall due d. cancellation of distributions/payments must not impose restrictions on the bank except in relation to distributions to common stockholders. |

|

| 8. | Dividends/coupons must be paid out of distributable items | |

| 9. | The instrument cannot have a credit sensitive dividend feature, that is a dividend/coupon that is reset periodically based in whole or in part on the banking organisation’s credit standing. | |

| 10. | The instrument cannot contribute to liabilities exceeding assets if such a balance sheet test forms part of national insolvency law. | |

| 11. | Instruments classified as liabilities for accounting purposes must have principal loss absorption through either

(i) conversion to common shares at an objective pre-specified trigger point or (ii) a write-down mechanism which allocates losses to the instrument at a pre-specified trigger point. The write-down will have the following effects: a. Reduce the claim of the instrument in liquidation; b. Reduce the amount re-paid when a call is exercised; and c. Partially or fully reduce coupon/dividend payments on the instrument. |

|

| 12. | Neither the bank nor a related party over which the bank exercises control or significant influence can have purchased the instrument, nor can the bank directly or indirectly have funded the purchase of the instrument | |

| 13. | The instrument cannot have any features that hinder recapitalisation, such as provisions that require the issuer to compensate investors if a new instrument is issued at a lower price during a specified time frame | |

| 14. | If the instrument is not issued out of an operating entity or the holding company in the consolidated group (eg a special purpose vehicle – “SPV”), proceeds must be immediately available without limitation to an operating entity18 or the holding company in the consolidated group in a form which meets or exceeds all of the other criteria for inclusion in Additional Tier 1 capital | |

Incentive to issue AT1 Bonds

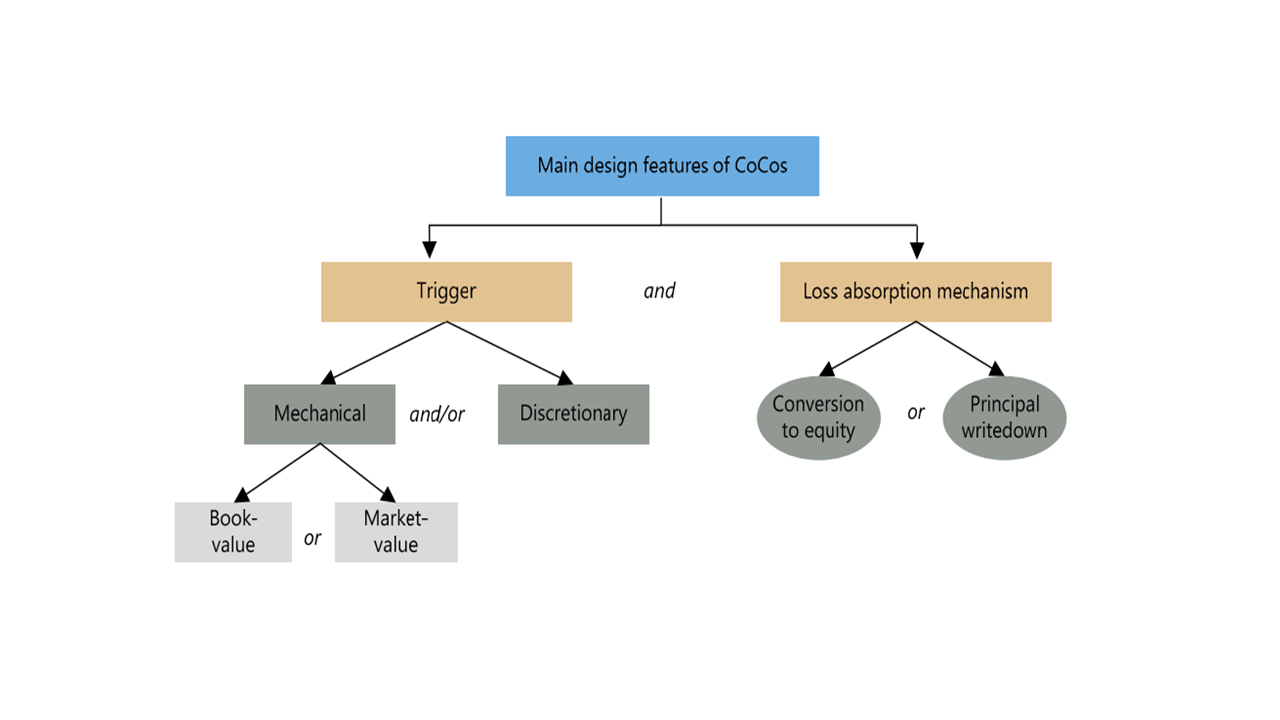

The foremost reasons for issuing AT1 Bonds is the fact that they satisfy the regulatory capital requirements. Most of the investors are private banks, mutual funds and retail investors, having a high risk appetite, while institutional investors are mostly restrained. Since the risk is higher, higher is the yield from these bonds. The rate of return is higher than those of higher-ranked debt instruments of the same issuer. It is dependent on their two factors – the trigger level and the loss absorption mechanism.

Priority order

The claims of the investors in AT1 Bonds and any interest accrued thereon is superior to the claims of investors in equity shares and perpetual non-cumulative preference shares, if any and any other securities that are subordinated to AT 1 Capital in terms of the Basel III Regulations.

However, the claims are subordinated to the claims of depositors, general creditors and any other securities of the issuer that are senior to AT 1 Capital of the Bank in terms of Basel III Regulations. Further, the stand pari passu without preference amongst themselves and other subordinated debt classified as AT1 Capital in terms of Basel III Regulations.

These bonds are neither secured nor covered by any guarantee of the issuer or any of its related entities or any other arrangement that legally or economically enhances the seniority of such claim as compared to the other creditors.

Rating of AT1 Bonds

AT1 Bonds issued by banks are usually rated by rating agencies as plain bonds even if the rating agency uses a tag ‘hybrid’. However, they are assigned ratings as applicable for bonds. Earlier, the absence of a complete set of credit ratings for AT1 Bonds was a hurdle on its growth path. According to the S&P rating methodology, an AT1 Bond rating should be at least two to three notches below the issuer’s credit rating and cannot exceed BBB+[6]. Further downward notching is applied to instruments with triggers near or at the point of non-viability and to those that have a discretionary trigger. On average, given the higher risk, the rating for these bonds is one to four notches lower than the secured bond series of the same bank. For example, while SBI’s tier II bonds are rated AAA by CRISIL, its tier I long-term bonds are rated AA+.

Pricing and Yield

Though the risk is much more than a plain or any other structured bond, however, usually NBFCs and banks offer about 200-300 basis points higher than similar maturity debentures.

Since these bonds have no maturity date they can continue to pay the coupon forever. The issuer has the option to call back the bonds or repay the principal after a period of five years. While AAA rated tier II bond of a public sector bank may have an interest rate of around 7- 7.5% per annum, its AT1 Bond can carry a rate of around 9- 10% per annum. The attraction for investors is higher yield than secured bonds issued by the same entity. But along with the high yield there are certain risks as well; the option with issuer to skip coupon payment and maintaining a CET1 ratio of 5.125%, failing which the bonds can get written down or get converted into equity.

The pricing of AT1 Bonds is consistent with their position in banks’ capital structures. The main determinants of yields are the mechanical trigger level, the loss absorption mechanism, and the existence of a discretionary trigger.

Classification as AT1 Bonds

In some jurisdictions, the respective domestic law does not allow direct issuance of perpetual debt. There can be the following possible circumstances that may be eligible for recognition as AT 1 capital:

- Dated instrument having terms and conditions that include an automatic roll-over feature,

- Instruments with mandatory conversions into common shares on a pre-defined date,

- Subordinated loans

Dated instruments that include automatic roll-over features are designed to appear as perpetual to the regulator and, simultaneously to appear as having a maturity to the tax authorities and/or legal system. This creates a risk that the automatic roll over could be subject to legal challenge and repayment at the maturity date could be enforced. As such, instruments with maturity dates and automatic roll-over features are not treated as perpetual.

An instrument may be treated as perpetual if it will mandatorily convert to common shares at a pre-defined date and has no original maturity date prior to conversion. However, if the mandatory conversion feature is combined with a call option (i.e. the mandatory conversion date and the call are simultaneous or near simultaneous), such that the bank can call the instrument to avoid conversion, the instrument will be treated as having an incentive to redeem and will not be permitted to be included in AT1 Capital.

Subordinated loans meeting all the criteria required for Additional Tier 1 or Tier 2 capital, can be included in the regulatory capital.

Write down and write-off

AT1 Bonds accounted for as liabilities are required to meet both the requirements for the point of non-viability and the principal loss absorbency requirements. To meet the point of non-viability trigger requirements, the instrument needs to be capable of being permanently written-off or converted to common shares at the trigger event. The trigger event is the earlier of[7]:

- a decision that a write-off, without which the firm would become non-viable, is necessary, as determined by the relevant authority; and

- the decision to make a public sector injection of capital, or equivalent support, without which the firm would have become non-viable, as determined by the relevant authority.

Source: CoCos: a primer

The write-down or conversion requirements for Additional Tier 1 instruments accounted for as liabilities, a temporary write-down mechanism is only permitted if it meets the following conditions:

- The trigger level for write-down/conversion must be at least 5.125% Common Equity Tier 1 (CET1).

- The write-down/conversion must generate CET1 under the relevant accounting standards and the instrument will only receive recognition in Additional Tier 1 up to the minimum level of CET1 generated by a full write-down/conversion of the instrument.

- The aggregate amount to be written-down/converted for all such instruments on breaching the trigger level must be at least the amount needed to immediately return the bank’s CET1 ratio to the trigger level or, if this is not possible, the full principal value of the instruments.

Global scenario

AT1 bonds come with the basic feature of protecting the issuer from capital losses. When the issuer is in stress, these bonds extend a helping hand by absorbing the losses. For absorbing the losses, the issuer can either write-off, write-down or convert the AT1 bonds into equity. In fact, the terms of issue of AT1 bonds specifically provide for the method of absorbing losses. Following are a few examples of the methods of absorbing losses provided in the terms of issue of AT1 bonds:

- Deutsche Bank intends of issue AT1 bonds in 2020[8], which would be subject to write-down provisions if its common equity tier 1 capital ratio will fall below 5.13%. as against 13.6% as of December 31, 2019. The securities are also subject to other loss-absorption features pursuant to the applicable capital rules.

- Kookmin Bank issued CoCo Bonds in 2019[9] which can be written off in times of stress — with an interest rate of 4.35 per cent.

Companies have, in many instances, written-off or written-down AT1 bonds. Such as:

- Erste has written-off billions of euros in AT1 bonds in 2014[10].

- Bank of Jinzhou, in 2019[11], stopped paying coupon on its CoCo Bonds to protect its financial health.

Impact on Market for AT1 Bonds

Among the investors, mostly mutual funds and several individual investors, mostly high net worth individuals (HNIs), are exposed to Yes Bank issued AT 1 Bonds which are designed to absorb losses when the capital of the bank falls below certain levels. As of January 31, 2020, 11 mutual funds had exposure worth Rs 2,819 crore to bonds of the bank. Two schemes of Bank of Baroda Mutual Fund–Baroda Treasury Advantage Fund and Baroda Credit Risk Fund had investments worth Rs 53.69 crore in Tier 1 perpetual bonds of Yes Bank. UTI Mutual Fund holds investments worth nearly Rs 50 crore worth of holding in 9.5% perpetual bonds. Indiabulls Housing Finance had invested Rs 662 crore via AT1 Bonds. Several institutional investors are planning to come together to oppose the central bank’s proposal to write down Yes Bank’s perpetual bonds. Their main contention is that tier-I bonds are senior to equity, and cannot be written down without reducing equity.

Based on the information circulating in the market, the Information Memorandum (IM) of AT1 Bonds has provisions that in case there is a reconstitution or amalgamation of the bank under Sec 45 of Banking Regulation Act 1949, the bank will be deemed as non-viable and trigger for written-down / conversion of the AT1 Bonds will be activated. However, the IM sates it cannot be written down unless equity is also reduced.

AT1 bond holders are treated like equity holders. Hence repayment is not likely for these types of bonds. The Yes Bank scheme shall be an eye opener for the investors and is expected to adversely affect the market for AT1 Bonds. This is the first time ever in India that AT1 Bond investor got a hit on their investments. It is likely that the yield on such similar bonds would increase by around 200 basis points from existing levels.

[1] https://www.rbi.org.in/Scripts/BS_PressReleaseDisplay.aspx?prid=49479

[2] https://www.bis.org/publ/qtrpdf/r_qt1309f.pdf

[3] Replacement issues can be concurrent with but not after the instrument is called.

[4] Minimum refers to the regulator’s prescribed minimum requirement, which may be higher than the Basel III

Pillar 1 minimum requirement.

[5] A consequence of full discretion at all times to cancel distributions/payments is that “dividend pushers” are prohibited. An instrument with a dividend pusher obliges the issuing bank to make a dividend/coupon payment on the instrument if it has made a payment on another (typically more junior) capital instrument or share. This obligation is inconsistent with the requirement for full discretion at all times. Furthermore, the term “cancel distributions/payments” means extinguish these payments. It does not permit features that require the bank to make distributions/payments in kind.

[6] Standard & Poor’s (2011)

[7] https://www.bis.org/press/p110113.pdf

[8] https://finance.yahoo.com/news/deutsche-db-plans-offer-additional-131801196.html

[9] https://www.ft.com/content/523a5e62-9802-11e9-9573-ee5cbb98ed36

[10]https://www.washingtonpost.com/business/a-coco-bond-at-3375percent-the-markets-still-crazy/2020/01/23/7a9435ae-3db6-11ea-afe2-090eb37b60b1_story.html

[11] https://www.wsj.com/articles/ailing-chinese-bank-stops-paying-coupons-on-coco-bonds-11567424965

Hi,

How to find AT1 bonds exposure in Mutual funds ? I couldn’t see in SID or Fact sheet or Portfolio document

The exposure to AT1 bonds is usually disclosed in the portfolio of the mutual funds that have invested in such instruments

AT1 bonds are a Basel III requirement to minimize the cost of recapitalizing banks.

RBI’s has strictly gone by the terms and conditions of the AT1 bond issues which require a permanent write-down of AT1 bonds if public sector funds are used to rescue the bank. However, had a private sector bank like HDFC Bank stepped in to rescue Yes Bank, the write-down would be only temporary and would get written back once Yes Bank starts paying dividends.

Hence, the bond trustee should be putting together a proposal for a private sector bank to step in place of SBI so that the loss suffered by AT1 bond holders is only temporary.