Summary of Important Supreme Court Judgements on IBC

Team Resolution | resolution@vinodkothari.com

Loading…

Loading…

Team Resolution | resolution@vinodkothari.com

Loading…

Should borrower be given an opportunity of being heard?

-Rhea Shah, Executive | rhea@vinodkothari.com

A recent ruling of the Supreme Court placed emphasis on the classification of an account as fraudulent and the consequences thereof. The ruling is in favour of incorporating the principles of natural justice during the process of declaring an account as fraudulent.

Fraud classification by banks and NBFCs is essentially guided by Master Directions on Frauds – Classification and Reporting by commercial banks and select FIs[1] and the Master Direction – Monitoring of Frauds in NBFCs (Reserve Bank) Directions, 2016[2], respectively (‘Fraud Directions’). However, there has been a certain extent of ambiguity as to the procedural aspects of the classification. While the basic purpose of such classification remains to ensure the early detection and reporting of a fraudulent transaction, it also entails significance in implementing a procedure that is fast and robust for the RBI to disseminate information regarding fraudulent borrowers and related parties.

Read more →By Vinod Kothari, Managing Partner, Sikha Bansal, Partner and Shraddha Shivani, Executive | corplaw@vinodkothari.com

The Supreme Court ruling in PTC India Financial Services Limited v. Venkateshwar Kari and Another is significant in many ways – not that it categorically rewrites the law of pledges which is settled with 150 years of the statute[1] and even longer history of rulings, but it surely refreshes one of the predicaments of a pledge. Importantly, since most of the pledges of securities currently are in the dematerialised format, it brings out a very important distinction between the meaning of ‘beneficial owner’ under the Depository law, and the right of the pledgee (a.k.a. pawnee or security interest holder) to cause the sale in terms of the rights arising under the pledge. Also, very importantly, the SC dwells upon the essential principle of equity of redemption in pledges and renders void any provision in the pledge agreement which allows the pledgee to make a sale of the pledged article without notice to the pledgor, or to forfeit the pledged article and convert the same as pledgee’s own property. There are also observations in the ruling that seem to give an indefinite time to the pledgee for the sale of the pledged property – this is a point that this article discusses at some length.

Read more →– Sikha Bansal, Partner and Megha Mittal, Associate (resolution@vinodkothari.com)

Preference shares, as the nomenclature suggests, represent that part of a Company’s capital which carries ‘preference´ vis-à-vis equity shares, with respect to payment of dividend and repayment of capital in case of winding up. However, the real position of preference shares may be quite baffling, given that the instrument, by its very nature, is sandwiched between equity capital and debt instruments. Although envisaged as a superior class of shares, preference shareholders enjoy neither the voting powers vested with the equity shareholders (true shareholders) nor the advantages vested with debenture-holders (true creditors). As such, the preference shareholders find themselves suspended midway between true creditors and true shareholders – hence facing the worst of both worlds[1].

The ambivalence associated with preference shares is adequately reflected in the manner various laws deal with such shares – a preference share is a part of ‘share-capital’ by legal classification[2], but can be a ‘debt’ as per accounting classification[3]; similarly, while a compulsorily convertible preference share is classified as an ‘equity instrument’[4], any other preference share constitutes external commercial borrowing[5] under foreign exchange laws. Needless to say, the divergent treatment is owed to the objective which each legislation assumes.

-Prachi Bhatia

Legal Intern at Vinod Kothari & Company

The three-judge bench of the Hon’ble Supreme Court vide its order dated 14th April, 2021, in Asset Reconstruction Limited v. Bishal Jaiswal & Anr[1] (‘ARCIL v. Bishal’) has settled the dust around acknowledgment of liability in books of corporate debtor for the purpose of section 18 of the Limitation Act; corollary to the applicability of the section to the Insolvency and Bankruptcy Code, 2016 (‘Code’). This comes in tandem with another recent order of the Hon’ble SC in LaxmiPat Surana v. Union Bank of India & Anr[2], wherein too the Apex Court upheld that acknowledgement of debt in the balance sheet would render initiation of the limitation period afresh for the purpose of filing an application under the Code.

In what seems to be the final word of law, the, vide the instant order, the Hon’ble SC further set aside the judgment set aside the Full Bench judgment of the Hon’ble NCLAT in V.Padmakumar v. Stressed Assets Stabilisation Fund[3], (‘V. Padmakumar’), wherein the Appellate Tribunal dismissed the benefit of extension of limitation to the creditors by virtue of the debt’s presentation in the books of the corporate debtor.

In this article, author humbly analyses the order of the Apex Court in ARCIL v. Bishal in light of the catena of preceding judgements both in favour and against the ratio-decidendi in ARCIL v. Bishal.

-Sikha Bansal & Megha Mittal

While in general, in order to classify a transaction as a related party transaction, one needs to first determine whether the parties involved are ‘related parties’; however, in a recent case Phoenix Arc Private Limited v. Spade Financial Services Limited & Ors.[1] (‘Ruling’), the Hon’ble Supreme Court (‘SC’) has deduced ‘relationship’ between the parties on the basis of the underlying transactions.

The SC has read the definitions of ‘financial creditor’ and ‘related party’ (in relation to the corporate debtor) under sections 5(7) and section 5(24), respectively, of Insolvency and Bankruptcy Code, 2016 (‘Code’), in light of the ‘collusive arrangements’, ‘and ‘extensive history demonstrating interrelationship’ among the parties. Broadly put, it was held that the board/directors of these companies were ‘acting’ under the pervasive influence of common set of individuals, having ‘deeply entangled’ interrelationships. Besides, the SC refused to entertain the entities as financial creditors, as the debt was merely an eye-wash, arising out of sham and collusive transactions.

Therefore, the Ruling, in a way, uses ‘smoke’ to trace if there is a ‘fire’. The presence of collusion, entangled interrelationships, etc. have been seen as indicators suggesting that the parties were in fact ‘related’ and are thus ineligible to occupy seats in the committee of creditors.

This article touches upon the significant aspects of the Ruling, including how this ‘smoke-test’ used by the SC can act as a precedent in interpreting the provisions of the Code, specifically those relating to related parties.

-Megha Mittal

Ishika Basu

In view of the rising need to fill critical gaps in the corporate insolvency framework like last-mile funding and safeguarding the interests of resolution applicants, certain amendments were introduced by way of the Ordinance dated 28.12.2019[1], which were later on incorporated in the Insolvency Bankruptcy Code (Amendment) Act, 2020 (“Amendment Act”). The amendments inter-alia introduction of threshold for filing of application by Real-Estate Creditors, colloquially ‘Home-Buyers’ and section 32A for ablution of past offences of the corporate debtor, were made effective from 28.12.19 i.e. the date of Ordinance.

While the Ordinance introduced several amendments[2], clarificatory as well as in principles, apprehensions were raised against proviso to section 7 (1), that is, threshold for filing of application by Home-Buyers, the ablution provision introduced by way of section 32A, and clarification under section 11 dealing with the rights of a corporate debtor against another company. As such, various writ petitions were filed under Article 32 of the Constitution, alleging that the aforesaid amendments were in contravention of the fundamental rights viz. Article 14 which deals with the equality before law and equal protection of law; Article 19(1)(g) deals with fundamental right to trade, occupation, and business; and Article 21 deals with the right to life and personal liberty.

Now, after a year of its effect, the Hon’ble Supreme Court vide it order dated 19.01.2021, in Manish Kumar V/s Union of India, upheld the constitutional validity of the third proviso to section 7(1) and section 32A, setting aside all apprehensions against their insertion.

In this article, the Authors analyses the order of the Hon’ble Supreme Court, with respect to the threshold on filing of application by real-estate creditors, and section 32A.

This article has also been published in the LawStreetIndia blog – http://www.lawstreetindia.com/experts/column?sid=466 Liability Acknowledgment & Limitation Period for IBC Applications – Deciphering the Enigma -Sikha Bansal (resolution@vinodkothari.com) The applicability of the Limitation Act, 1963 (Limitation Act) to the applications under the Insolvency and Bankruptcy Code, 2016 (Code) has been settled long back, after a series of […]

Siddhart Goel

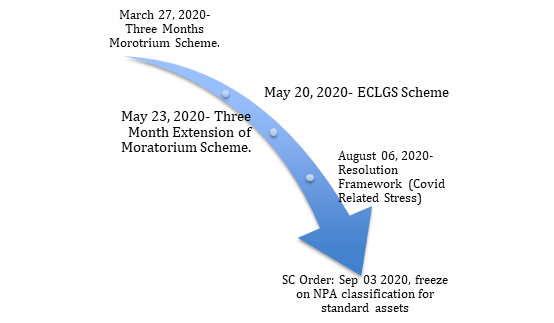

On September 03, 2020 the Hon’ble Supreme Court (the “court”) while dealing with several petitions on account of Covid related stress from various stakeholders, passed an interim order that that the accounts which have not declared NPA till August 31, 2020 shall not be declared NPA till further orders of the court.[1] Further in its September 10, 2020 order the court asked the government and RBI to file affidavit within two weeks to the court, on issues raised and relief granted thereto.[2]

The primary contention raised before the court for consideration was that the moratorium postpones the burden and does not eases the plight. It would be a double whammy on borrowers since Banks are charging compounded interest, and banks have benefitted during moratorium by charging compounded interest from customers. The court in its order dated September 10, 2020 observed that individuals are more adversely affected during this period of pandemic. Therefore, the court from the government and RBI, with regard to charging of compound interest and credit rating/downgrading during moratorium period, has sought specific instructions.

Though the matter is sub judice, this write-up aims to provide a legal analyses to the contentions raised in front of the court on the above counts, since any action or direction on the above issues will have an impact on the wider financial system including all, i.e. borrowers, government, banks and other financial institutions as a whole.

Before directly getting into the analyses, it is important to consider material reliefs and incentives announced by RBI and Government of India in respect to COVID19 related regulatory package. A brief history of timelines on series of regulatory reforms to cope with the disruptions caused due to COVID19 is provided below:

The moratorium scheme deferred the repayment schedule for loans, and the residual tenor, was to be shifted across the board. This essentially meant that all the liabilities of customers towards their repayments (principal plus interests) were to be rescheduled and shifted across the board by the Banks and NBFCs. However, the scheme clearly stipulated that the interest should continue to accrue on the outstanding portion of the term loans during the moratorium period. Moratorium granted to the customers of banks and NBFCs was to reprieve borrowers from any immediate liability to pay. However, charging of interest on outstanding accrued amount is the center of concern in the matter.

The money has time value, which is often expressed as interest in banking parlance. This is one of the most fundamental principles in finance. Rupee 1 today is more valuable from a year today. If interest is not paid, when it accrues, this in effect means, right to receive interest, which is a predictable stream of cash flow, is not available for reinvestment. Therefore, interest earned but not paid, should earn interest until paid. In debt markets, an obligation towards debt is valued in reference to yield to maturity or present value, all these rest on the compounding interest. These are generally in form of obligations on Banks and NBFCs on the liability side of their balance sheet. Bank deposits and interest thereon also attracts interest, which is adjusted towards total deposit amount of the customer. Therefore, interest on interest is a rule in finance and not a selective event.

Banking is no different to any other commercial business, besides it involves liquidity and maturity transformation and hence is highly leveraged. The short-term demand deposits from customers are converted into long-term loans to borrowers (‘maturity transformation’). Similarly, the customer deposits (liabilities of banks) are payable on demand, while on asset side receivables (repayment of principal and interest) are fixed on due dates (‘liquidity transformation’). It would be wrong to presume that NBFCs are any different from commercial banks. NBFCs largely rely on borrowings from Banks and other financial institutions by way of issuing debt instruments (CP, bonds, etc.), which is reflected on the asset side of the investing commercial banks and other financial institutions. Though obligation of payment on these debt instruments is not payable on demand, but they carry a substantial roll over and default risk. Hence, these institutions are highly leveraged and inherently fragile by nature of their business. Needless to state that receivables on asset side of banks and NBFC also carry certain risk of default and therefore are inherently risky in nature.

Financial institutions and other investors in market, (like Money Market Funds, Pension funds and etc.) invest in debt of Banks and NBFCs on the basis of strength of assets held by them. These assets are in form of receivables from pool of loans or by way advances to underlying borrowers. Thus, participants in financial markets are highly interlinked and are adversely affected by asset deterioration as a rule. Banks and financial institutions bear credit risk (default risk) of the underlying borrowers on their balance sheet. This credit risk has already increased substantially and would be unfolding further due the impact of pandemic on wider economy.

The waiver of interest charged on interest accrued but not paid during the moratorium, would not only be a loss for the banks and NBFCs, but would also substantially dilute the value of assets held by them. This could lead to an asset liability mismatch on balance sheets of banks. Such waiver of interest on accrued amount could exacerbate the risk of banks and NBFCs defaulting on other financial institutions (‘systemic risk’). The foregoing of charging of interest on interest accrued during moratorium would mean banks and financial institutions partially baling out borrowers either from their own limited funds or from the borrowed funds of other financial institutions. Such a move could entail systemic risk and wider financial catastrophe. As risk of default from comparatively large diversified group of borrowers will be shifted and get concentrated in the balance sheets of banks and financial institutions.

The RBI moratorium notification dated March 27, 2020, freezes the delinquency status of the loan accounts, which have availed moratorium benefit under the scheme. This essentially meant that asset classification standstill will be imposed for accounts where the benefit of moratorium have been extended.[3] As it stands, the RBI, March 27, 2020 circular clearly stipulated that moratorium/deferment/recalculation of loans is provided to borrowers to tide over economic fallout due to COVID and same shall not be treated as concession or change in terms and conditions due to financial difficulty of the borrower. In essence the rescheduling of payments and interest is not a default and should not be reported to Credit Information Companies (CICs). A counter obligation on CIC was also imposed to ensure credit history of the borrowers is not impacted negatively, which are availing benefits under the scheme. The relevant excerpt from the notification stipulates as follows:

“7. The rescheduling of payments, including interest, will not qualify as a default for the purposes of supervisory reporting and reporting to Credit Information Companies (CICs) by the lending institutions. CICs shall ensure that the actions taken by lending institutions pursuant to the above announcements do not adversely impact the credit history of the beneficiaries.”

Further through notifications dated August 06, 2020 RBI introduced a special window scheme for Resolution of stress on account of COVID 19 (“Special Window”). Banks and financial institutions could restructure the eligible accounts under the Special Window without any asset classification downgrade of borrowers. The Special Window scheme included personal loans to individuals and other corporate exposures. It is relevant to realize that the resolution of stressed assets is highly subjective to borrower’s leverage, sector specific risks, and other financial parameters. Banks and Financial institutions are better placed to implement the resolution or restructuring of the assets (loan accounts) at bank level.

The moratorium scheme and the Special Window resolution framework dated August 06, 2020 (the “Schemes”) were highlights of discussions during the court proceedings extensively. The primary contentions were in respect to limited applicability of these schemes. The schemes and their benefits were available to borrowers whose accounts were standard and not more than 30 DPD as on March 01, 2020 with their respective banks and financial institutions. Though the legal validity of the schemes were questioned directly in front of the court, but selective nature of schemes conferring benefit on to standard accounts (which are not more than 30 DPDs) only. The exclusion of other borrower accounts was criticised extensively. But this could form as a part of separate issue, the primary concern here being asset down gradation and credit rating scores.

The Special Window restructuring scheme notification under its disclosures and credit reporting section made an onus on lending institutions to make disclosures on such re-structured assets in their annual financial statements along with other disclosures. However where accounts have been restructured under special facility, and involve ‘renegotiations’, it shall qualify as restructuring and the same shall be governed under credit information polices as applicable. The relevant clause is produced as is herein below:

“54. The credit reporting by the lending institutions in respect of borrowers where the resolution plan is implemented under this facility shall reflect the “restructured” status of the account if the resolution plan involves renegotiations that would be classified as restructuring under the Prudential Framework. The credit history of the borrowers shall consequently be governed by the respective policies of the credit information companies as applicable to accounts that are restructured.”

It is argued that the area of application and scope of both the schemes are entirely exclusive and independent remedies available to respective eligible borrowers. Under moratorium scheme the borrower gets benefit of liquidity since all the payments due during the period are deferred. While in the latter, i.e. restructuring scheme the borrower under stress can get their accounts restructured by way of implementing resolution plan without facing any asset classification downgrade upfront. In the latter case, only such restructurings involving ‘renegotiations’ will affect the credit history of the borrowers.

The intention of the RBI and the government was to provide relief to the borrowers, who were gasping for relief after the disruptions caused due to COVID 19. There is no doubt that the COVID-19 outbreak and subsequent lockdown has impacted all level of borrowers, ranging from small to large borrowers, including, individuals to corporates. It would be wrong to presume that those accounts, which were NPA or otherwise ineligible under the schemes, are not affected by the pandemic. Therefore it is always open for the government and RBI to introduce or implement any other scheme or some sort of reprieving mechanism for the ineligible borrowers. However, it is important to consider that even banks and financial institutions are no exception like any other businesses that have been affected by the pandemic; moreover they have been exposed to severe liquidity crunch and on the flip side are witnessing asset quality problems on their balance sheets. Any attempts to tamper or distort with the fundamental principle of finance (‘interest on interest’) or shifting the burden of it on banks and other financial institutions could have a much wider systemic ramifications than the current economic stress.

[1] https://main.sci.gov.in/supremecourt/2020/11127/11127_2020_34_16_23763_Order_03-Sep-2020.pdf

[2] https://main.sci.gov.in/supremecourt/2020/11127/11127_2020_36_1_23895_Order_10-Sep-2020.pdf

[3] Our detailed write up asset classification standstill is available at < http://vinodkothari.com/2020/04/the-great-lockdown-standstill-on-asset-classification/>