The most reliable way to predict the future is to create it

– Abraham Lincoln

Surely, Lincoln did not have either securitisation or predictability in mind when he wrote this motivational piece; however, there is an interesting and creative use of securitisation methodology, to raise funding based on cashflows which have some degree of predictability. In many businesses, once an initial framework has been created, cashflows trickle over time without much performance over time. These situations become ideal to use securitisation, by pledging this stream of cashflows to raise funding upfront. Surely, traditional methods of on-balance-sheet funding fail here, as there is very little assets on the balance sheet.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2024-03-04 15:46:002024-03-14 13:11:08The Promise of Predictability: Regulation and Taxation of Future Flow Securitization

This quote by Beethoven remains relevant today, not only within the music industry but also in the realm of finance. In the continually evolving landscape of finance, innovative strategies emerge to monetize various assets. One such groundbreaking concept gaining traction in recent years is music royalty securitization. This financial mechanism offers investors a unique opportunity to access the lucrative world of music royalties while providing artists and rights holders with upfront capital.

The roots of this innovative financing technique can be traced back to the 1990s when musician David Bowie made history by becoming the first artist to securitize his future earnings through what became known as ‘Bowie Bonds’. This move not only garnered attention but also paved the way for other artists to follow suit. Bowie Bonds marked a significant shift in how music royalties are bought, sold, and traded.

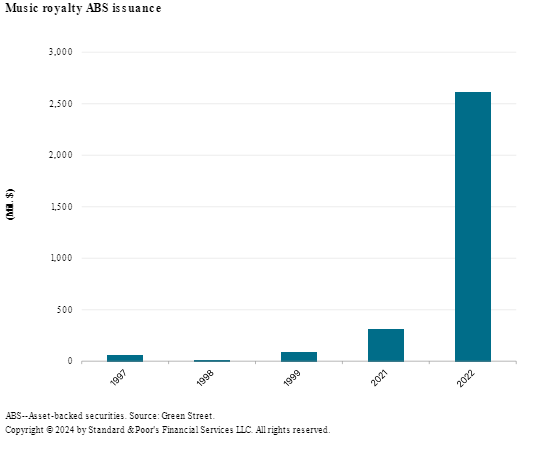

As per the S&P Global Ratings[1], the issuance of securities backed by music royalties totaled nearly $3 billion over the two-year span 2021-22. The graph below shows a recent surge in issuance of securities backed by music royalties.

Data showing the growth of Music Royalty Securitization

This article discusses music royalty securitization, its mechanics, benefits, challenges along with implications for the music industry.

Understanding Music Royalties:

Before exploring music royalty securitization, it’s essential to understand the concept of music royalties. In the music industry, artists and rights holders earn royalties whenever their music is played, streamed, downloaded, or licensed for use. These royalties are generated through various channels, including digital platforms, radio, TV broadcasts, live performances, and synchronization licenses for commercials, movies, and TV shows. However, it’s important to note that artists only earn royalties when their music is utilized, whether through sales, streaming, broadcasting, or live performances.

As a result, the cash flows from these royalties being uncertain are received over time and continue to be received for an extended period. Consequently, artists experience a delay in receiving substantial amounts from these royalties, sometimes waiting for several years before seeing significant income.

The Birth of Music Royalty Securitization:

Securitization involves pooling and repackaging financial assets into securities, which are then sold to investors. The idea is to transform illiquid assets, such as mortgage loans or in our case, music royalties, into tradable securities. Music royalty securitization follows a similar principle, where the future income generated from music royalties is bundled together and sold to investors in the form of bonds or other financial instruments.

Future Flows Securitization:

Music royalty securitization is a constituent of future flows securitization and therefore before discussing the constituent, it is important to discuss the broader concept of future flows securitization.

Future flows securitization involves the securitization of future cash flows derived from specific revenue-generating assets or income streams. These assets can encompass a wide range of future revenue sources, including export receivables, toll revenues, franchise fees, and other contractual payments, even future sales. By bundling these future cash flows into tradable securities, issuers can raise capital upfront, effectively monetizing their future income. Future flows securitization differs from the traditional asset backed securitization by their very nature as while the latter relates to assets that exist, the former relates to assets that are expected to exist. There is a source, a business or infrastructure which already exists and which will have to be worked upon to generate the income. Thus, in future flows securitization the income has not been originated at the time of securitization. The same can be summed up as: In future flow securitization, the asset being transferred by the originator is not an existing claim against existing obligors, but a future claim against future obligors.

Mechanics of Music Royalty Securitization:

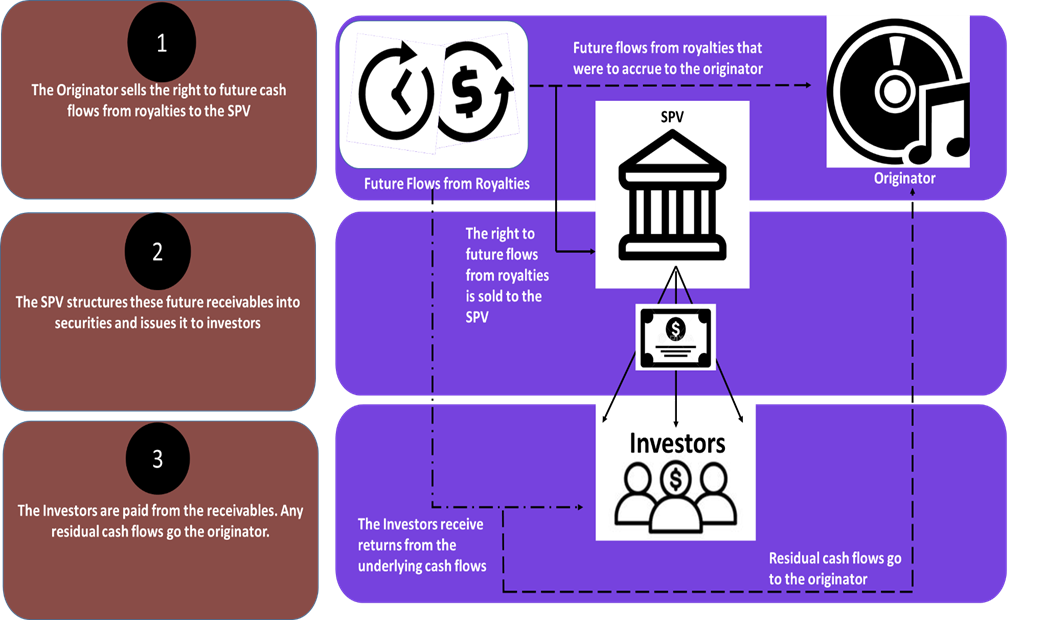

Music royalty securitization involves packaging the future income streams generated by music royalties into tradable financial instruments. The process begins with the identification of income-generating assets, which are then bundled into a special purpose vehicle (SPV). The SPV issues securities backed by these assets, which are sold to investors. The revenue generated from the underlying music royalties serves as collateral for the securities, providing investors with a stream of income over a specified period.

The process of music royalty securitization typically involves several key steps:

Asset Identification: Rights holders, such as artists, record labels, or music publishers, identify their future royalty streams eligible for securitization.

Valuation: A valuation is conducted to estimate the present value of the anticipated royalty income streams. Factors such as historical performance, market trends, and artist popularity are taken into account.

Selling the future flows: The future flows from royalties are then sold off to the Special Purpose Vehicle (SPV) to make them bankruptcy remote. The sale entitles the trust to all the revenues that are generated by the assets throughout the term of the transaction, thus protecting against credit risk and sovereign risk as discussed later in this article.

Structuring the Securities: These future cash flows are then structured into securities. This may involve creating different tranches with varying levels of risk and return.

Issuance: The securities are then issued and sold to investors through public offerings or private placements. The proceeds from the sale provide upfront capital to the rights holders.

Revenue Collection and Distribution: The entity responsible for managing the securitized royalties collects the revenue from various sources which is then distributed to the investors according to the terms of the securities.

Importance of Over-collateralization:

Over-collateralization is an important element in music royalty securitization. In music royalty securitization and in all future flows transactions in general, the extent of over-collateralization as compared to asset backed transactions is much higher. The same is to protect the investors against performance risk, that is the risk of not generating sufficient royalty incomes. Over-collateralization becomes even more important since subordination structures generally do not work for future flow securitizations. This is because the rating here will generally be capped at the entity rating of the originator.

Why go for securitization ?

Now the question may arise as to why an artist or a right holder of a royalty has to go for securitization of his music royalties in order to secure funding. Why cant he simply opt for a traditional source of funding ? The answer to this question is two folds:

Firstly, the originator in the present case generally has no collateral to leverage and hardly there will be a lender willing to advance a loan based on assets that are yet to exist.

Secondly even if they are able to obtain funding it will be at a very high cost due to high risk the lender perceives with the lending.

Music royalty securitization, could be his chance to borrow at a lower cost. The cost of borrowing is related to the risks associated with the transaction, that is, the risk the lender takes on the borrower. Now, this risk includes performance risk, that is the risk that the work of the originator does not generate enough cash flows. While this risk holds good in case of securitization as well, it however takes away two major risks – credit risk and sovereign risk.

Credit risk, as divested from the performance risk would basically mean that the originator has sufficient cash flows but does not pay it to the lender. This risk can be removed in case of a securitization by giving the SPV a legal right over the cash flow.

Sovereign risk on the other hand emanates only in case of cross-border lending. This risk arises when an external lender gives a loan to a borrower whose sovereign later on in the event of an exchange crises either imposes a moratorium on payments to external lenders or may redirect foreign exchange earnings. This problem is again solved by giving the SPV a legal right over the cash flows from the royalties arising in countries other than the originator’s, therefore trapping cash flow before it comes under the control of the sovereign.

The lack of these two types of risks might reduce the cost of borrowing for the originator; thus making music royalty securitization a lucrative option.

Accounting Treatment:

As discussed, there is no existing asset in a music royalty transaction. In terms Ind AS 39, an entity may derecognize an asset only when either the contractual rights to the cash flows from the financial asset have expired or if it transfers the financial asset. However, here asset means an existing asset and a future right to receive does not qualify as an asset in terms of the definition under Ind AS 32.

Accordingly, the funding obtained through the securitization of music royalties should be shown as a liability in books as the same cannot qualify as an off-balance sheet funding.

Regulatory Framework in India:

It is crucial to discuss the applicable regulatory framework on securitization currently prevalent in India and whether music royalty securitization would fall under any of these:

Master Direction – Reserve Bank of India (Securitization of Standard Assets) Directions, 2021(‘SSA Master Directions)

SEBI (Issue and Listing of Securitised Debt Instruments and Security Receipts) Regulations, 2008 (SDI Framework)

Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002

While the SSA Master Directions primarily pertain to financial sector entities, and will not directly apply to this domain; however, there exists a possibility that the securitization of music royalties could fall under the purview of SEBI’s SDI Framework.

Music royalty securitization offers a range of benefits for both investors and rights holders:

Diversification: Investors gain exposure to a diversified portfolio of music royalties, potentially reducing risk compared to investing in individual songs or artists.

Steady Income Stream: Music royalties often provide a stable and predictable income stream, making them attractive to income-oriented investors, such as pension funds and insurance companies.

Liquidity: By securitizing music royalties, rights holders can access immediate capital without having to wait for future royalty payments, providing liquidity for new projects or business expansion.

Risk Mitigation: Securitization allows rights holders to transfer the risk of fluctuating royalty income to investors, providing a hedge against market uncertainties and industry disruptions.

Challenges and Considerations:

While music royalty securitization presents compelling opportunities, it also poses certain challenges and considerations:

Market Volatility: The music industry is subject to shifts in consumer preferences, technological disruptions, and regulatory changes, which can impact the value of music royalties.

Due Diligence: Thorough due diligence is essential to assess the quality and value of music assets, including considerations such as copyright ownership, market demand, and revenue potential.

Potential Risks:

Market Risk: Changes in consumer behavior, technological advancements, or regulatory developments could impact the value of music royalties.

Legal Risk: Disputes over ownership rights, copyright infringement, or licensing agreements could lead to litigation and financial losses.

Concentration Risk: Investing in a single music catalog or genre exposes investors to concentration risk if the popularity of that catalog or genre declines.

Cash Flow Variability: While music royalties can provide steady income, fluctuations in streaming revenues or changes in licensing agreements may affect cash flow stability.

Reputation Risk: The success of music royalty securitization depends on the ongoing popularity and commercial success of the underlying music assets. Negative publicity, controversies, or declining relevance can adversely affect investor confidence and returns.

Implications for the Music Industry:

While music royalty securitization presents exciting opportunities, it also raises certain considerations for the music industry:

Artist Empowerment: Securitization can empower artists by providing them with alternative financing options and greater control over their financial destiny.

Industry Evolution: The emergence of music royalty securitization could reshape the traditional music business model, fostering innovation and collaboration between artists, labels, and investors.

Way Forward

Music royalty securitization offers a compelling investment opportunity for investors seeking exposure to the lucrative music industry. By securitizing future royalty streams, music rights owners can unlock liquidity while providing investors with access to a diversified portfolio of music assets.

As the music industry continues to evolve, music royalty securitization is likely to play an increasingly prominent role in the financial landscape, providing new avenues for capital deployment and revenue generation. It has the potential to transform the rhythm of creativity into the melody of investment opportunity.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00executivehttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngexecutive2024-02-26 16:24:482024-03-14 13:07:56Securing the Beat: Tuning into Music Royalty Securitization

Sale and leaseback (SLB) transactions are one of the most innovative, and in the past history of lease transactions, one of the most maligned transaction types. All over the world, there have been hundreds of rulings where SLB transactions have been challenged; in many cases, there were upheld and their sanctity was preserved, in many other cases, they have been treated either as no valid lease transactions, or pure financing transactions.

Motivations

There may be various motivations for a lessee to get into an SLB:

Liquidity – while normal lease transactions do not lead to cash in the hands of the lessee, SLBs do, SLBs extend leasing to a device of unlocking of investment. The money raised by SLBs is like general purpose corporate funding – it may be used for any purpose as the lessee may choose.

Putting assets off the books – A selling lessee may put the asset being sold off the books, if the SLB is properly structured as a sale and operating leaseback.

Financial restructuring – if the money raised by an SLB is used to pay off on-balance sheet liability, the SLB may have twin effects on the balance sheet. By putting fixed assets off the books, it reduces operating leverage, and by reducing liabilities, it reduces financial leverage.

Capturing revaluation gains – assume there are assets where the carrying values as per books are significantly lower as compared to the fair market value. In such cases, if the SLB is properly structured as operating leaseback (other conditions also need to be satisfied), the gain on the sale of the asset may be booked as realized gain (not just a revaluation surplus), and may be taken to shareholders’ equity.

Tax benefits – many SLBs, such as those of cars, furniture, etc., may be designed to accelerate the tax write off of the lessee by moving from depreciation to rental write off.

Acceleration of VAT set off – an entity having substantial amount of carry forward of input tax credit may accelerate the set off by making a sale of capital assets.

Why SLBs walk on Achilles’ heels:

An SLB transaction has the apparent looks of a financial transaction. There is only a transfer of legal title over the asset. The asset stays with the lessee. In practice, parties may take quite callous approach evaluating the asset, and may take a purely lessee exposure, in which case, most often lessor may not bother about valuation of the asset. In many cases in the past, assets have been found not even to be existing.

Besides, in many cases, lessees in SLBs have been motivated either by a funding motive, or one of booking profits on the sale of the asset. Therefore, lessees may have aggressively overvalued assets.

In India, one of the ill-famed example of SLBs has been the SLB of electric meters by state electricity boards (SEBs). SEBs, starved of funding, were advised to use the innovative funding device of leasing back electric meters that were installed in consumers’ premises. Leasing companies (and in fact, many entities not in leasing business at all), starved of tax benefits, were easily attracted to this option, as it was contended that electric meters qualify for 100% depreciation. Many SLB transactions of electric meters happened around 1996-1997. Many of these cases have already traveled long routes of litigation. Some High courts have challenged them as being pure financing devices. Some have respected them, merely based on the legal nature of the contract.

In one of the recent rulings before the Madras High court, electric meters were shown to have been bought on 30th March – hence, used for just one day. In fact, meters actually bought by the selling SEB only a few months back were heavily revalued too. Despite such glaring facts, the Madras High court still went by the legal form, and upheld the lessor’s claim to depreciation.

Electric meters is not the only thing – many weird assets such as glass bottles, gas cylinders, tools, jigs, and so on have been sold and taken back on lease. In recent past, we have noticed transactions structured to give lessees a rental write off – hence, SLBs of sanitary fittings, office fitouts, office interiors, wall panels, false ceilings, etc have commonly been done.

As most of these transactions are factually very weak, SLB transactions continue to look like money lending transactions.

Types of SLBs:

First of all, the most essential distinction will be on – is it a new asset or old asset? Since it is SLB, sure enough, it is not a new asset being acquired by the lessee, but the moot question is – has the asset been subject to use for a long period? There are cases where lessees might have recently bought assets, and may now want to get them off the books. Needless to say, older the asset, more serious the concerns, as the chances of overvaluation, or sale of decrepit assets purely with financial motives, etc., go up.

From accounting viewpoint, SLBs may be sale and financial leasebacks, and sale and operating leasebacks. We discuss the implications under the caption accounting issues.

Note that the following is not a case of sale and leaseback – X has leased an asset to Y, and X now sells the leased asset to Z, such that now the lease continues between Z and Y.

Lease and leasebacks are also not sale and leasebacks. A lease and leaseback transaction may be structured from variety of viewpoints – longer lease out, and shorter leaseback, or financial lease out and operating leaseback, etc.

Legal issues

First key question is – is an SLB legally valid as a lease? US Supreme Court discussed the legal validity of SLBs in the famous ruling of Frank Lyon and Company. The questions on the legal validity of an SLB are in fact questions which are germane to the validity of any lease. By way of a quick check (each of the factors below are negatives):

The asset being sold might have become an immovable property.

The asset being sold may have become inseparable part of another asset.

The lessor may not have done anything to indicate that the lessor is really interested in the asset, or that the asset is a genuine purchase of an asset. Facts may indicate that the lessor merely went by the financials of the lessee.

The asset may have been subject matter of third party rights. For example, the asset might already have been leased to a third party, in which case, it cannot be sold without the concurrence of the third party. The asset might have been encumbered, and so on.

In not-so-extreme cases, the asset may not at all exist, or may have outlived its life.

If facts are strong, there is nothing to challenge the legal validity of an SLB, merely because it is an SLB and not a lease of a new asset. Of course, the lessor must do everything that a prudent man would do, if really buying an asset for good value.

Income Tax issues

In case of assets which have already been depreciated by the lessee prior to their sale, income-tax law has an explanation below section 43 (1) whereby the tax WDV in the hands of the lessor will be the tax WDV in the hands of the selling lessee. That is to say, the actul sale price of the asset will be ignored, and the seller’s WDV will become the WDV of the acquiring lessor. Obvious enough, if the asset has not been depreciated by the seller, the provision does not apply. If the asset has been sold in the same financial year in which it is acquired, the seller does not claim tax depreciation.

Other than the above specific SLB-directed provision, in actual practice, tax officers question eligibility of financial lease transactions to depreciation for the lessor or rental write off for the lessee. The real culprit for tax purposes is not a financial lease, but such a lease which is a disguised financial transaction, particularly transactions containing options to buy at bargain prices. SLB transactions may especially be targeted as engineered to produce an artificial tax shelter – for example, a sale of office furniture which is taken back on lease.

VAT issues

VAT is one of the least understood implications – in fact, for VAT purposes, SLBs are no different from any other sales. Where capital assets are sold by the selling lessee, the sale is a taxable sale (assuming the seller is in some business where he generates taxable sales). Presumably, when the asset was acquired, it might have been acquired either under CST, or it might have been imported, or might have been acquired under some state VAT law (that is, the asset was acquired after introduction of VAT laws in the country). If the asset had suffered VAT at the time of its purchase, such VAT might have been eligible for set off (assuming the capital asset was not one of the negative-listed capital asset). If the asset was bought under CST or was an imported asset, the question of any VAT set off at the time of acquisition would not arise at all.

In any case, the sale of the asset would certainly be a local sale. The question of an SLB being an inter-state sale does not arise at all. The local sale will be chargeable to VAT. Of course, if the selling lessee has carry forward of input tax credit, the same can be claimed against the VAT on the sale of the capital asset.

As the asset is taken back on lease, there is clearly a VAT on lease rentals. This is also off-settable by lessee.

In the hands of the lessor, the VAT paid on the purchase of the asset is off-settable in the same manner as any other VAT.

Accounting standards

Accounting standards distinguish between SLB where the leaseback is financial, and SLB where the leaseback is operating.

If the leaseback is financial, the fact of sale of the asset is completely disregarded. No profit is booked on the sale of the asset, as there is no accounting sale of the asset at all. The amount of funding raised by the sale of the asset appears as a liability on the books of the lessee.

If the leaseback is operating lease, the asset goes off the books, and the funding realized does not come as a liability, Any gain or loss on the sale of the asset is a realized gain, and is taken to profit and loss. In fact, there is something even further: if the sale price is not fair market value of the asset, profits are recognized based on the fair market value of the asset.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Staffhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngStaff2021-08-20 11:41:152021-08-20 11:41:15Sale and leaseback transactions: Walking once again on Achilles’ Heels

With this, one of the main areas of concern happens to be capital relief for securitisation. The concerns arise not just for new exposures but also existing securitisation exposures, as Chapter VI (dealing with Capital Requirements) shall come into immediate effect, even for the existing securitisation exposures.

Earlier, due to the implementation of Ind-AS, concerns arose with respect to capital relief treatment as most of the securitisation exposures did not qualify for derecognition under Ind-AS. However, on March 13, 2020, RBI came out with Guidance on implementation of Ind-AS, which clarified the issue by stating that securitised assets not qualifying for derecognition under Ind AS due to credit enhancement given by the originating NBFC on such assets shall be risk weighted at zero percent. However, the NBFC shall reduce 50 per cent of the amount of credit enhancement given from Tier I capital and the balance from Tier II capital.

Once again, the issue of capital relief arises as the draft guidelines may cause an increase in capital requirements for existing exposures.

Capital requirement under the Draft Framework

The Draft Framework lays down qualitative as well as quantitative criteria for determining capital requirements. As per Para 70, lenders are required to maintain capital against all securitisation exposure amounts, including those arising from the provision of credit risk mitigants to a securitisation transaction, investments in ABS or MBS, retention of a subordinated tranche, and extension of a liquidity facility or credit enhancement. For the purpose of capital computation, repurchased securitisation exposures must be treated as retained securitisation exposures.

The general provisions for measuring exposure amount of off-balance sheet exposures are laid down under para 71-78 of the Draft Framework.

The quantitative conditions are however, laid down in paragraphs 79 (a) and (b). The intention here is to delve into the impact of the quantitative conditions only, keeping aside the qualitative conditions for the time being.

Substantial transfer of credit risk:

The first condition (79(a)) is that significant credit risk associated with the underlying exposures of the securities issued by the SPE has been transferred to third parties. Here, significant credit risk will be treated as having transferred if the following conditions are satisfied:

If there are at least three tranches, risk-weighted exposure amounts of the mezzanine securitisation positions held by the originator do not exceed 50% of the risk-weighted exposure amounts of all mezzanine securitisation positions existing in this securitisation;

In cases where there are no mezzanine securitisation positions, the originator does not hold more than 20% of the exposure values of securitisation positions that are first loss positions.

Taking each of the two points at a time.

The first clause contemplates a securitisation structure with at least three tranches – the senior, the mezzanine and the equity. Despite the presence of three tranches, the condition for risk transfer has been pegged with the mezzanine tranche only, however, nothing has been discussed with respect to the thickness of the mezzanine tranche (though the draft Directions has prescribed a minimum thickness for the first loss tranche).

If the language of the draft Directions is retained as is, qualifying for capital relief will become very easy. This can be explained with the help of the following example.

Suppose a securitisation transaction has three tranches, the composition and proportion of which has been provided below:

Tranche

Rating

Proportion as a part of the total pool

Retention by the Originator

Effective retention of interest by the Originator

Senior Tranche – A

AAA

85%

0%

0%

Mezzanine Tranche – B

AA+

5%

50%

2.5%

Equity/ First Loss Tranche – C

Unrated

10%

100%

10%

12.5%

As may be noticed, both the senior and mezzanine are fairly highly rated as the junior most tranche has a considerable amount of thickness and represents a first loss coverage of 10%. Additionally, it also retains 50% of the Mezzanine tranche. Therefore, effectively, the Originator retains 12.5% of the total pool, yet it will qualify for the capital relief, by virtue of holding upto 50% of the Mezzanine tranche, despite retaining 10% in the form of first loss support.

The second clause contemplates a situation where there are only two tranches – that is, the senior tranche and the equity tranche. The clause says that in absence of a mezzanine tranche, the retention of first loss by the Originator should not be more than 20% of the total first loss tranche.

Given the current market conditions, it will be practically impossible to find an investor for the first loss tranche, hence, the entire amount will have to be retained by the Originator. Also, it is very common to provide over-collateral or cash collateral as first loss supports in case of securitisation transactions, even in such cases a third party’s participation in the first loss piece is technically impossible.

Also, there is a clear conflict between this condition and para 16 of the draft Directions, which gives an impression that the first loss tranche has to be retained by the originator itself, in the form of minimum risk retention.

Therefore, in Indian context, if one were to take a holistic view on the conditions, they are two different extremes. While, in the first case, capital relief is achievable, but in the second case, the availing capital relief is practically impossible. This will make the second condition almost redundant.

In order to understand the rationale behind these conditions, please refer to the discussion on EU Guidelines on SRT below.

Impact on the existing transactions

As noted earlier, this part of the draft Directions shall be applicable on the existing transactions as well. Here it is important to note that currently, most of the transaction structures in India either have only one or two tranches of securities, and only a fraction would have a mezzanine tranche. In all such cases, the entire first loss support comes from the Originator. Therefore, almost none of the transactions will qualify for the capital relief.

In the hindsight, the originators have committed a crime which they were not even aware of, and will now have to pay a price.

The moment, the Directions are finalised, the loans will have to be risk-weighted and capital will have to be provided for.

This will have a considerable impact on the regulatory capital, especially for the NBFCs, which are required to maintain a capital of 15%, instead of 9% for banks.

Thickness of the first loss support:

This requirement states that the minimum first loss tranche should be the product of (a) exposure (b) weighted maturity in years and (c) the average slippage ratio over the last one year.

The slippage ratio is a term often used by banks in India to mean the ratio of standard assets slipping to substandard category. So, if, say 2% of the performing loans in the past 1 year have slipped into NPA category, and the weighted average life of the loans in the pool is, say, 2.5 years (say, based on average maturity of loans to be 5 years), the minimum first loss tranche should be [2% * 2.5%] = 5% of the pool value.

In India, currently the thickness of the first loss support depends on the recommendations of the credit rating agencies (CRAs). Typically, the thresholds prescribed by the CRAs are thick enough, and we don’t foresee any challenge to be faced by the financial institutions with respect to compliance with this point.

EU’s Guidelines on Significant Risk Transfer

The guidelines for evidencing significant risk transfer, as provided in the draft Guidelines, are inspired from the EU’s Guidelines on Significant Risk Transfer. The EU Guidelines emphasizes on significant risk transfer for capital relief and states that a high level, the capital relief to the originator, post securitisation, should commensurate the extent of risk transferred by it in the transaction. One such way of examining whether the risk weights assigned to the retained portions commensurate with the risk transferred or not is by comparing it with the risk weights it would have provided to the exposure, had it acquired the same from a third party.

Where the Regulatory Authority is convinced that the risk weights assigned to the retained interests do not commensurate with the extent of risk transferred, it can deny the capital relief to the originator.

Under three circumstances, a transaction is deemed to have achieved SRT and they are:

Where there is a mezzanine tranche involved in the structure: the originator does not retain more than 50% of the risk weighted exposure amounts of mezzanine securitisation positions, where these are:

positions to which a risk weight lower than 1,250% applies; and

more junior than the most senior position in the securitisation and more junior than any position in the securitisation rated Credit Quality Step 1 or 2.

Where there is no mezzanine tranche involved in the structure: the originator does not hold more than 20% of the exposure values of securitisation positions that are subject to a deduction or 1,250% risk weight and where the originator can demonstrate that the exposure value of such securitisation positions exceeds a reasoned estimate of the expected loss on the securitised exposures by a substantial margin.

The competent authority may grant permission to an originator to make its own assessment if it is satisfied that the originator can meet certain requirements.

In case, the originator wishes to achieve SRT with the help of 1 & 2, the same has to be notified to the regulator. If as per the regulator, the risk weights assigned by the originator does not commensurate with the risks transferred, the firms will not be able to avail the reduced risk weights.

Mezzanine test: This is applicable where the transaction has a mezzanine tranche. Usually the first loss tranches are meant to cover up the expected losses in a pool and the mezzanine tranches are meant for covering up the unexpected losses, irrespective of whether the equity/ first loss tranche is retained by the originator or sold off to a third party. The mezzanine test is indifferent with regard to the retention or transfer to third parties of securitisation positions mainly or exclusively covering the EL — given potential losses on these tranches are already completely anticipated through the CET1 deduction/application of 1250% risk weight if they are retained.

First loss test: This is applicable where the transaction does not have a mezzanine tranche. In such a situation, the first loss tranche is expected to cover up the entire expected and unexpected losses. This is clear from the language of the EU SRT guidelines which states, that the securitisation exposure in the first loss tranche must be substantially higher than the expected losses on the securitisation exposure. In this case, due to the pari passu allocation of the actual losses to holders of the securitisation positions that are subject to CET1 deduction/1250% risk weight (irrespective of whether these losses relate to the EL or UL), the first loss test may effectively require the originator to transfer also parts of the EL, depending on the specific structure of the transaction and, in particular, on which portion of the UL is actually covered by the positions subject to CET1 deduction/1250% risk weight

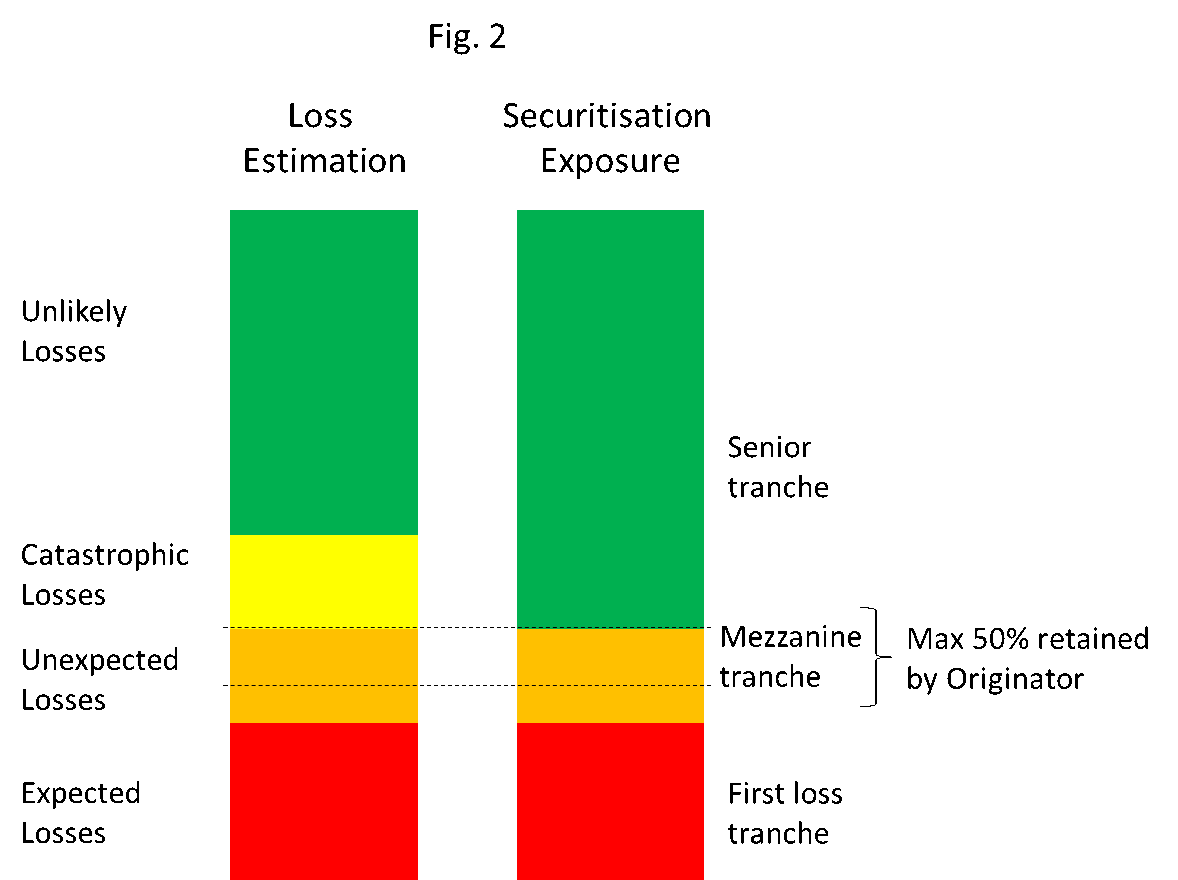

The following graphics will illustrate the conditions better:

In figure 1, the mezzanine tranche is thick enough to cover the entire unexpected losses. If in the present case, 50% of the total unexpected losses are transferred to a third party, then the transaction shall qualify for capital relief.

Unlike in case of figure 1, in figure 2, the mezzanine tranche does not capture the entire unexpected losses. The thickness of the tranche is much less than what it should have been, and the remaining amount of unexpected losses have been included in the first loss tranche itself.

In the present case, even if the mezzanine tranche does not commensurate with the unexpected losses, the transaction will still qualify for capital relief, because, if the first loss tranche is retained by the originator, it will have to be either deducted from CET1/ assign risk weights of 1250%

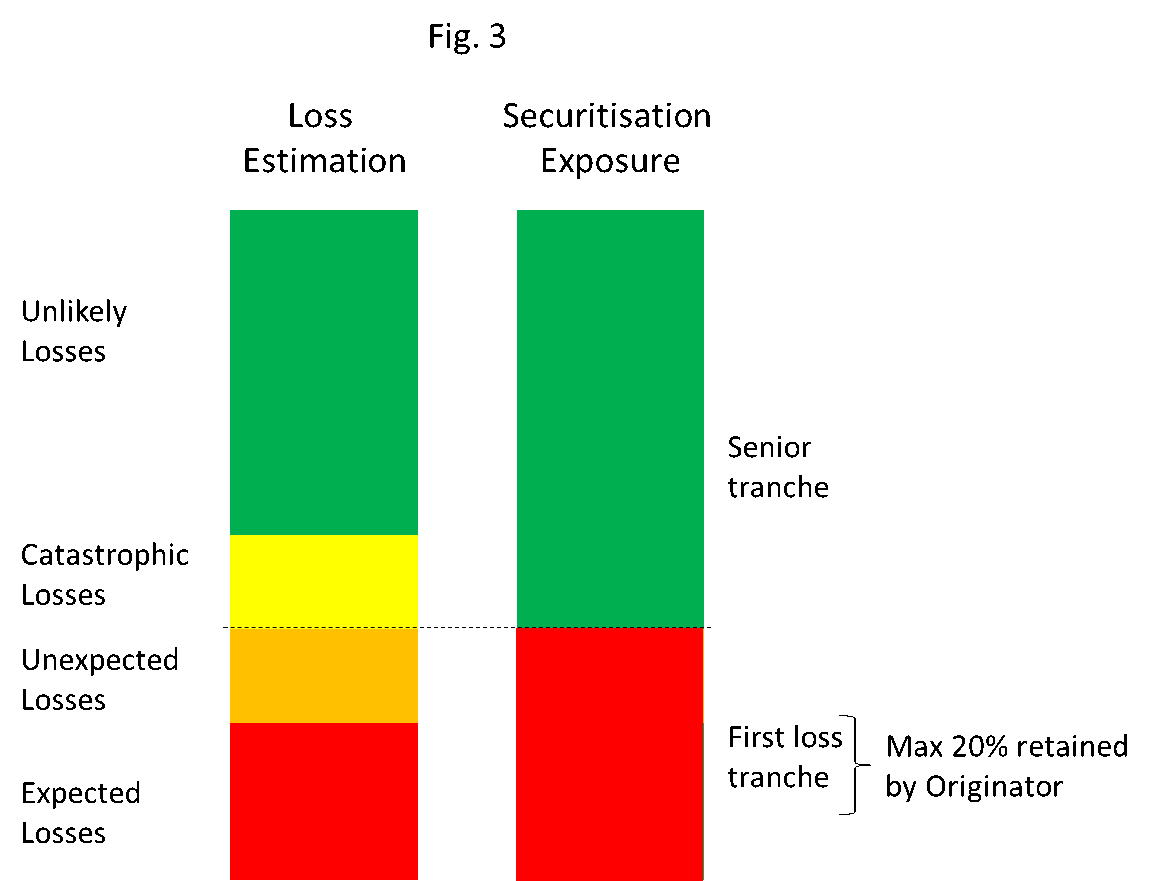

In figure 3, there is no mezzanine tranche. In the present case, the first loss tranche covers the entire expected as well as the unexpected losses. In order to demonstrate a significant risk transfer, the originator can retain a maximum of 20% of the securitisation exposure.

Conclusion

Currently, the draft Directions do not provide any logic behind the conditions it inserted for the purpose of capital relief, neither are they as elaborate as the ones under EU Guidelines. Some explicit clarity in this regard in the final Directions will provide the necessary clarity.

Also, with respect the mezzanine test, in the Indian context, the condition should be coupled with a condition that the first loss tranche, when retained by the originator, must attract 1250% risk weights or be deducted from CET 1. Only then, the desired objective of transferring significant risks of unexpected losses, will be achieved.

Further, as pointed out earlier in the note, there is a clear conflict in the conditions laid down in the para 16 and that in the first loss test in para 79, which must be resolved.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Vinod Kothari Consultantshttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngVinod Kothari Consultants2020-06-10 20:11:032020-06-16 18:31:39Inherent inconsistencies in quantitative conditions for capital relief