Indian companies were permitted to raise funds from overseas either pursuant to issue of depository receipts listed overseas or having the non-residents subscribe to issuances made in India or by way of borrowing overseas. As an initiative to provide an avenue to access global capital markets, GoI had announced the decision to ease raising of foreign funds in order to boost foreign investment inflows, unlock growth opportunities and offer flexibility to Indian companies to raise funds. Consequently, an enabling provision for direct listing of prescribed class of securities on permitted stock exchanges in permissible foreign jurisdictions was inserted vide Companies (Amendment) Act, 2020 in Section 23 of Companies Act, 2013 (‘CA, 2013’), that deals with permissible modes of issue of securities, vide notification dated September 28, 2020 and made effective fromOctober 30, 2023. Thereafter, the Ministry of Corporate Affairs (‘MCA’) notifiedCompanies (Listing of equity shares in permissible jurisdictions) Rules, 2024 (‘LEAP Rules’) effective from January 24, 2024. As listing of shares abroad will result in raising funds from persons resident outside India, Ministry of Finance (‘MoF’) notified FEMA (Non-Debt Instruments) Amendment Rules, 2024 amending FEMA (Non-Debt Instruments) Rules, 2019 (‘NDI Rules’) with effect from January 24, 2024. SEBI is also expected to roll out the operational guidelines for listed companies to list their equity shares on permitted stock exchanges.[1]

Additionally, FAQs on direct listing scheme (FAQs) have also been rolled out on January 24, 2024. Further, two of the key recommendations of the working group report on Direct Listing of Listed Indian Companies on IFSC Exchanges submitted in December 2023 was to notify the rules under Section 23 (3) and (4) of CA, 2013 and notify necessary amendments in NDI Rules to permit cross-jurisdiction issuance and trading of equity shares of Indian companies on IFSC exchanges.

Presently, both the LEAP Rules as well as NDI Rules have notified International Financial Services Centre in India (‘Gift City’) as the permissible jurisdiction and India International Exchange and NSE International Exchange as the permissible stock exchange. International Financial Services Centres Authority (‘IFSCA’) had issued the IFSCA (Issuance and Listing of Securities) Regulations, 2021 effective July 19, 2021 (‘IFSC Regulations’) however, in the absence of enabling provision under CA, 2013 and NDI Rules, Indian companies were unable to undertake listing of securities abroad.

In this article we provide an overview of the regulatory regime and deal with the procedural aspect.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Team Corplawhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngTeam Corplaw2024-01-25 19:28:252024-02-14 11:36:05LEAP to listing: India permits direct listing of shares overseas through IFSC

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Team Corplawhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngTeam Corplaw2023-11-20 15:37:412023-11-28 18:55:51Online workshop on Significant Beneficial Owners: For Companies and LLPs

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Team Corplawhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngTeam Corplaw2023-10-30 17:05:022023-11-01 10:34:11Mandatory conversion of share warrants issued under CA 1956 into demat securities - Snippet on MCA Notification

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Team Corplawhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngTeam Corplaw2023-10-30 16:55:082023-11-01 11:04:43FAQs on mandatory demat of securities by private companies

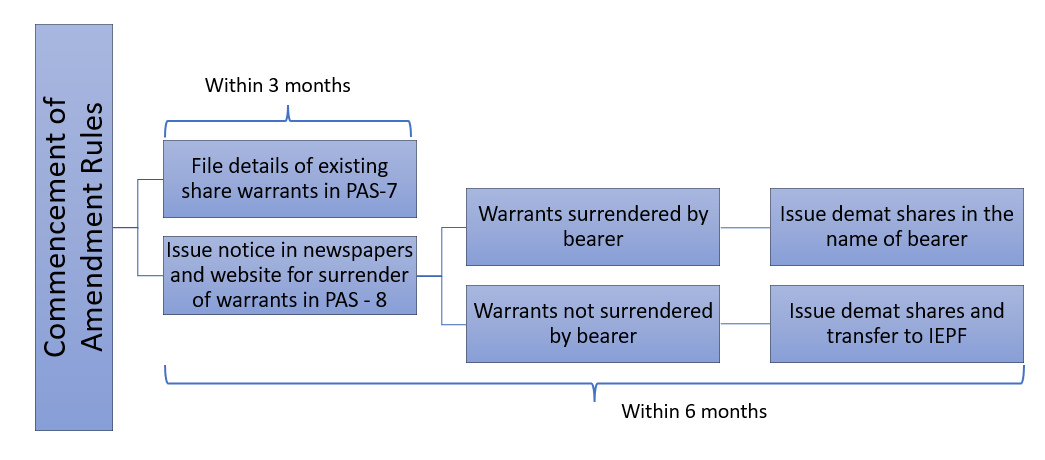

Share warrants are one of the widely used means to raise funds, particularly, in case of start-ups. MCA has recently notified the Companies (Prospectus and Allotment of Securities) Second Amendment Rules, 2023 (“Amendment Rules”) vide which Rule 9 has been amended to require mandatory conversion of the existing share warrants issued by public companies under the erstwhile Companies Act, 1956 (“Erstwhile Act”) into dematerialised form of securities.

Following this amendment, a significant question comes up to be addressed is whether public companies will not be allowed to issue share warrants altogether? We attempt to decode the implications of the present amendment in this write up.

Actionables under the present amendment

The newly inserted sub-rule (2) and (3) to Rule 9 of the PAS Rules requires every unlisted company to –

File the details of existing share warrants with the ROC in form PAS-7 within 3 months from the commencement of the Amendment Rules, i.e., by 27th January 2024,

Require bearers of the share warrants to surrender the same and issue dematerialised shares in the name of such bearer within 6 months from the commencement of the Amendment Rules, i.e., by 27th April, 2024, and

Convert the unsurrendered share warrants into demat shares and transfer the same to IEPF

The company shall be required to issue notice for the bearers of share warrants in form PAS-8 on its website as well as two newspapers – in vernacular language, having wide circulation in the district and in English language having wide circulation in the state in which the registered office of the company is situated.

Share warrants covered under the present amendment

In the context of the newly inserted sub-rule (2) of Rule 9, the term share warrants is to be interpreted in a much restricted sense. The provision refers to “share warrants prior to commencement of the Companies Act, 2013 and not converted into shares”, which implies share warrants issued under the Erstwhile Act only. In this regard, one may refer to section 114 of the Erstwhile Act that allowed public companies to issue “bearer warrants” entitling the bearer of such warrants to the shares specified therein. The same was referred to as “share warrants” under the said Act, and the shares contained therein can be transferred through mere delivery of the warrant.

The present amendment requires mandatory surrender of such “share warrants” in the form of “bearer warrants” against issuance of shares in dematerialised form.

Permissibility for issuance of share warrants under the Companies Act, 2013 (“Act”)?

As mentioned above, the “share warrants” referred to under the Amendment Rules are limited to the bearer warrants issued in accordance with the Erstwhile Act, and do not extend to all share warrants which companies issue under the various provisions of law.

In general context, share warrants are actually written options to subscribe to the shares of a company on pre-agreed terms at a future date. Such warrants are fairly common in the corporate world on account of the benefits associated with the same, and the present amendment cannot be said to rule out the possibility of issuance of such share warrants. Share warrants are directly or indirectly recognised under various provisions of law, for instance:

The definition of “securities” as provided for in section 2(h) of the Securities Contracts (Regulation) Act also includes “rights or interest in securities”. Share warrants are, in fact, a right to acquire securities at a future date, and therefore, well covered under the definition of securities

The SEBI (Issue of Capital and Disclosure Requirements) Regulations, 2018 contains specific provisions with respect to issuance of share warrants.

The Foreign Exchange Management (Non Debt Instruments) Rules, 2019 also refers to the term “share warrants” within the overall definition of “equity instruments” and contains specific provisions with respect to the same.

The Act refers to the conversion of “warrants” as a permissible mode for issuance of shares during the restricted period post buyback u/s 68(8) of the Act. It also contains references to employee “stock options”, which, by nature are equivalent to share warrants.

While the Act does not mention at several places under it about share warrants, however, at few places, like the provisions under section 68 dealing with buy back of securities as well as reference to employee “stock options”, which, by nature are equivalent to share warrants are given the Act.

Therefore, there are no explicit provisions that prohibit the issuance of share warrants by unlisted companies, and the same, being a “security” can very well be issued by a company, whether listed or unlisted, in compliance with the applicable provisions of law to meet the required funding as well as investment objectives.

Concluding remarks

The Amendment Rules aim at the wiping out of the bearer share warrants, since the legal and beneficial ownership of the shares are non-traceable in such a case. However, that does not eliminate the concept of share warrants as a whole, that are issued to an identified set of persons, and follows a due procedure laid down in the law for transfer of such warrants. Although not expressly defined under the Act, the concept of share warrants is legally recognised under various laws and are being widely issued by Indian companies, whether listed or unlisted, including private companies. The current set of amendments will have no impact on the permissibility of issuing share warrants issued under the Act and other laws as mentioned hereinabove.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Team Corplawhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngTeam Corplaw2023-10-28 23:55:412023-11-09 12:26:45Share warrants under cloud - are companies not allowed to issue share warrants?

The concept of “beneficial owner” or BO is well-established under the Companies Act, 2013 by way of section 89 and 90 read with the rules made thereunder. The primary onus of declaration of beneficial interest lies on the person holding such beneficial interest. For the purpose of assigning responsibility to one or more person with respect to the compliance with the said provisions, Rule 9 of the Companies (Management and Administration) Rules, 2014 (“MGT Rules”) has been amended vide the Companies (Management and Administration) (Second Amendment) Rules, 2023 introducing the concept of “designated person” for the purpose of the said section. The amendment has been notified and made applicable from the date of its publication in the official gazette, i.e, 27th October, 2023.

Functions of a designated person

The concept of “designated person” has been brought in vide sub-rule (4) of Rule 9 of the MGT Rules. It requires “every company” to designate a person to be responsible for “furnishing, and extending co-operation for providing, information to the Registrar or any other authorised officer with respect to beneficial interest in shares of the company.” Therefore, a person, identified as a designated person under this rule, would be expected to be aware of, and therefore, take all reasonable steps to become aware, of the person holding “beneficial interest” in the shares of the company.

The applicability of the requirement to identify a designated person is not limited only to such companies that have received declarations with respect to “beneficial interest”, but extends to every company. It is upon the ROC/ other authorities to seek information with respect to beneficial interest from any company, and any such information, as and when sought, will be required to be provided by the designated person identified under this rule.

Who can be a designated person?

Sub-rule (5) of Rule 9 deals with the person qualified to be a designated person. It requires one of the following to act as a “designated person”:

CS of the company, if the company is required to appoint a CS (as per section 203 of the Act), or

any KMP of the company (as defined u/s 2(51) of the Act), or

every director of the company, in case the company does not have a CS or other KMPs.

Therefore, a company may, acting through its board of directors, preferably through a duly passed board resolution in this regard, designate the CS, or any of the KMPs or directors of the company to act as a designated person. The use of the term “every director” does not imply that all directors shall be identified as “designated person”, rather, it would mean that either of the directors can be designated under the aforesaid rule.

“Deemed” designated person

The provisions are applicable immediately, and therefore, till the time a company designates a person for compliance with the aforesaid, the following persons shall be deemed to be designated person:

CS of the company, if the company is required to appoint a CS (as per section 203 of the Act)

In case a CS has not been appointed, every Managing Director or Manager of the company,

In the absence of both (a) and (b), every director of the company.

Disclosure of details of a designated person

The details of the designated person are required to be disclosed in the annual return. The annual return is an e-form filed with ROC, and the present change would require a modification in the existing format so as to facilitate the provision of such information. Further, since the provisions are applicable from 27th October, 2023, the disclosure should be applicable for the annual return filed for FY 23-24 and onwards.

Any changes in the designated person is also required to be intimated to the ROC in e-form GNL-2. No timeline has been specified for filing the same, but should be filed within a reasonable period of time.

The introduction of the concept of “designated person” with respect to the “beneficial interest” in the shares of a company, will have the impact of assigning responsibility and accountability on the designated person with respect to compliance with the provisions of the Act relating to beneficial interest. Recently, many companies have received advisories from the ministry to ensure compliance with the provisions of declaration of beneficial ownership, and the present amendment would act as a “single point assistance” to the authorities in their inspection of companies with respect to compliance with declaration of “beneficial interest”.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Payal Agarwalhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngPayal Agarwal2023-10-28 18:19:162023-11-01 10:45:08Designated to reveal beneficiary identity: all companies mandated to name one

Two major amendments have been notified by MCA on 27th October, 2023 impacting all companies, and majorly the private companies. These include the Companies (Management and Administration) (Second Amendment) Rules, 2023 introducing the concept of “designated person” with respect to beneficial interest in shares of a company[1] and the Companies (Prospectus and Allotment of Securities) Second Amendment Rules, 2023 (“PAS Amendment Rules”). The PAS Amendment Rules encompass two major amendments: (i) with respect to the bearer share warrants under the erstwhile Companies Act, 1956, and (ii) mandatory dematerialisation for all private companies excluding small companies. In this write-up, we briefly discuss the amendments with respect to mandatory dematerialisation of securities for the private companies and the implications thereto.

Regulatory basis of present amendment

Sub-section (1A) was inserted under Section 29 of the Companies Act 2013 (“the Act”) facilitating the Central Government to prescribe such class or classes of unlisted companies for which the securities shall be held and/ or transferred in dematerialised form only. In exercise of the powers conferred under the said section, Rule 9B has been inserted vide the PAS Amendment Rules specifying the requirement of mandatory dematerialisation of securities issued by private companies.

Applicability of mandatory dematerialisation on private companies

The mandatory dematerialisation requirement is applicable on all securities of every private company, excluding small companies[2] and government companies. The provisions are applicable with immediate effect, and a timeline of 18 months is provided from the closure of the financial year in which a private company is not a small company for the compliance with the mandatory dematerialisation requirements.

For example, a private company (other than a company that is a small company as on 31st March, 2023) is required to comply with mandatory dematerialisation of securities within a period of 18 months from the end of FY 22-23, i.e., on or before 30th September 2024.

In case a company ceases to be a small company after 31st March, 2023, the timeline of 18 months triggers from the close of the financial year in which it ceases to be a small company. Therefore, if a company ceases to be a small company at any time during FY 23-24, the timeline of 18 months will trigger from 31st March, 2024 and therefore, shall be complied with by 30th September 2025.

Applicability on a wholly-owned subsidiary

Rule 9B of the PAS Rules, enforcing mandatory dematerialisation of the securities of private companies, is applicable on all private companies other than the following:

Small company, and

Government company

In case of unlisted public companies, sub-rule (11) of Rule 9A extends a similar exemption from dematerialisation requirements. The said sub-rule covers the following public companies –

Nidhi company,

Government company, and

A wholly owned subsidiary.

It is important to note that a wholly owned subsidiary, though exempt from the dematerialisation requirements under Rule 9A, similar exemption does not extend to a private company under Rule 9B. Therefore, currently it seems that a wholly-owned subsidiary, incorporated in the form of a private company, is not exempt from dematerialisation requirements.

Further, for a private company that is a wholly-owned subsidiary of a public company, and therefore, a deemed public company, it remains an open question as to whether it will be exempt under sub-rule (11) of Rule 9A or the provisions of Rule 9B will apply.

The position may be summarised as below –

Nature of wholly-owned subsidiary

Nature of holding company

Applicability of dematerialisation provisions

Public company

Public company

Exempt under Rule 9A(11)

Public company

Private company

Exempt under Rule 9A(11)

Private company

Private company

Covered under Rule 9B as of now

Private company

Public company

The same being a deemed public company, there is no clarity on whether Rule 9A applies or Rule 9B. If considered to be a private company – covered under Rule 9B If considered to be a public company – exempt in terms of Rule 9A(11)

Compliances applicable to private companies

A private company, covered under the provisions of mandatory dematerialisation shall –

Issue all securities in dematerialised form only;

Facilitate dematerialisation of all existing securities (as and when request is received from the holder of such securities);

Ensure that the entire holding of its promoters, directors and KMPs are held in dematerialised form only, prior to making any offer for issuance or buyback of securities

Apart from the aforesaid, the compliances applicable to an unlisted public company under sub-rule (4) to (10) of Rule 9A are also applicable to private companies. These include –

Application with depository for dematerialisation of all existing securities and securing ISIN for each type of security;

Inform the existing security holders about the facility of dematerialisation;

Make timely payment and maintenance of security deposit with the depository, RTA and STA as may be agreed between the parties;

Complies with all applicable regulations, directions and guidelines with respect to dematerialisation of securities of a private company;

File a return in form PAS-6 with ROC on a half yearly basis within 60 days from conclusion of each half of the financial year, with respect to reconciliation of the share capital of the company;

Bring to the notice of the depositories, any difference in the issued capital by the company and the capital held in dematerialised form;

The grievances of any security holders under this rule (Rule 9B) to be filed with IEPF Authority, and the same, in turn, shall initiate any action against a depository or depository participant or RTA or STA, as may be required, after prior consultation with SEBI.

Compliances applicable to the holders of securities of a private company

As for persons holding securities of a private company, while the mandatory dematerialisation cannot be enforced by the private company, the same is expected to be taken care of by way of sub-rule (4) of Rule 9B that requires –

Dematerialisation of securities by the securityholder, before the transfer of such securities; and

Subscription to the securities issued by a private company, in dematerialised form only

Therefore, the mandatory dematerialisation of securities of a private company is ensured through placing restrictions on both a private company and the holders of securities issued by the same.

Consequences of non-compliance

There are no specific penal provisions governing the non-compliance with the provisions of section 29 of the Act read with Rule 9B of the PAS Rules, and therefore, general penal provisions under section 450 of the Act should apply.

Section 450 specifies the following: “If a company or any officer of a company or any other person contravenes any of the provisions of this Act or the rules made thereunder, or any condition, limitation or restriction subject to which any approval, sanction, consent, confirmation, recognition, direction or exemption in relation to any matter has been accorded, given or granted, and for which no penalty or punishment is provided elsewhere in this Act, the company and every officer of the company who is in default or such other person shall be liable to a penalty of ten thousand rupees, and in case of continuing contravention, with a further penalty of one thousand rupees for each day after the first during which the contravention continues, subject to a maximum of two lakh rupees in case of a company and fifty thousand rupees in case of an officer who is in default or any other person.”

Implications of the present amendment

The existence of shell companies and personification of shareholders is not a rare scenario, and such a situation is likely to be more common in case of a private company, unlike a public company. Historically, dematerialisation of shares is looked upon by the government as a means to curb black money[3]. As for listed companies and unlisted public companies[4], the dematerialisation of securities is already a mandatory requirement. With the present amendments being notified, the private companies have also been covered by the mandatory dematerialisation requirements.

As on 31st January, 2023, more than 14 lac companies registered with MCA comprising 95% of the total active companies are private companies, out of which approximately 50,000 companies are small companies[5]. Thus, with the mandatory dematerialisation for private companies coming into existence, a large number of companies will be forced to move towards dematerialisation of shares. Further, while the company can be held accountable for the mandatory dematerialisation of securities held by promoters, directors and KMPs, given the closely held nature of private companies, barely any securityholder (particularly shareholders) will remain outside the purview of the same.

Further, it is clarified that, in no way such a mandatory dematerialisation for private companies can be taken to mean that the restriction on transfer of shares of such a company is relaxed, and adequate systems can be implemented at the depository’s level to ensure compliance with the basic distinguishing characteristic of a private company and thereby have filters before executing any transfer of securities.

[2] As per the definition under the Act read with the rules made thereunder, a small company means a company, other than a public company, having paid up share capital not exceeding Rs. 4 crores and turnover not exceeding Rs. 40 crores. Further, the following cannot be a small company –

(A) a holding company or a subsidiary company;

(B) a company registered under section 8; or

(C) a company or body corporate governed by any special Act.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Payal Agarwalhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngPayal Agarwal2023-10-28 17:03:082023-11-01 11:02:47Diktat of demat for private companies

If the intent of CSR provisions coded in the law was to promote socially responsible conduct on the part of companies, that lesson of responsibility is being taught the very hard, indiscriminately harsh way – by imposing penalties of 2X of the amount involved in CSR breaches, even if the breach was a pure timing mismatch. By now, there are several such adjudication orders – purely as an example, is where the order clearly notes that there has been no failure on the part of the company to spend the failed amount of Rs 14.50 lacs. The amount was indeed spent, as intended for “ongoing projects”, but there mere segregation of this money into a separate bank account, required to be done within 30 days, was missing. Applying the provisions of sec. 135 (7) which provides for a “penalty of twice the amount” which failed the segregation requirement, though it did not fail the spending requirement.

There are several points that arise here: segregation of the amounts meant to be spent for ongoing projects is merely a ring-fencing requirement, such that companies are aware of the purpose for parking the money, and such money is indeed not commingled with the company’s own funds. If the funds are indeed spent for the purpose for which they are to be segregated, the failure to segregate is, at the most, the failure of the method and not the ultimate result. The failure was transient, and only a timing issue, and not a substantive failure. Therefore, even if punishable, the punishment could not have been the maximum amount provided by the law.

The article was also published by IndiaCorpLaw and can be viewed here

Disposal of an undertaking (whole or substantially the whole) can be done either as part of a scheme of arrangement or otherwise by way of slump sale / business transfer agreement (‘BTA’). Disposal, other than by way of scheme of arrangement, have so far been regulated as per section 180(1)(a) of the Companies Act, 2013 (‘Act’) which requires approval of the shareholders by way of special resolution. SEBI has prescribed approval requirement in this regard by way of introduction of regulation 37A vide SEBI (Listing Obligations and Disclosure Requirements) (Second Amendment) Regulations, 2023 (‘Amendment Regulations’) effective from June 14, 2023 that requires listed entities to follow a stricter regime for disposal of undertaking inter alia mandating approval from majority of the public shareholders who are not interested in the transaction, disclosure of the object, commercial rationale and use of proceeds arising from such transaction. While there is an exemption provided in case of transactions with a wholly owned subsidiary (WOS), the approval regime will apply in case of disposal of undertaking by such WOS or any reduction in shareholding in the WOS subsequent to transfer of the undertaking.

The said amendment is based on the Consultation Paper rolled by SEBI on February 21, 2023. Apart from incorporating the provisions proposed in this regard in the Consultation Paper, the amendment has introduced new provisions as well. Provision with respect to seeking approval from the shareholders of the listed entity in case a WOS is used as a conduit for transfer in undertaking is a new requirement brought in through the amendment.

https://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.png00Nitu Poddarhttps://vinodkothari.com/wp-content/uploads/2023/06/vinod-kothari-logo.pngNitu Poddar2023-06-16 17:21:532023-06-21 11:35:52Stricter framework for sale, lease or disposal of undertaking by a listed entity