Torrid time for NBFCs as FIU-IND lays down ‘High Risk’ classification

– By Saloni Mathur (finserv@vinodkothari.com)

Introduction

Just when the NBFCs were grappling with the outburst of RBI’s Ombudsman Scheme which was proposed to come into effect from 23rd February, 2018, FIU-IND released the list of ‘High risk NBFCs’[1] (‘List’) on account of non-compliance with the Prevention of Money Laundering Act, 2002 (‘PMLA Act’)[2] and the Prevention of Money Laundering (Maintenance of Records) Rules, 2005[3] (‘PMLA Rules’).

The Financial Intelligence Unit in the List laid down 9500 high risk NBFC’s that are coming under the ambit of the non-compliance with the PMLA Act and the PMLA Rules in respect of non-registration of the Principal Officer(PO) as on 31.01.2018.

Rationale

The intent of the Financial Intelligence Unit seems quite rational. Post demonetization in 2016 it has been strongly witnessed that several NBFCs were taking advantage of their business models by allegedly converting banned currency notes and accepting cash as deposits, and subsequently violating the provisions of the PMLA Act and the PMLA Rules. In order to curb this malpractice, the FIU has issued a warning to the NBFCs by categorizing them as ‘high risk NBFCs’ on the basis of non-compliance with the PMLA Act and the PMLA Rules with regard to non-appointment of the Principal Officer and the kind of repercussions that these may encounter in the case of any further non-compliance.

Legality emanating the ‘High Risk Classification’

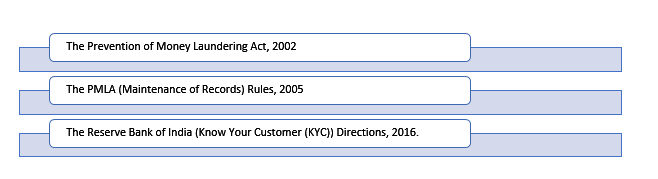

The legality that governs the above high-risk classification of the NBFCs has its roots from the PMLA Act, PMLA Rules and the RBI directions titled, ‘The Reserve Bank of India (Know Your Customer (KYC)) Directions, 2016’ applicable to all the Regulated Entities (RE’s) as defined in 3(b)(xiii) of the said directions[4].

Clause wa of Chapter 1 of the PMLA Act, 2002 defines Reporting entity:

“Reporting entity” means a banking company, financial institution, intermediary or a person carrying on a designated business or profession.”

Clause f of the PMLA (Maintenance of Records) Rules, 2005 defines Principal Officer:

“Principal Officer” means an officer designated by a Reporting Entity.”

Rule 3 of the PMLA( Maintenance of Records) Rules 2005 deal with the maintenance of the records and the transactions of following nature and value:

- “All cash transactions of the value of more than 10 lakhs or its equivalent in the foreign currency

- All series of cash transactions integrally connected to each other which have been individually valued below rupees ten lakh or its equivalent in foreign currency where such series of transactions have taken place within a month and the monthly aggregate exceeds an amount of ten lakh rupees or its equivalent in foreign currency.”

- All transactions involving receipts by non-profit organizations of value more than rupees ten lakh, or its equivalent in foreign currency.

- All cash transactions where forged or counterfeit currency notes or bank notes have been used as genuine or where any forgery of a valuable security or a document has taken place facilitating the transactions;

- All suspicious transactions whether or not made in cash and by way of-

- deposits and credits, withdrawals into or from any accounts in whatsoever name they are referred to in any currency maintained by way of-

- cheques including third party cheques, pay orders, demand drafts, cashier cheques, or any other instrument of payment of money including electronic receipts or credits and electronic payments or debits, or

- travellers cheques, or

- transfer from one account within the same banking company, financial institution and intermediary, as the case maybe including from or to nostro and Vostro accounts, or

- any other mode in whatsoever name it is referred to;

- all cross border wire transfers of the value of more than five lakh rupees or its equivalent in foreign currency where either the origin or destination of fund is in India.

- All purchase and sale by any person of immovable property valued at fifty lakh rupees or more that is registered by the reporting entity, as the case maybe.”

Following table represents various compliances by the reporting entity and their respective principal officers in respect to the above functions under various legal regulations:

| S.no | Act/Rule/Legislation | Governing Regulation/Section | Requirement |

| 1. | The Prevention of Money Laundering(Maintenance of Records) Rules, 2005 | Reg.7 | Every reporting entity shall communicate to the director the name, designation, and address of the designated director and the Principal Officer. |

| 2. | The Prevention of Money Laundering(Maintenance of Records) Rules, 2005 | Reg.8 | The principal officer shall submit all the information pertaining to the transactions to the director as defined in rule 3 above. |

| 3. | The PMLA Act, 2002 | Section 12 (a) and (b) | a)Every reporting entity shall maintain records of all transactions

b)furnish to the director any such information within such time as may be prescribed. |

| 4. | The PMLA Act, 2002 | Chapter IV Section 12A | The director may call for any such information as may be required by him within such time and in such manner in which he may specify. |

| 5. | The PMLA Act, 2002 | Chapter IV Section 13(2) | The director may, either of his own motion or an application made by the authority, officer or person with regard to the obligations of the reporting entity.

Any failure to comply with the provisions of this chapter would result in laying down some standing instructions and monetary penalty. |

| 6. | The Reserve Bank of India (Know Your Customer (KYC)) Directions, 2016 | Chapter II Reg.7(i) and (ii) | Principal officer shall be responsible for ensuring compliance, monitoring transactions, and sharing and reporting information as required under the laws/regulations |

Impact of such release on NBFCs

The publication of names is primarily a step by the FIU to make the public aware that these NBFCs are not law compliant and they should refrain from indulging into transactions with them. Through this release NBFCs are being urged to comply with this ‘basic obligation’ of appointing a principal officer who would oversee the compliances under the PMLA Act and the PMLA rules.

The Financial Intelligence Unit has come out with this list with an intent to warn the NBFCs in case of non-compliance with the PMLA Act, 2002 and the PMLA Rules, 2005. Further failure to comply with the provisions of the PMLA Act, 2002 and the PMLA Rules, 2005 specifically non-registration of the Principal officer would require stringent penal proceedings against the NBFC as specified in Section 13(2) of the PMLA Act, 2002.

Section 13(2) of the PMLA Act, 2005 prescribes certain standing instructions and monetary penalty for all applicable entities. These are as follows:

Standing instructions that might be imposed by the FIU

- Director may issue a warning in writing.

- Direct such reporting entity or its designated director on the board or any of its employees, to comply with the specific instructions

- Direct reporting entity to send reports at regular intervals as may be prescribed

Monetary Penalty that might be imposed by the FIU

- Penalty shall not be less than ten thousand rupees but may exceed to one lakh rupees for each failure.

The intent of this circular does not seem so stringent in nature presently. NBFCs who have not appointed Principal officer as on date are required to appoint them in order to remove the name from this list. This warning is issued in the nature of a standing instruction, which soon has to be complied by all the NBFCs who are not complying with the provisions of the Act.

Quick Actionable by the NBFCs

- Appoint Principal Officer

- Ensure communication of name, designation and address of the Principal Officer to the director, FIU-IND

- Ensure that the Principal Officer reports all transactions under rule 3 of the PMLA( Maintenance of Records) Rules, 2005 to the director, FIU-IND.

Conclusion

Generation of the above list can be viewed as a measure by the Financial Intelligence Unit a standing instruction to all the NBFC’s to comply with provisions of the PMLA Act, 2002 and the respective Rules regarding the appointment of the Principal Officer

This standing instruction may turn into severe stringent penalty in case of further non-compliance. Thus if the principal officer is failed to get appointed until now, NBFCs can ensure their appointment now in order to escape any further penalties that may arise in this regard.

[1] http://fiuindia.gov.in/pdfs/quicklinks/High%20Risk%20NBFCs%20as%20on%2031.01.2018.pdf

[2] http://lawmin.nic.in/ld/P-ACT/2003/The%20Prevention%20of%20Money-laudering%20Act,%202002.pdf

[3] http://www.enforcementdirectorate.gov.in/pmla_rules.pdf

[4] https://rbidocs.rbi.org.in/rdocs/notification/PDFs/18MDKYCD8E68EB13629A4A82BE8E06E606C57E57.PDF