Investment by FPIs in securitised debt instruments

By Anita Baid,(anita@vinodkothari.com)(finserv@vinodkothari.com)

Investments by Foreign Portfolio Investors (FPIs) in unlisted debentures and securitised debt instruments (SDIs) issued by Indian companies was allowed pursuant to SEBI notification dated 27th February, 2017[1]. Earlier in November, 2016, Reserve Bank of India (RBI) had also permitted investment by FPIs in unlisted non-convertible debentures and securitised debt instruments issued by Indian companies[2]. The said amendments by the securities market regulator and financial services regulator were the final push which was needed to encourage more FPI investments in India.

Previously, FPIs could invest only in debt securities of companies engaged in the infrastructure sector. This was a clear indication that the government aimed to develop the infrastructure sector in India. But eventually, it seemed that the government did not want to restrict this to infrastructure only and wanted to reap all the benefits for developing a dynamic and facilitating bond market in the country.

Economic development and smooth flow of funds into the economy are the twin sides of the same coin and the government of India has very well taken this into account while amending the FPI regulation. Allowing FPI investments in unlisted debt instruments of Indian companies, was a step by the government to relax the burden which the companies had to bear, while raising funds in the form of equity. The regulation in turn blocked the companies from tapping into fresh funds and listing of debt instruments, which called for additional burden of complying with a host of other regulations.

Indian Valuation Standards: Standardizing the rules of valuation in India

Refer to valuation approaches here- http://vinodkothari.com/2020/09/valuation-approaches-and-methods/

MCA raises curtain on SBO Rules – Notifies final rules with several changes.

CS Vinita Nair, vinita@vinodkothari.com

CS Nikita Snehil, nikita@vinodkothari.com

Vinod Kothari & Co. | June 14, 2018

Amendment to Section 89 and 90 is one of the key amendments proposed in Companies (Amendment) Act, 2017 (Amendment Act). While, the Amendment Act is being enforced in phases, stakeholders were given the option to provide the public comments on the draft rules[1] in relation to Significant Beneficial Ownership (SBO), which was issued by MCA on Feb 2, 2018. Thereafter, on June 6, 2018, MCA vide its Notification, has enforced the provisions of amended Section 90 of the Companies Act, 2013 and also issued the Companies (Beneficial Interest and Significant Beneficial Interest) Rules, 2018[2] (‘Final Rules’) in relation to SBO. This is one of the most onerous provision rolled out by MCA. The purpose of this Section is to ask companies ‘Parde ke peeche kaun hai? Saamne aao!’. The present Article explains the provisions of the amended Section 90 and the Final Rules. Read more →

MCA amends MGT Rules- alignment with Companies (Amendment) Act, 2017

By Megha Saraf (megha@vinodkothari.com),(corplaw@vinodkothari.com)

Introduction

Subsequent to the Ministry of Corporate Affairs (“MCA”) notifications dated 9th February, 2018 and 7th May, 2018 through which MCA hadenforced 43 sections and 28 sections of the Companies (Amendment) Act 2017, (“Act, 2017”),it has once again come up with another set of notificationsvide its notification dated 14th May, 2018 bringing 5more sections of Act, 2017 to life and amending corresponding Rules that are prescribed. Read more →

Transitory liberalisation of asset classification norms for MSMEs

by Yutika Lohia and Anita Baid (finserv@vinodkothari.com)

With the advent of GST in the Indian economy, all three sectors i.e. Agriculture, Industry and Service, have been facing several challenges. Majority of small entities in the country have been impacted in some way or the other, irrespective of whether they required registration under GST or not. MSMEs requiring registration faced difficulties due to disruption of their business for ensuring compliance with the new regime. Even unregistered MSMEs faced complications as they were dealing with businesses which were directly disrupted due to GST implementation eventually effecting their cash flows to honour financial obligations. In response to the worries of small enterprise, the government has introduced several relaxation so as to enable them to adopt themselves with the revolutionary change of indirect taxation scheme being implemented in the country. Certainly the cash flows of the micro, small, medium enterprises (MSMEs) sector has been adversely affected with this new GST regime and such entities whether registered or not under GST, who have taken financial assistance are definitely facing problems to pay off their debts. Read more →

Fair Market Value – as per Company Law perspective

By Nikita Snehil | nikita@vinodkothari.com

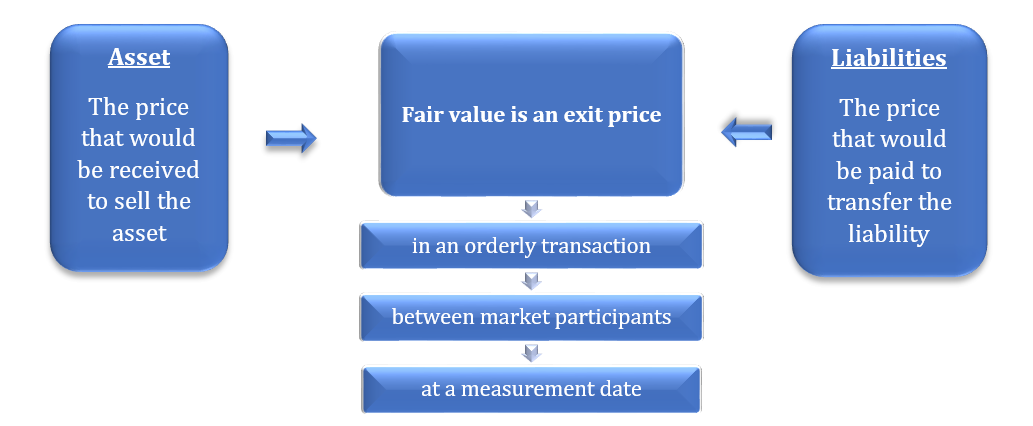

The term ‘Fair market value’ has been used hundreds of times in the Income Tax Act, 1961, however, the same has also been given due weightage under the Companies Act, 2013. The present Article intends to explain the meaning of the term ‘Fair Market Value’, its significance and its relevance as per Companies Act, 2013.

Meaning of Fair Market Value

In general parlance, Fair market value is the price agreed between a buyer and a seller for a specific asset. Both parties should be aware of the asset’s condition and willing to participate in the transaction with no force or conditions.

However, the term has been defined in para 9 the Ind AS 113[1], which states the following:

“Ind AS defines fair value as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date.”

Therefore, the definition can be illustrated in the following way:

The concept of Fair Market Value has become all pervasive particularly after the introduction of International Financial Reporting Standards because there is greater stress on fair value today than in the past.

Provisions of the Companies Act, 2013 referring to fair valuation

The provisions of the Companies Act, 2013 (‘Act’) talks about the requirement of valuation in many cases, the following table shows the sections of the Act requiring valuations:

| Section no. | Valuation purpose |

Requirements in brief

|

| 54 | Issuance of Sweat Equity Shares | The sweat equity shares to be issued shall be valued at a price determined by a registered valuer as the fair price giving justification for such valuation.

|

| 62(1) (c) | Preferential Offer | When a company proposes to issue new shares, the price of such shares should be determined by the valuation report of a Registered Valuer.

|

| 192(2) | Non-cash transaction involving directors | Where there is a sale or purchase of any asset involving a company and its directors (or its

holding, subsidiary or associate company) or a person connected with the director for consideration other than cash, the value of the assets has to be calculated by a Registered Valuer.

|

| 230 & 232 | Compromises, Arrangements and Amalgamations | In case of compromise or arrangement between members or with creditors or any class of them, a valuation report in respect of shares, property or assets, tangible and intangible, movable and immovable of the company is required by a Registered Valuer.

|

| 236 | Purchase of minority share holding | Where an acquirer or person acting in concert with the acquirer acquires 90% or more of the equity capital in a company, then they can offer to the minority shareholder or the minority shareholder can offer to the acquirer, to acquire the minority shareholding at a valuation determined by the Registered Valuer.

|

| 281 & 305 | Winding up of a company | In case of winding up, the valuation of assets of the company prepared by the Registered Valuer is required.

|

Who can be valuer?

Though the Act does not specify anything regarding the eligibility of the registered valuers, the Companies (Share Capital and Debenture) Rules, 2014 provides the following:

For the purposes of these rules, it is hereby clarified that, till a registered valuer is appointed in accordance with the provisions of the Act, the valuation report shall be made by an independent merchant banker who is registered with the Securities and Exchange Board of India or an independent Chartered Accountant in practice having a minimum experience of ten years.

Thereafter, MCA had notified the provisions governing valuation by registered valuers [section 247 of the Act and the Companies (Registered Valuers and Valuation) Rules, 2017 (‘Rules’), both to come into effect from 18 October, 2017.

Valuation by Registered Valuers

As per the notified section 247(1), where a valuation is required to be made in respect of any property, stocks, shares, debentures, securities or goodwill or any other assets or net worth of a company or its liabilities under the provision of this Act, it shall be valued by a person having such qualifications and experience and registered as a valuer in such manner, on such terms and conditions as may be prescribed and appointed by the audit committee or in its absence by the Board of Directors of that company.

Proposal of MCA to have registered valuers

The definition of ‘Valuer’ in the said Rules, provides the following:

“valuer” means a person registered with the authority in accordance with these rules and the term “registered valuer” shall be construed accordingly.

Therefore, the valuer will have to obtain the Certificate of Registration after complying the qualification and eligibility criteria as specified in the Rules, in order to do the valuation.

Eligibility of Registered Valuers

As per Rule 3 of the said Rules, the following person shall be eligible to be a registered valuer if he-

- Is a valuer member of a registered valuers organisation;

Explanation.- For the purposes of this clause, “a valuer member” is a member of a registered valuers organisation who possesses the requisite educational qualifications and experience for being registered as a valuer;

- Is recommended by the registered valuers organisation of which he is a valuer member for registration as a valuer;

- Has passed the valuation examination under rule 5 within three years preceding the date of making an application for registration under rule 6

- Possesses the qualifications and experience as specified in rule 4;

- Is not a minor;

- Has not been declared to be of unsound mind;

- Is not an undischarged bankrupt, or has not applied to be adjudicated as a bankrupt;

- Is a person resident in India; .

Explanation.- For the purposes of these rules ‘person resident in India’ shall have the same meaning as defined in clause (v) of section 2 of the Foreign Exchange Management Act, 1999 (42 of 1999) as far as it is applicable to an individual;

- Has not been convicted by any competent court for an offence punishable with imprisonment for a term exceeding six months or for an offence involving moral turpitude, and a period of five years has not elapsed from the date of expiry of the sentence:

Provided that if a person has been convicted of any offence and sentenced in respect thereof to imprisonment for a period of seven years or more, he shall not be eligible to be registered;

- Has not been levied a penalty under section 271J of Income-tax Act, 1961 (43 of 1961) and time limit for filing appeal before Commissioner of Income-tax (Appeals) or Income-tax Appellate Tribunal, as the case may be has expired, or such penalty has been confirmed by Income-tax Appellate Tribunal, and five years have not elapsed after levy of such penalty; and

- Is a fit and proper person:

Further, with respect to a partnership entity or company, the following shall not be eligible to be a registered valuer if-

- It has been set up for objects other than for rendering professional or financial services, including valuation services and that in the case of a company, it is not a subsidiary, joint venture or associate of another company or body corporate;

- It is undergoing an insolvency resolution or is an undischarged bankrupt;

- All the partners or directors, as the case may be, are not ineligible under clauses (c), (d), (e), (g), (h), (i), (j) and (k) as mentioned above;

- Three or all the partners or directors, whichever is lower, of the partnership entity or company, as the case may be, are not registered valuers; or

- None of its partners or directors, as the case may be, is a registered valuer for the asset class, for the valuation of which it seeks to be a registered valuer.

Applicability of the Rules

As per the transitional provisions specified in the Rules read with the MCA’s Notification[1] on extending the transitional period:

“Any person who may be rendering valuation services under the Act, on the date of commencement of these rules, may continue to render valuation services without a certificate of registration under these rules upto 30th September, 2018:

Provided that if a company has appointed any valuer before such date and the valuation or any part of it has not been completed before 30th September, 2018, the valuer shall complete such valuation or such part within three months thereafter.”

Therefore, the persons intending to act as the registered valuers must obtain the Certificate of Registration within September 30, 2018, as per the requirements of the Rules.

Issuance of Valuation Standards by ICAI

Recognising the need to have the consistent, uniform and transparent valuation policies and harmonise the diverse practices in use in India, the Council of the Institute of Chartered Accountants of India at its 375th meeting has issued the Valuation Standards vide the Press Release[2] dated May 25, 2018, mandating the compliance with the Standards for the Chartered Accountants providing valuation reports under various provisions of the Companies Act.

The Standards include the framework for the preparation of valuation report, valuation bases, approaches and methods, scope of work, analyses and evaluations, documentation and reporting, intangible assets and financial instruments, among several other aspects.

Therefore, recognizing the importance of valuation, the Rules introduced by MCA and the standards introduced by ICAI will provide a benchmark to the professionals to ensure uniformity in approach and quality of valuation output.

[1] http://mca.gov.in/Ministry/pdf/INDAS113.pdf

[2] http://www.mca.gov.in/Ministry/pdf/CompaniesRules2018_12022018.pdf

[3] https://www.icai.org/new_post.html?post_id=14799&c_id=238

SEBI proposes to streamline the ICDR Regulations

By Pammy Jaiswal, (pammy@vinodkothari.com) & Nikita Snehil (nikita@vinodkothari.com)

The SEBI had constituted the Issue of Capital & Disclosure Requirements Committee (‘ICDR Committee) under the Chairmanship of Mr. Prithvi Haldea in June, 2017, to review the ICDR Regulations. The ICDR Committee suggested certain policy changes which were taken to the Primary Market Advisory Committee (‘PMAC’) of SEBI which comprises of eminent representatives from the Ministry of Finance, Industry, Market Participants, academicians, the Institute of Chartered Accountants of India and the Institute of Company Secretaries of India. Thereafter, pursuant to the recommendations made by the PMAC, SEBI vide its Press Release dated May 4, 2018[1], has come out with its Consultation Paper on Review of the SEBI (Issue of Capital and Disclosure Requirements) Regulations, 2009, on its website for public comments.

Approach adopted by the ICDR Committee

The Consultation Paper provides that the ICDR Committee while reviewing the Regulations and Schedules, adopted the following approach:

- Simplify language and structure of the regulations to enhance its readability;

- Separate the chapters on the basis of the type of offering so that all relevant information pertaining to the regulations relating to a particular type of offering are available at one place;

- Align the regulations in line with the various informal guidance/ interpretative letters/ frequently asked questions regarding interpretation of various provisions of the regulations, issued by SEBI from time to time;

- Update the regulations with the changes that have taken place in the last few years, including in the Companies Act, 2013, adoption of Indian Accounting Standards, various ICDR related circulars, SEBI (Share Based Employee Benefit) Regulations, 2014, SEBI (Substantial Acquisition of Shares and Takeover) Regulations, 2011, ASBA, abolition of MRTP, etc.;

- To identify policy changes in line with the present market practices and the prevailing regulatory environment.

In this regard, the present article, through the following table, portrays the major changes proposed by SEBI for issuance through rights issue, bonus, preferential allotment and QIPs, the rationale behind such changes and the impact of such proposed changes.

| Chapter | Existing Provision | Proposed changes | Rationale | Remarks |

| Rights Issue | ||||

| Rights Issue – Roll over of non-convertible portion of partly convertible of debt instruments

|

21. (1) The non-convertible portion of partly convertible debt instruments issued by a listed issuer, the value of which exceeds fifty lakh rupees, may be rolled over, without change in the interest rate subject to compliance with the provisions of section 121 of the Companies Act, 1956 and the following conditions: | 64. {21. (1)} The non-convertible portion of partly convertible debt instruments issued by a listed issuer, the value of which exceeds ten crore rupees, may be rolled over, subject to compliance with the provisions of the Companies Act, 2013 and the following conditions: | It is proposed to increase the low threshold of Rs. 50 Lacs to Rs. 10 Crore. | Proposed change will make debt securities with non-convertible portion lesser than Rs. 10 crores to become ineligible for roll-over.

Further, the reference to section 121 of the Companies Act, 1956 has been removed considering that the same is not present under the Act, 2013 and accordingly, the reference to the Act, 2013 has been made. |

| Rights Issue – Issue of warrants | 4. (3) An issuer shall be eligible to issue warrants subject to the following: … (b) not more than one warrant shall be attached to one specified security (c) the price or conversion formula of the warrants shall be determined upfront and at least 25 of the consideration amount shall also be received upfront | 67. {4. (3)} An issuer shall be eligible to issue warrants subject to the following: a) the tenure of such warrants shall not exceed eighteen months from their date of allotment in the rights issue; b) A specified security may have one or more warrants attached to it; c) the price or formula for determination of exercise price of the warrants shall be determined upfront and disclosed in the letter of offer and at least twenty-five per cent. of the consideration amount based on the exercise price shall also be received upfront; Provided that in case the exercise price of warrants is based on a formula, twenty-five per cent. consideration amount calculated as per the formula with reference date being the record date shall also be received upfront. d) in case the warrant holder does not exercise the option to take equity shares against any of the warrants held by the warrant holder, the consideration paid in respect of such warrant shall be forfeited by the issuer. | It is proposed to introduce flexibility of having more than one warrant attached to a specified security and to clarify that the price or formula for determination of exercise price of the warrants shall be determined upfront and that if the warrant is not exercised, 25% of consideration will be forfeited | The proposed change will allow more than one warrant to be attached to a specified security and the same shall enable more flexibility to the warrant holder in terms of conversion decision.

Further, 25% of the consideration based on warrant exercise price as paid shall be forfeited in case of non-exercise of option. |

| Rights Issue – Record Date | 52. (1) A listed issuer making a rights issue shall announce a record date for the purpose of determining the shareholders eligible to apply for specified securities in the proposed rights issue. | 68.(1) {52. (1)} The issuer shall announce a record date for the purpose of determining the shareholders eligible to apply for specified securities in the proposed rights issue at least seven working days prior to the record date or such period as may be specified in the SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015. | It is proposed to make the provision of record date consistent with the SEBI LODR Regulations. | Proposed change is made to align ICDR with Listing Regulations. |

| Rights Issue – Filing of the draft letter of offer and letter of offer | 6. (1) No issuer shall make, (a) a public issue; or (b) a rights issue, where the aggregate value of the specified securities offered is fifty lakh rupees or more, unless a draft offer document, , along with fees as specified in Schedule IV, has been filed with the Board through the lead merchant banker, at least thirty days prior to registering the prospectus, red herring prospectus or shelf prospectus with the Registrar of Companies or filing the letter of offer with the designated stock exchange, as the case may be | 71. (1) {6. (1)} Prior to making a rights issue, the issuer shall, except in case of a fast track issue, file a draft letter of offer, with the concerned regional office of the Board under the jurisdiction of which the registered office of the issuer company is located, in accordance with Schedule IV, along with fees as specified in Schedule III, with the Board and with the stock exchange(s), through the lead manager(s). | It is proposed to clarify that filing of letter of offer with the Board is not required in case of a fast track issue, although the fee will be paid. | The proposed change shall do away with filing of the offer letter with the exchange which seems to a welcome change considering the timeline under fast track issue. |

| Rights Issue – ASBA

|

58. (5)} The issuer shall provide the ASBA facility in the manner specified by the Board where not more than one payment option is provided. Provided that in case of qualified institutional buyers and non-institutional investors the issuer shall accept submit their bids applications using the ASBA facility only. Retail individual investors may either apply through ASBA facility or make payment through cheque or demand draft. | 76. {58. (5)} The issuer shall provide the ASBA facility in the manner specified by the Board where not more than one payment option is provided. Provided that the applicants in a rights issue shall be eligible to make applications through ASBA facility only if such applicant: (i) is holding equity shares in dematerialised mode; (ii) has not renounced entitlement in part or in full; and (iii) is not a renouncee | It is proposed to clarify that applicants in a Rights Issue shall make applications only through ASBA facility and will have the provision to make a physical application in in certain specified scenarios. | Proposed change will not allow applicants in a rights issue to participate in the following cases:

· Applicant is holding equity shares in physical mode; · Applicant has renounced entitlement in part or in full; and · Applicant is not a renouncee. |

| Rights Issue – Underwriting | 13. (1) Where the issuer making a public issue (other than through the book building process) or rights issue, desires to have the issue underwritten, it shall appoint the underwriters in accordance with Securities and Exchange Board of India (Underwriters) Regulations, 1993. | 81. (1) {13. (1)} If the issuer desires to have the issue underwritten, it shall appoint the underwriters in accordance with the Securities and Exchange Board of India (Underwriters) Regulations, 1993.

Provided that the issue can be underwritten only to the extent of entitlement of shareholders other than the promoters and promoter group. |

It is proposed to clarify that issue can be underwritten only to the extent of entitlement of public shareholders (and not for the entitlement of the promoters and promoter group). | Proposed change prohibits underwriting the offer made to the promoters in a rights issue. The same is logical considering that if promoters portion is also required to be underwritten , then one obviously cannot be sure of the subscription to the non-promoters’ portion. |

| Rights issue – Fast Track Rights Issue – Eligibility Conditions | 10. (1)(c the annualised trading turnover of the equity shares of the issuer during six calendar months immediately preceding the month of the reference date has been at least two per cent. of the weighted average number of equity shares listed during such six months‘ period Provided that for issuers, whose public shareholding is less than fifteen per cent. of its issued equity capital, the annualised trading turnover of its equity shares has been at least two per cent. of the weighted average number of equity shares available as free float during such six months‘ period 10. (1)(k) annualized delivery-based trading turnover of the equity shares during six calendar months immediately preceding the month of the reference date has been at least ten per cent. of the weighted average number of equity shares listed during such six months‘ period;

|

99.(1) (d) ({10(1)(c)}- annualised trading turnover of the equity shares of the issuer during six calendar months immediately preceding the month of the reference date has been at least two per cent. of the weighted average number of equity shares listed during such six months‘ period: Provided that for issuers, whose public shareholding is less than fifteen per cent. of its issued equity capital, the annualised trading turnover of its equity shares has been at least two per cent. of the weighted average number of equity shares available as free float during such six months‘ period; 10(1)(k)} annualized delivery-based trading turnover of the equity shares during six calendar months immediately preceding the month of the reference date has been at least ten per cent. of the annualized trading turnover of equity shares during such six months‘ period; | It is proposed to clarify the delivery turnover should be as a percentage of the trading turnover. | The same is a clarificatory change. |

| Rights issue – Fast Track Rights Issue – Eligibility Conditions | 10.(1)(f)(f) the impact of auditors‘ qualifications, if any, on the audited accounts of the issuer in respect of those financial years for which such accounts are disclosed in the offer document does not exceed five per cent. of the net profit or loss after tax of the issuer for the respective years.

|

99.(2)(m) {10(1)(f)} there are no auditors‘ qualifications on the audited accounts of the issuer in respect of those financial years for which such accounts are disclosed in the letter of offer. | To improve the requirements for fast track issues, it is proposed that for a company to be eligible to make a fast track rights issue, it should not have any audit qualifications.

|

Proposed change will not allow companies having audit qualification to come up with fast track rights issue. Such change will have due implications on the compliance status of the listed company. |

| Bonus Issue | ||||

| Bonus Issue | No issuer shall make a bonus issue of equity shares unless it has made reservation of equity shares of the same class in favour of the holders of outstanding [compulsorily] convertible debt instruments[ if any,] in proportion to the convertible part thereof The equity shares so reserved for the holders of fully or partly compulsorily convertible debt instruments shall be issued at the time of conversion of such convertible debt instruments on the same terms or same proportion at which the bonus shares were issued | An issuer shall make a bonus issue of equity shares only if it has made reservation of equity shares of the same class in favour of the holders of outstanding compulsorily convertible debt instruments, optionally convertible instruments, warrants, or lenders who loans are convertible into equity, if any, in proportion to the convertible part thereof. The equity shares so reserved for the holders of fully or partly compulsorily convertible debt instruments, optionally convertible instruments, warrants, or lenders who loans are convertible into equity, shall be issued at the time of conversion of such convertible debt instruments, optionally convertible instruments, warrants, or loans, as the case may be, on the same terms or same proportion at which the bonus shares were issued.

|

All cases of convertible instruments, warrants and loans convertible into equity should be covered. There could be lenders (especially in cases of CDR, whereby lenders have the option to convert their loans to equity. In such cases, there should be a reservation for them.

|

Proposed change may not be flexible considering that every convertible instrument may or may not be opted for conversion. In such cases where the option of conversion is not exercised, bonus issue reserved with respect to such instruments will turn futile. |

| Preferential Issue | ||||

| Conditions for Preferential Issue | 72. (2) The issuer shall not make preferential issue of specified securities to any person who has sold any equity shares of the issuer during the six months preceding the relevant date: … Provided that the above restriction shall not apply to any sale of equity shares by any person belonging to promoter(s) of the promoter group which qualifies for inter-se transfer amongst qualifying persons under Regulation 10 (1) (a) of Securities and Exchange Board of India (Substantial Acquisition of Shares and Takeover Regulations), 2011

|

159. (1) Preferential issue of specified securities shall not be made to any person who has sold any equity shares of the issuer during the six months preceding the relevant date:

Provided that the above restriction shall not apply to any sale of equity shares by any person belonging to promoter(s) of the promoter group which qualifies for inter-se transfer amongst qualifying persons under regulation 10 (1) (a) of Securities and Exchange Board of India (Substantial Acquisition of Shares and Takeover Regulations), 2011 or in case of transfer of shares held by the promoters or promoter group on account of invocation of pledge by a lender. |

This proviso was inserted to restrict any person from taking benefit of short swing profits which is not applicable in this case. It is now proposed that for transfer pursuant to invocation pledge by the lender may be excluded as this is an involuntary sale by the lender and the promoter is not a party to the sale decision. | The proposed change seems to provide genuine relaxation in case of transfer pursuant to invocation pledge by the lender, as the promoter is not involved in the said transaction. |

| Disclosures for Preferential Issue | 73. (1) The issuer shall, in addition to the disclosures required under section 173 of the Companies Act, 1956 or any other applicable law, disclose the following in the explanatory statement to the notice for the general meeting proposed for passing special resolution:

(e) the identity of the natural persons who are the ultimate beneficial owners of the shares proposed to be allotted and/or who ultimately control] the proposed allottees, the percentage of post preferential issue capital that may be held by them and change in control, if any, in the issuer consequent to the preferential issue.

Provided that if there is any listed company, mutual fund, bank or insurance company in the chain of ownership of the proposed allottee, no further disclosure will be necessary. |

163. (1) The issuer shall, in addition to the disclosures required under the Companies Act, 2013 or any other applicable law, disclose the following in the explanatory statement to the notice for the general meeting proposed for passing the special resolution:

identity of the natural persons who are the ultimate beneficial owners of the shares proposed to be allotted and/or who ultimately control the proposed allottees, the percentage of post preferential issue capital that may be held by them and change in control, if any, in the issuer consequent to the preferential issue:

Provided that if there is any listed company, mutual fund, scheduled commercial bank, insurance company registered with the Insurance Regulatory and Development Authority of India, foreign portfolio investor other than Category III foreign portfolio investor, foreign venture capital investor or alternative investment funds in the chain of ownership of the proposed allottee, no further disclosure will be necessary.

|

There is a need to consider inclusion of Category I foreign portfolio investors, Category II foreign portfolio investor, foreign venture capital investors and alternative investment funds in the exclusions in this proviso. These categories are registered with SEBI and hence their KYC is already done at the time of their registration. | The proposed changes seeks to do away with the double disclosure requirements or the Category I foreign portfolio investors, Category II foreign portfolio investor, foreign venture capital investors and alternative investment funds. |

| Adjustments in pricing – Frequently or Infrequently traded shares | 76B. The price determined for preferential issue in accordance with regulation 76 or regulation 76A, shall be subject to appropriate adjustments, if the issuer:

(a) makes an issue of equity shares by way of capitalization of profits or reserves, other than by way of a dividend on shares; (b) makes a rights issue of equity shares; (c) consolidates its outstanding equity shares into a smaller number of shares; e) divides its outstanding equity shares including by way of stock split; f) re-classifies any of its equity shares into other securities of the issuer; g) is involved in such other similar events or circumstances, which in the opinion of the concerned stock exchange, require adjustments.

|

166. The price determined for a preferential issue in accordance with regulation 164 or regulation 164A, shall be subject to appropriate adjustments, if the issuer:

a) makes an issue of equity shares by way of capitalization of profits or reserves, other than by way of a dividend on shares; b) makes an issue of equity shares after completion of a demerger wherein the securities of the resultant demerged entity are listed on a stock exchange; c) makes a rights issue of equity shares; d) consolidates its outstanding equity shares into a smaller number of shares; e) divides its outstanding equity shares including by way of stock split; f) re-classifies any of its equity shares into other securities of the issuer; g) is involved in such other similar events or circumstances, which in the opinion of the concerned stock exchange, require adjustments.

|

It is proposed to include demerger where the equity shares of the resulting entity are listed post demerger. Through a demerger, an undertaking of the company is demerged into a separate company and such resulting company’s shares are listed. Post the listing of the resulting company, the value of the demerged company goes down and it trades accordingly. Hence, adjustment for pre-demerger market price needs to be made. | The proposed amendment broadens the scope of these regulation to demerger as well, where the said adjustment is required post the demerger. |

| Payment of consideration | 77. (1) Full consideration of specified securities other than warrants issued under this Chapter shall be paid by the allottees at the time of allotment of such specified securities:

Provided that in case of a preferential issue of specified securities pursuant to a scheme of corporate debt restructuring as per the corporate debt restructuring framework specified by the Reserve Bank of India, the allottee may pay the consideration in terms of such scheme.

{77.(2) and (3)}An amount equivalent to at least twenty five per cent. of the consideration determined in terms of regulation 76 shall be paid against each warrant on the date of allotment of warrants. |

169.(1) Full consideration of specified securities other than warrants, shall be paid by the allottees at the time of allotment of such specified securities except in case of shares issued for consideration other than cash.

Provided that in case of a preferential issue of specified securities pursuant to a scheme under the corporate debt restructuring framework specified by the Reserve Bank of India, the allottee may pay the consideration in terms of such scheme.

(2) In the case of warrants, an amount equivalent to at least twenty five per cent. of the consideration determined in terms of regulation 76 shall be paid against each warrant on the date of allotment of warrants and the balance seventy five per cent. of the consideration shall be paid at the time of allotment of the equity shares pursuant to exercise of options against each such warrant by the warrant holder. Alternately, twenty five per cent. of the consideration can be computed on the basis of the current market price and the balance can be paid based on the price at the time of exercise.

|

It is proposed to remove the limit of attaching one warrant to a specified security and the issuer will have the flexibility to decide number of warrants to be attached to a specified security.

It is also proposed to clarify that the 25 per cent. consideration can be based on the pricing formula computed using the current market price, and the balance consideration can be paid at the time of exercise which can be subsequently determined at the time of final pricing. |

The proposed changes provide two things:

(a) relaxation- the flexibility to decide number of warrants to be attached to a specified security shall now vest with the issuer.

(b) Clarificatory – the same will remove any ambiguity regarding the pricing. |

| Qualified Institutions Placement | ||||

| Restrictions on amount raised – QIP | 89. The aggregate of the proposed qualified institutions placement and all previous qualified institutions placements made by the issuer in the same financial year shall not exceed five times the net worth of the issuer as per the audited balance sheet of the previous financial year. | Deleted | Companies suffer losses for a variety of reasons including slowdown in their sectors, which leads to erosion of their net worth.

These companies, while in the process of turning around are unable to raise funds through QIP as their pre-QIP net worth will be small or negative. As such, these companies have to look for other avenues for fund raising which may be time consuming and expensive options. QIB investors are in a better position to evaluate such opportunities and QIBs also are not required to be given any protection. Hence, it is proposed to delete this requirement. |

The proposed change will provide the companies an ease in raising the amount through QIPs. |

| Appointment of merchant banker – QIP | 83. (2) The merchant banker shall, while seeking in-principle approval for listing of the eligible securities issued under qualified institutions placement, furnish to each stock exchange on which the same class of equity shares of the issuer are listed, a due diligence certificate stating that the eligible securities are being issued under qualified institutions placement and that the issuer complies with requirements of this Chapter. | 174.(3) The lead manager(s) shall, while seeking in-principle listing approval for the eligible securities, furnish to each stock exchange on which the same class of equity shares of the issuer are listed, a due diligence certificate stating that the eligible securities are being issued under qualified institutions placement and that the issuer complies with requirements of this Chapter, and also furnish a copy of the preliminary placement document along with any other document required by the stock exchange. | The issuer should have the choice of listing (and trading) eligible securities such as CCDs (other than equity shares) issued through the QIP process either at the time of allotment or at the time of conversion. If these remain unlisted, a clarification is needed that the in-principle listing approval has to be sought at the time of issuance but the same can be listed and traded on conversion of such securities. New clause has been added with a proviso to bring out that difference. | As per the proposed changes, furnishing the preliminary document will provide detailed information. Further, the proposed changes provides the option to the issuer an option not to list the securities as well. |

| Minimum no. of allottees | 87. (2) The qualified institutional buyers belonging to the same group or who are under same control shall be deemed to be a single allottee. Explanation: For the purpose of subregulation (2), the expression “qualified institutional buyers belonging to the same group” shall have the same meaning as derived from sub-section (11) of section 372 of the Companies Act, 1956; | 180. (2) Qualified institutional buyers belonging to the same group or who are under same control shall be deemed to be a single allottee.

For the purpose of sub-regulation (2), the expression “qualified institutional buyers belonging to the same group” shall mean entities where (i) any of them controls directly or indirectly, through its subsidiary or holding company, not less than fifteen per cent. of the voting rights in the other; or (ii) any of them directly or indirectly, by itself, or in combination with other persons exercise control over the others; (iii) there is a common director, excluding nominee director amongst the investor, its subsidiary or holding company and other investor. |

Given that the Companies Act, 2013 does not have corresponding provision for Section 372 of the Companies Act, 1956, it is proposed to define ‘same group’ to bring more clarity. | The proposed changes seeks to align the Regulation with Companies Act, 2013 and to provide clarification in the absence of the corresponding provision in the Companies Act, 2013. |

Conclusion

Owing to the various regulatory changes brought in for the listed entities, updating and aligning the SEBI ICDR Regulations is much required. Therefore, the proposed amendments will help in merging all the previous SEBI Circulars related to these Regulations and updating the same with the requirements of the Companies Act, 2013 and the various SEBI Regulations, to maintain uniformity.

[1] https://www.sebi.gov.in/reports/reports/may-2018/consultation-paper-on-review-of-sebi-issue-of-capital-and-disclosure-requirements-regulations-2009_38859.html