RBI’s P2P Regulations: A step forward or backward?

The Reserve Bank of India issued a Master Directions – Non Banking Financial Company – Peer to Peer Lending Platform (Reserve Bank) Directions, 2017 (hereinafter referred to as “Directions”) on 4th October, 2017[1], which is an extensive statement outlining in detail the various rules and regulations that all existing and prospective entities carrying on or intending to carry on the business of Peer-to-Peer (P2P) lending (hereby known as NBFC-P2P) will have to comply with. These Directions shall come in force with immediate effect and shall apply to all NBFC-P2Ps, i.e. with effect from the date of issuance of the Master Directions, mentioned above.

1. Registration

1.1. Eligibility criteria

The basic eligibility criteria for carrying on the business of setting up a P2P lending platform are as follows:

- Only a Non-Banking Financial company shall undertake the business of P2P lending platform.

- All NBFC-P2Ps that are either commencing or carrying on the business of Peer-to-peer lending platform must obtain a Certificate of Registration (CoR) from the bank.

- Every existing and prospective NBFC-P2P must make an application for registration to the Department of Non-Banking Regulation, Mumbai of RBI.

- Any company seeking registration as an NBFC-P2P must have Net Owned Funds of at least Rs. 2 Crores or higher as RBI may specify.

- The RBI has imposed the condition that the company seeking registration must be incorporated in India and must have a robust IT system in place. The management must act in public interest and the directors and promoters must be fit and proper.

While the eligibility criteria remains same for those already into business and prospective ones, however, there is a slight difference in the way the application process of these two categories will be dealt with by the RBI.

1.2. Prospective P2Ps

An entity intending to set up a P2P lending platform will have to make an application to the RBI and at the time of making the application, it should achieve net-owned funds of Rs. 2 crores which must be parked into Fixed Deposit.

Upon submission of the application, if the RBI is of the view that the aforesaid conditions have been fulfilled, it will grant an in-principle approval for setting up of a P2P lending platform, subject to such conditions which it may consider fit to impose. This approval will be valid for a maximum of 12 months from the date of granting of the approval. Within this period of 12 months, the company must put in place the technology platform, enter into all other legal documentations required. We are of the view that during this period, the entity will be allowed to break the fixed deposit and utilize that money to incur capital expenditure as the ones mentioned above. The entity will have to report position of compliance with the terms of grant of in-principle approval to the RBI.

Once the systems are in place and the RBI is satisfied that the entity is ready to commence operations, it shall grant the Certificate of Registration as an NBFC–P2P.

This high NOF requirements and the long gestation can deter prospective players from entering into the market.

1.3. Existing P2Ps

The situation will be different for entities who are already into the business. Any entity carrying out the business of Peer-to-peer lending platform as on the effective date of these Directions, can continue to do so provided that they apply for registration as an NBFC-P2P to the RBI within 3 months from the date of effect of these Directions. This will however, not hamper their business, as the RBI allows them to carry on the business, during the pendency of the application and until the application for issuance of CoR is rejected. If the application is rejected, the applicant will have to wind up its business.

2. Scope of Activities

The Master Directions, next, discuss about the Dos and Don’ts of the P2P lending platforms. Let us first discuss about the Dos.

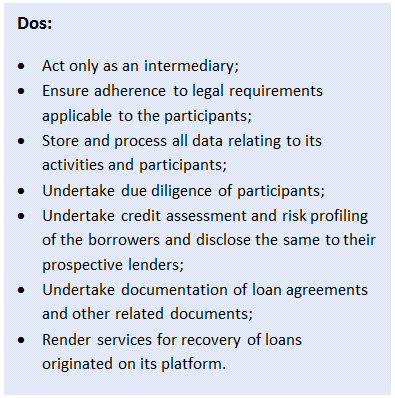

2.1. Dos

An NBFC-P2P can only act as an intermediary that provides an online platform to the participants, i.e., borrowers and lenders, involved in P2P lending. It should ensure adherence to legal requirements applicable to the participants as prescribed under relevant laws, which means this includes the KYC Directions prescribed by RBI. It is also required to store and process all data relating to its activities and participants on hardware located within India. It is permitted to invest in instruments specified by RBI provided they are not traded in.

Another important function that has been added to the scope of the NBFC-P2P credit assessment and risk profiling of the borrowers, the findings of which must be disclosed to the prospective lenders. Earlier, only few of the platforms carried out underwriting on behalf of the lenders, but, henceforth, this is something that a platform will have to carry out mandatorily.

In addition to the above, NBFC-P2Ps will have to get themselves registered with all the Credit Information Companies (CICs) in the country and file the credit information (relating to borrowers), and update them regularly on a monthly basis or at such shorter intervals as may be mutually agreed upon between the NBFC-P2P and the CICs.

NBFC-P2Ps shall also ensure that appropriate agreements are executed between the participants and the platform, which should categorically specify the terms and conditions agreed between the borrower, lender and the platform. The interest rates to be charged on the loans must be displayed in Annualized Percentage Rate (APR) format on the website of the platform.

2.2. Don’ts

Despite being an NBFC, NBFC-P2Ps are prohibited from lending on its own. It shall ONLY act as an intermediary and nothing more. It should not provide or arrange any credit enhancement or credit guarantee and also all loans intermediated must be purely unsecured in nature. It is required to maintain an escrow account to transfer funds and should not hold on its own balance sheet any funds received from lenders for lending, or from borrowers for repayment. It is prohibited from cross-selling any product on its platform except for loan specific insurance products. International flow of funds is also not permitted for NBFC-P2Ps.

During surveys we have observed that some P2Ps have been engaged in lending through their own platforms. This will have to be stopped now. P2Ps are not allowed to carry on any other activity other than P2P loan intermediation. This is much stricter regulation than for any other type of NBFC. Mortgage guarantee companies are allowed to take up any other activity up to 10% of its total assets. All other NBFCs must in general satisfy the principality requirements- at least 50% of its total assets must be financial assets and at least 50% of its total income must be from these assets. This is far more lenient than that being allowed for P2Ps.

3. Prudential Norms

Like all other Directions issued by the RBI for NBFCs, these Directions also lay down the prudential regulations for this class of entities. They are as follows:

- Leverage: The outside liabilities of a platform must not exceed 2 times of its owned funds;

- Concentration limits: The Directions provide for several concentration limits, which are:

- Maximum that a single lender can lend across all P2P platforms – Rs. 10 lakhs;

- Maximum that a single borrower can borrow across all P2P platforms – Rs. 10 lakhs;

- Maximum that a single lender can lend to a single borrower across all P2P platforms – Rs. 50,000;

One apparent concerns that we can point out in this regard is as follows:

Say for instance, a borrower requires a funding of Rs. 5 lakhs, in such case, the platform will have require at least 20 lenders empanelled with itself to meet the requirements of the borrower. Thus, the platforms will have to have large lender base to survive and be able to satisfy loan requirements of borrowers. Therefore, the success of the platforms will be directly related to the scalability of their business.

The P2Ps are also required to obtain a certificate from the borrower and lender, as applicable, that the aforementioned limits are being adhered to.

- Tenure: The tenure of the loans extended through the platforms cannot exceed 36 months.

4. Operational Guidelines

An NBFC-P2P is required to have a Board approved policy in place specifying the eligibility criteria, pricing of services and rules for matching participants on its platform.

The Directions explicitly state that the obligation of an NBFC-P2P does not diminish towards those activities that it has outsourced. It will be held responsible for the actions of its service providers including recovery agents and the confidentiality of information pertaining to the participant that is available with the service provider.

5. Transparency

The Directions has provided for one way transparency. On one hand, it states that the NBFC-P2Ps must disclose to the lender details about the borrower including:

- personal identity;

- required amount;

- interest rate sought; and credit score as per the P2P’s credit rating mechanism;

- terms and conditions of the loan, including

- likely return; and

- fees and taxes associated with the loan.

On the other hand it requires the NBFC-P2Ps to make the following disclosures to the borrowers:

- amount of loan proposed by the lender

- the interest rate offered by the lender etc.

However, it restricts the platform to give out the personal identity and contact details of the lender to the borrower.

Therefore, the Directions provide for full transparency with respect to borrower’s information but partial transparency with respect to lender’s information.

Apart from information of the participants, the Directions require the platforms to provide the following information on its website:

- overview of credit assessment/score methodology and factors considered;

- disclosures on usage/protection of data;

- grievance redressal mechanism;

- portfolio performance including share of non-performing assets on a monthly basis and segregation by age; and

- its broad business model.

6. Signing of the loan terms

One of the requirements of the Direction is that no loan shall be disbursed unless the individual lender has approved the individual recipient of loan and all the concerned parties have signed the loan contract.

Here it is important to take a note that while signing the terms of loan, sufficient measures must be taken by the platform to ensure that the personal and contact details of the lender continues are not revealed to the borrower, owing to the restrictions imposed by the Directions on the platform with respect to transparency.

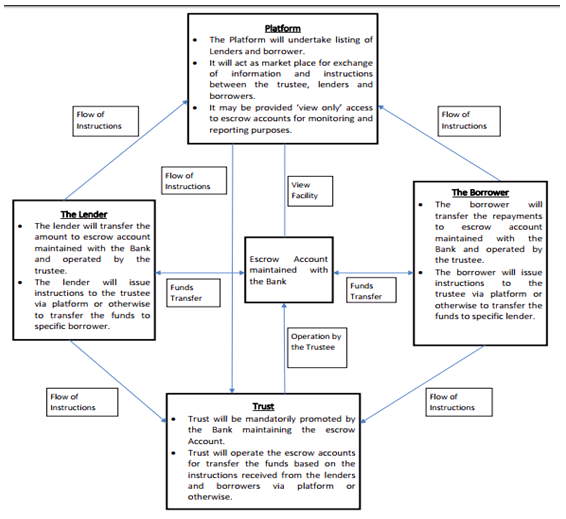

7. Fund Transfer Mechanism

RBI has put a lot of focus on implementing an efficient fund transfer mechanism in order to eliminate any fears of money laundering or usage by the company for its benefit. The Directions stipulate that Fund transfer between the participants on the Peer-to-peer lending platform must take place through escrow accounts which will be operated by a trustee, who must mandatorily be promoted by the bank maintaining the escrow accounts. At least 2 escrows accounts must be maintained – one comprising funds received from lenders and pending disbursal, and the other for collection from borrowers as repayment of loans. All forms of transfer of funds must take place through bank accounts ONLY and cash transactions are prohibited. The graphical representation of the proposed mechanism was included in the Directions, the same has been reproduced below for your reference.

The graphic provided on the Directions for the funds transfer mechanism is somewhat ambiguous as it shows only one escrow account, and also shows direct flow of instructions between the lender/borrower and the Trust, which is odd, as it is the platform who should control the flow of information to the Trust.

8. Fair Practices Code

NBFC-P2Ps are required to follow the usual NBFC related Fair Practices Code (FPC) with the approval of its board. They are further required to disclose the same on their website for the information of various stakeholders.

The NBFC-P2Ps are prohibited from providing any assurances on the recovery of loans.

The platform is required to post the following disclaimer on its website –

“Reserve Bank of India does not accept any responsibility for the correctness of any of the statements or representations made or opinions expressed by the NBFC-P2P, and does not provide any assurance for repayment of the loans lent on it”

The Board of Directors shall also provide for periodic review of the compliance of the Fair Practices Code and the functioning of the grievances redressal mechanism at various levels of management. A consolidated report of such reviews shall be submitted to the Board at regular intervals, as may be prescribed by it.

9.Information Technology Framework

Given the fact that the core operation of P2P lending platforms depends on a robust IT framework, the Directions state that the technology must be scalable in nature to handle growth in business. The Directions also stipulate that there should be adequate safeguards built in its IT systems to ensure that it is protected against unauthorized access, alteration, destruction, disclosure or dissemination of records and data. The RBI also reserves the right to, from time to time, prescribe technical specifications, as deemed fit. The rest of the IT laws are same as those issued to NBFC-SIs in general.

10.Fit and Proper Criteria

An NBFC-P2P must ensure that a policy is put in place with the approval of Board of Directors, setting out the ‘Fit and Proper’ criteria to be met by its directors and also obtain a Deed of Covenants signed by the Directors. RBI may, if it deems fit and in public interest, may independently assess the directors and have the power to remove the concerned directors.

The guidelines have, surprisingly, been kept at par with NBFC-SI. The Deed of Covenants, regular reporting requirements etc. are all observed by NBFCs which are systemically important i.e. NBFCs having asset size of over 500 crores. For P2P platforms to have to observe these is perhaps over-regulation.

11.Requirement to obtain prior approval of the Bank for allotment of shares, acquisition or transfer of control of NBFC-P2P

Given the fact that most P2P lending platforms are start-ups in nature, the requirements are very restrictive in nature. The Directions stipulate that prior approval from the banks will be required in case of:

- any allotment of shares which will take the aggregate holding of an individual or group to equivalent of 26 per cent and more of the paid up capital of the NBFC-P2P;

- any takeover or acquisition of control of an NBFC-P2P, which may or may not result in change of management;

- any change in the shareholding of an NBFC-P2P, including progressive increases over time, which would result in acquisition by/ transfer of shareholding to, any entity, of 26 per cent or more of the paid up equity capital of the NBFC-P2P;

- any change in the management of the NBFC-P2P which would result in change in more than 30 per cent of the Directors, excluding independent Directors;

- any change in shareholding that will give the acquirer a right to nominate a Director

A public notice of at least 30 days shall be given before effecting the sale or transfer of the ownership.

The format for application for prior approval is the same as for other NBFCs.

This is quite unprecedented level of regulation and will seriously increase the bureaucracy PE/VC investors and startups have to go through before a funding round can be closed. Even a 1% allotment which takes one’s shareholding past 26%, then prior permission will be required. Again, should an investor want the right to nominate a Director, then prior approval will be required. This level of regulation is higher than for regular NBFCs and would slow down the process of investments in P2P platforms in India.

12. Reporting Requirements

NBFC-P2Ps must submit a statement showing number and amount of loans during, at the closing of and outstanding at the beginning and end of quarter, including the number of lenders and borrowers outstanding as at the end of quarter to RBI regional office within 15 days after the quarter to which they relate.

They must also disclose the amount of funds held in the Escrow Account, with credit and debit summations for the quarter. Further, number of complaints outstanding at the beginning and end of quarter and disposed of during the quarter, bifurcated between the lenders and borrowers must also be disclosed in order to constantly improve the state of the industry.

13. Conclusion

The regulations on P2P platform was much awaited, but the way the Directions have been crafted, this could cause serious damage to these platforms. To start with, the requirement of maintaining NOF of Rs. 2 crores is not justified since the business is not a capital intensive one. Next, we also feel that RBI has taken a very cautious approach with respect to the credit concentration, however, we feel that this may be enhanced in the future looking at the performance of the sector. Next, the time required for registration of new P2P platforms also seems to be on the higher side. Further, the list of instances for which prior approval will have to be sought from RBI by the platform, may act as a deterrent for the investors who may interested in investing in P2P platforms.

Having said that, the attempt of giving a regulatory shape to the P2P businesses in India, itself must be applauded.

[1] https://www.rbi.org.in/Scripts/BS_ViewMasDirections.aspx?id=11137

Leave a Reply

Want to join the discussion?Feel free to contribute!