New rules of corporate control: Limit on layers of subsidiaries

By CS Vinita Nair, (corplaw@vinodkothari.com)

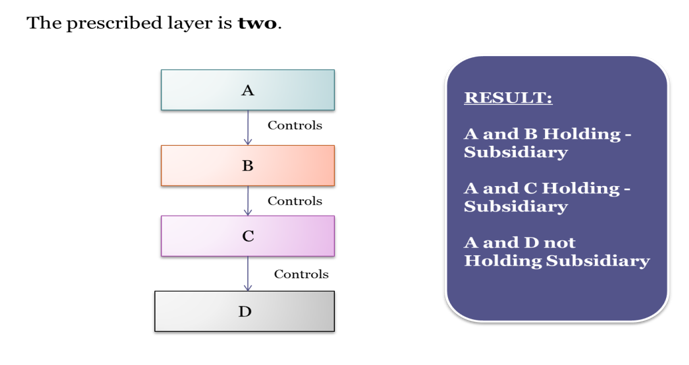

MCA has issued a notification notifying the Companies (Restriction on Number of Layers) Rules, 2017[1], imposing a limit of two layers of subsidiaries which shall be effective from September 20, 2017[2]. Earlier, MCA vide public notice dated 1 June 28, 2017[3] had conveyed its intent of issuing a notification proposing amendments to the Companies (Specification of Definitions Details) Rules, 2014 containing the restriction on layers of subsidiaries beyond prescribed number and had invited suggestions on the draft notification. This write up initially discusses the conditions imposed and thereafter analyses the permitted combinations.

Proviso to Section 2 (87) along with explanation (d) was proposed to be omitted in Companies (Amendment) Bill, 2016. However, in view of reports of misuse of multiple layers of companies, where companies create shell companies for diversion of funds or money laundering, MCA has decided to retain the provisions and commence the aforesaid proviso and explanation. Further, MCA had no intent to exempt private companies from the requirement as well. Companies (Amendment) Bill, 2017 as passed by Lok Sabha omitted the amendment proposed in Proviso to Section 2 (87).

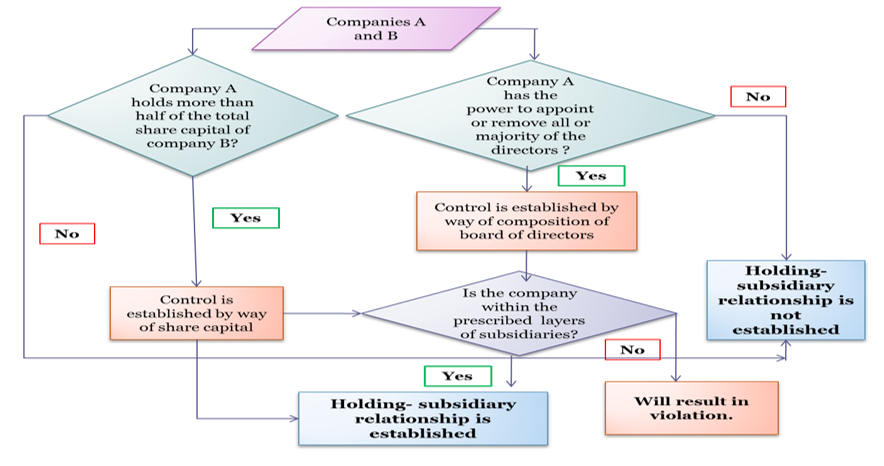

Figure 5 of Taxmann’s Your Queries on Companies Act, 2013

Exempted companies

Rule 2(2) of Companies (Restriction on number of layers) Rules, 2017 shall not apply to following classes of companies, namely:-

(a) a banking company;

(b) a non-banking financial company as defined in the Reserve Bank of India Act, 1934 (2 of 1934) which is registered with the Reserve Bank of India and considered as systemically important non-banking financial company by the Reserve Bank of India; (Nothing specified in relation to housing finance companies/ NBFC CICs).

(c) an insurance company being a company which carries on the business of insurance in accordance with provisions of Insurance Act, 1938 and Insurance Regulatory Development Authority Act, 1999;

(d) a Government company referred to in clause (45) of section 2 of the Act.

Exemptions in cases of Housing Finance Companies, Core Investment Companies as well as Non-Operative Financial Holding Company, Companies that become subsidiary entities pursuant to lenders acquiring majority of shareholding in the borrowing entity as a measure to deal with stressed assets in accordance with the guidelines issued by the Reserve Bank of India from time to time are missed out in the Rules notified.

Exempted subsidiaries – subsidiaries incorporated outside India

First proviso to Rule 2 of the Rules provides exemption to a Company from acquiring a company incorporated in a country outside India with subsidiaries beyond two layers as per the laws of such country.

The exemption in case of acquiring of subsidiaries incorporated outside India should be extended equally to subsidiaries freshly incorporated outside India. There need not be a distinction in acquisition and incorporation of subsidiary outside India. Either a company may acquire a subsidiary outside India which in turn has several layers of downstream investment or it may float a subsidiary outside India which will keep on further incorporating or acquiring subsidiaries outside India.

It cannot be interpreted that a Company incorporating subsidiaries outside India will have to adhere to the restriction of layers even if the same is permitted as per law of that country.

Exempted subsidiaries – wholly owned subsidiaries

One layer which consists of one or more wholly owned subsidiary or subsidiaries shall not be taken into account while computing the number of layers. The proposed Rule provided the explanation to the effect that one layer which is represented by a wholly owned subsidiary shall not be taken into account.

‘Layer’ cannot mean ‘Layers’ based on interpretation that singular includes plural. Therefore, it should not be read as any layer represented by a wholly owned subsidiary. The whole purpose will get defeated if companies are allowed to incorporate layers of wholly owned subsidiaries without any restriction.

It is very pertinent to ponder whether the wholly owned subsidiaries can be at layer not immediately following the layer of holding company.

Example 1: Company ‘A Ltd’ has a subsidiary ‘B Ltd’ which in turn has a subsidiary ‘C Ltd’. ‘C Ltd’ forms a wholly owned subsidiary ‘D Ltd’. How can Company ‘A Ltd’ avail the exemption for the layer represented by ‘D Ltd’ which is not wholly owned subsidiary of ‘A ltd’.

Example 2: Company ‘A Ltd’ has wholly owned subsidiaries ‘B Ltd’ and ‘C Ltd’. Both of these wholly owned subsidiaries hold shares in ‘D Ltd’ in the ratio of 60% and 40% respectively. Thereafter, ‘D Ltd’ forms a subsidiary ‘E Ltd’. In this case, the layer represented by ‘B Ltd’ and ‘C Ltd’ shall not be considered.

Therefore, the layer of wholly owned subsidiary has to reflect in the first layer and not thereafter in order to avail the exemption.

Limit prescribed under Section 186 (1)

Similar restriction on number of layers of investment companies has already been in force under Section 186 (1). The provisions of this rule shall not be in derogation of the proviso to sub-section (1) of section 186 of the Act.

Rules are prospective in nature

The holding companies, other than exempted companies, that breach the conditions of layers of subsidiaries as on the date of commencement of provision are prohibited from incorporating additional layer of subsidiaries.

Such holding companies shall file return in Form CRL-1 with the Registrar within a period of 150 days from the date of publication of these rules in Official Gazette. The form requires specifying layer number of the subsidiary and percentage of shares held by holding company.

The Rules further provide that, such Company shall not, in case one or more layers are reduced by it subsequent to the commencement of these rules, have the number of layers beyond the number of layers it has after such reduction or maximum layers allowed in sub-rule (1), whichever is more.

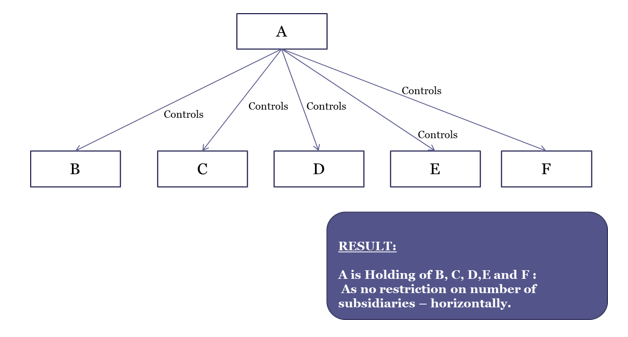

No restriction on horizontal propagation

All the below mentioned structures are permitted and well in compliance

Figure 9 of Taxmann’s Your Queries on Companies Act, 2013

Figure 9 of Taxmann’s Your Queries on Companies Act, 2013

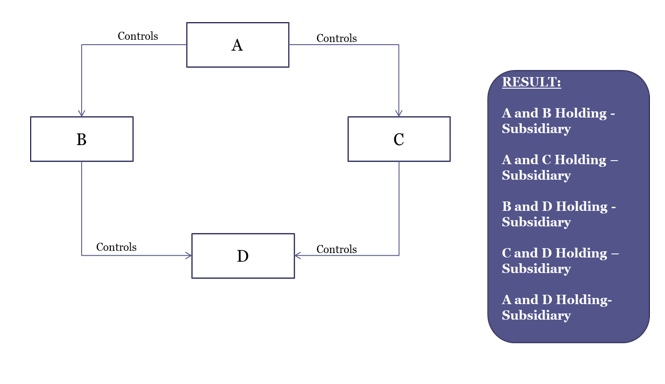

Permitted and prohibited combinations

Case 1:

Figure 8 of Taxmann’s Your Queries on Companies Act, 2013

In the aforesaid structure, if we consider on as is basis, there exists more than 2 layers of subsidiaries. Therefore, an existing company cannot go beyond ‘D’. Once the provisions are enforced, an existing holding company A will not be able to float ‘D’ unless any exemptions/ relaxations become applicable.

Case 2 – ‘B’ is a wholly owned subsidiary of ‘A’:

In that case, the structure is permissible.

Case 3 –’C’/ ‘D’[1] is a wholly owned subsidiary of ‘A’:

In that case, the structure is not permissible for reasons stated above.

Case 4 – ‘B’/’C’ is a subsidiary incorporated outside India:

Currently, the wording of draft rule prescribes ‘acquired’ subsidiaries to be exempted. However, there is no reason to infer that the benefit cannot be extended to subsidiaries incorporated outside India if the laws of host country permit the same.

Case 5 – ‘B” is a subsidiary acquired outside India while ‘C’ and ‘D’ and subsidiaries of ‘B’ incorporated in India

So ‘A’, ‘C’ and “D’ are companies incorporated in India while ‘B’ is a subsidiary outside India. The exemption cannot be extended to ‘C’ and ‘D’ merely because it’s immediately holding company is a subsidiary acquired outside India. Therefore, the limit is likely to be breached unless ‘B’ or ‘C’ or ‘D’ is a wholly owned subsidiary.

Case 6 – ‘A’/‘B’/’C’ fall under exempted companies:

In that case, the restriction shall not apply.

Case 7 – ‘B’/’C’/ ‘D’ is an LLP:

The expression ‘company’ includes body corporate. Therefore, an existing company cannot go beyond ‘D’. Once the provisions are enforced, an existing holding company A will not be able to float ‘D’ unless any exemptions/ relaxations become applicable.

[1] Either of ‘C’ or ‘D’

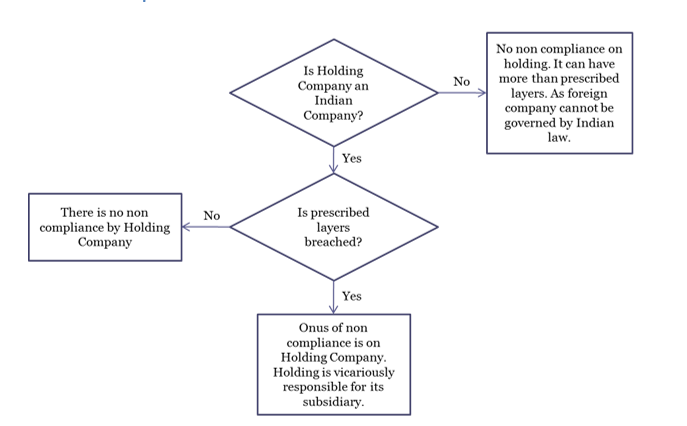

Onus of non-compliance

Figure 7 of Taxmann’s Your Queries on Companies Act, 2013

If any company contravenes any provision of these rules the company and every officer of the company who is in default shall be punishable with fine which may extend to ten thousand rupees and where the contravention is a continuing one, with a further fine which may extend to one thousand rupees for every day after the first during which such contravention continues.

[1] http://egazette.nic.in/WriteReadData/2017/179104.pdf

[2] http://egazette.nic.in/WriteReadData/2017/179105.pdf

[3] http://www.mca.gov.in/Ministry/pdf/Notice_29062017.pdf

[4] Either of ‘B’ or ‘C’ or ‘D’

Surprising to see a provision for fine in the Rules.